Module 1: Dividends and Dividend Policy

A company can distribute surplus cash to its shareholders by paying them a cash dividend, repurchasing their common shares, or a combination of both. The amount paid out is normally the portion of a business’s earnings that is not needed to finance its future growth but it can also include a return of share capital if the company is liquidating all or a portion of its operations. Common share dividends are quoted as a dollar amount per share but preferred share dividends are sometimes denoted as a percentage of the share’s par value.

Many academics feel that it is irrelevant whether a company pays a dividend or not. They claim that if the dividend is too low, shareholders would simply generate additional cash by selling some of their shares in the company. If the dividend is too high, they would use the money to buy more shares. It does matter though whether a shareholder receives a cash dividend or earns a capital gain selling shares as these two sources of income are taxed differently. Transaction costs incurred by shareholders buying and selling shares change with the size of the dividend as do the issuance costs paid by companies raising new equity. The size of the dividend influences management’s financial flexibility and the agency costs incurred by the company’s shareholders. Finally, the size of a dividend and whether it is increasing or decreasing provides important information to the financial markets about a firm’s financial performance.

Senior managers must be familiar with the mechanics of distributing a company’s surplus cash and be able to design a dividend policy that best meets its financing needs and stock market expectations.

1.1 | Taxation of Dividends and Capital Gains

Dividends and the capital gains earned when a share is repurchased are taxed differently depending on the type of investor. This may affect the decision whether to pay a cash dividend or repurchase common shares.

Individual Investors Outside a Tax-Shelter Account

For individual investors saving outside of a tax-sheltered account such as a company pension plan, Registered Retirement Savings Plan (RRSP), or Tax-Free Savings Account (TFSA), capital gains are taxed at a slightly lower rate than dividends in Canada and also offer a tax deferral. A tax deferral means capital gains are only taxed when the shares are sold, which can be an extended period of time for a long-term investor who is saving for their retirement in 20 to 30 years. This may influence a company to distribute earnings through a stock repurchase instead of a dividend

The following exhibit compares the effective tax rates for dividend and capital gain:

Exhibit 1: Taxation of Dividends and Capital Gains in Canada

| Dividends (CAD) | |

|---|---|

| Dividend income | 100.00 |

| Gross-up (38% of dividend income) | 38.00 |

| Taxable (grossed-up) dividend | 138.00 |

| Federal tax (29% of taxable dividend) | 40.02 |

| Provincial tax (12.29% of taxable dividend) | 16.96 |

| Federal dividend tax credit (15.02% of grossed-up dividend) | 20.73 |

| Provincial dividend tax credit (10% of grossed-up dividend) | 13.80 |

| Taxes payable | 22.45 |

| Effective tax rate | 22.45% |

| Capital Gains (CAD) | |

| Capital gains | 100.00 |

| Taxable capital gains (50%) | 50.00 |

| Federal tax (29%) | 14.50 |

| Provincial tax (12.29%) | 6.14 |

| Taxes payable | 20.64 |

| Effective tax rate | 20.64% |

The effective rates vary by province. The Provincial and Federal Dividend Tax Credits help to eliminate the double taxation of dividend income. Double taxation means that corporate income is first taxed at the corporate income tax rate when it is earned and then taxed again when the dividends are distributed to shareholders at their personal tax rate.

Individual Investors Inside a Tax-Shelter Account

For investors in tax-sheltered accounts that are funded with before-tax dollars like most pension plans and RRSPs, dividends and capital gains are not taxed as long as the funds remain inside the account. The dividends and capital gains are tax as normal income when funds are taken out of the account in the future.

For investors in tax-sheltered accounts that are funded with after-tax dollars such as some pension plans and TSFAs, dividends and capital gains are not taxed as long as the funds remain inside the account. The dividends and capital gains are not tax when they are taken out of the account either as taxes were paid prior to the funds being invested.

Whether retained earnings are distributed as dividends or capital gains is irrelevant to both these types of investors.

Corporations

Corporations do not pay tax on intercorporate dividends but do pay tax on all capital gains. This favours the payment of dividends instead of capital gains to corporations.

Non-Profit Organizations

Non-profit organizations like charities and their charitable endowments are not subject to tax. Whether retained earnings are distributed as dividends or capital gains is irrelevant to non-profits.

Trusts

Trust beneficiaries can be taxed either like investors inside a tax-sheltered account or outside a tax-sheltered account so the preference for dividends or capital gains varies.

1.2 | Types of Dividends

Cash Dividends

Regular cash dividends are normally paid quarterly in North America, but additional extra or special dividends may be paid at any time.Extra dividends depend on the availability of cash in that period. These dividends may begin to be viewed as regular dividends by investors if they are paid too often. Special dividends are much less common, and are not normally confused by investors with regular dividends.

Combining small regular dividends with extra dividends is common in cyclical industries with variable cash flows. Large extra dividends are paid out during cyclical highs when companies generate more cash than needed for growth and are then curtailed during cyclical lows when cash is required internally. Special dividends may be used to distribute surplus cash after one-time events such as the sale of a business unit.

Dividends are commonly paid on a semi-annual basis in Europe and Japan and annually in the rest of Asia. A longer time between dividend payments allows companies to save on administration costs and earn more interest on their idle cash balances. These savings are particularly significant for companies with a large number of shares.

Stripped common shares are created by investment dealers who sell a share’s dividend and capital gain streams separately to appeal to different investors. Some investors want regular cash payments to support their spending needs, while others want their investment to grow at a faster rate by deferring taxation on any capital gains. Investment dealers are financial institutions who help companies sell new stocks and bonds by pricing the issues and finding interested buyers such as pension plans, trust companies, life insurance companies, or mutual funds.

Important Dividend Dates

There are several important dates relating to the distribution of dividends:

- Date of Declaration.

- Date when the company’s board of directors agrees to pay a dividend to its shareholders and the dividend becomes a liability of the business.

- Ex-Dividend Date.

- Date set by the stock exchange that determines which shareholders are entitled to the dividend. Shares trade cum-dividend (entitled to the dividend) before this date and ex-dividend (not entitled to the dividend) afterwards.

- Date of Record.

- All shareholders listed in the corporation’s records on this date receive the dividend. This date is set by the company and usually occurs one or two days after the ex-dividend date to provide sufficient time for them to process all sales transactions.

- Date of Payment.

- Date when the dividend is paid to shareholders.

Share prices generally fall by the average after-tax value of the dividend when they go ex-dividend since potential buyers are no longer entitled to that payment. For example, if a share with an upcoming dividend of CAD 1 was trading at CAD 30 cum-dividend just prior to the ex-dividend date, it would trade at approximately CAD 29 ex-dividend. This is consistent with the dividend discount model which states the value of a share is equal to the present value of the future dividends a shareholder will receive.

Dividend Re-Investment Plans and Stock Purchase Plans

Some companies offer dividend re-investment plans (DRIPs) so shareholders can reinvest their dividends if they do not want them by buying additional shares in the company. Many DRIPs also offer a stock purchase plan (SPP) or optional cash purchase (OCP) feature that allows shareholders to buy additional shares without reference to the size of their dividend although a limit may be placed on the number of shares that can be purchased this way. Shares issued under a DRIP are usually new equity, but if the company does not need the additional capital, they sometimes buy existing shares in the open market to meet shareholder demand.

DRIPs offer a number of advantages:

- Companies do not incur issuance costs when raising new capital because the shares are sold directly to investors. Equity issuance costs average 7% to 8% in Canada, but these expenses are much higher for the smaller issues of startup or growth companies.

- Shareholders may be able to purchase additional stock at a discount since they are buying directly from the company who can pass along some of their savings. Shareholders also save on trading costs by not having to purchase the shares through a stockbroker. DRIPs are especially attractive to small investors as they do not have to buy shares through the exchanges in the standard board lot size of 100 shares to receive the lowest commission and they may also be allowed to buy fractional shares.

- Management is able to build a more diverse and loyal investor clientele that is less likely to sell their shares during a market downturn resulting in a more stable share price.

- Investors are forced to cost average their share purchases over time. Cost average means shareholders buy shares regularly throughout the normal up-and-down movements of the stock market, and thus they do not risk buying all their shares during a market peak when shares are likely overvalued.

One disadvantage of a DRIP is the dividends re-invested are still taxable even though shareholders receive no cash. This makes these plans more suitable for investors who are using tax-sheltered accounts like an RRSP.

Liquidating Dividends

Liquidating dividends occur when a business is fully or partially liquidated and its share capital is returned to investors. Since the dividend is paid out of the initial investment in the company and not retained earnings, it is not subject to tax.

Stock Splits

Stock splits lower a company’s share price by exchanging current shares for multiple new shares commonly in a 2-for-1, 3-for-2, or 3-for-1 ratio. The number of outstanding shares increases, but the value of equity remains the same, so the price of a share falls. Each shareholder owns more shares and has more votes, but continues to have the same fractional ownership and voting position in the company after the split and the value of their investment does not change.

Companies use stock splits to keep their share price in a preferred trading range that is more appealing to retail and institutional investors leading to greater market liquidity and a higher share price. For example, shares trade on the TSX in standard board lot sizes of 100 which can become quite expensive for retail investors if the share price becomes too high. The concept of a preferred trading range is supported by management surveys but also by practice. Shares have continued to trade in the same average price range under CAD 100 over decades despite considerable growth in the consumer price index and the value of corporate equity which should have increased average share prices.

Theoretically, the decision to split a stock should be irrelevant since the value of a shareholder’s investment and their ownership age does not change. Industry research does not support this view and has contributed a number of important findings:

- Surveys of managers indicate that they strongly feel there is a preferred share price range.

- Managers do use stock splits to reduce their company’s share price to the preferred price range after periods of high earnings and dividend growth. Splits are structured to reduce the share price to approximately the same level that it was at after the last stock split.

- Shareholders generally earn substantial positive abnormal returns after a stock split due to greater market liquidity (trading volume) caused by an increased number of shares and a lower share price. This is limited by increased transaction costs after the split that are caused by a higher bid-ask spread relative to the new share price. The higher relative spread does encourage brokerage firms to recruit more new investors thus increasing market liquidity and creating a more diversified shareholder base. Bid-ask spread is the difference between what a market maker pays for a share (bid price) and what they will then sell it for (ask price). The size of the spread varies with the liquidity of the market and is a major transaction cost for investors.

- Shareholders generally earn substantial positive abnormal returns after a stock split due to the favourable signal it gives about a company’s future performance. Shareholders believe management would not split a stock unless they expected the company’s strong performance to continue. If the share price is reduced below the last stock split price, the markets interprets this information more positively thinking future performance will be even stronger. The announcement of a stock split also attracts new investors who had not considered the stock in the past and causes equity analysts to raise their earnings forecasts for the company. Both these factors contribute to a higher share price.

Reverse Stock Splits

A reverse stock split (also called a consolidation) is the same as a stock split except it reduces the number of shares such as in a 1-for-10 ratio. Since the value of equity remains the same, having fewer shares leads to a higher share price. Reverse stock splits are used to:

- Return a share price to its preferred trading range to improve market liquidity.

- Eliminate the negative stigma associated with a low-priced share such as with “penny” stocks that are generally valued at under a few dollars.

- Comply with security regulations that prevent institutional investors from purchasing shares that are valued below a specified price because they are perceived to have greater risk.

- Comply with minimum price rules established by some stock exchanges or indexes to prevent shares from being delisted or removed from an index.

- Lower administrative costs by reducing the number of shares.

- Eliminate minority shareholders who own less than a specified number of shares after a split.

Similar to stock splits, industry research indicates that reverse stock splits are relevant. Generally, investors experience significant negative abnormal returns after a reverse split. Management is signaling that a decline in share price is permanent and that it wants to return the share price to the preferred trading range to improve it liquidity or comply with market requirements. Firms that declare multiple reverse stock splits usually fail or are eventually delisted.

Stock Dividends

Stock dividends have the same effect as stock splits. Instead of paying the dividend in cash, dividends are paid with new shares in the company. Again, the number of outstanding shares goes up, but the equity remains the same, so the value of each share falls.

Stock dividends and stock splits do not change liquidity ratios (e.g., current ratio) or financial leverage ratios (e.g., debt ratio) as assets and liabilities are unaffected since no cash is distributed. Stock dividends require that equity be moved from retained earnings to share capital but the company’s total equity remains the same. The amount transferred equals the number of shares issued times their market value. Stock splits require no journal entries but the higher number of shares is noted in the financial statements.

The rationale for utilizing stock dividends are similar to stock splits but industry research findings are different. Shareholders earn positive abnormal returns after a stock dividend due to the favourable signal they give about a company’s future performance, but research shows these abnormal returns are considerably lower than with stock splits. Market liquidity is also improved through higher trading volume and by returning the share price to its preferred range, but there is generally no significant abnormal shareholder return. This can be explained by the fact that stock dividends result in considerably fewer new shares on average when compared to stock splits. Finally, it is sometimes maintained that a stock dividend is used by companies to conserve cash to fund lucrative growth opportunities or to deal with temporary cash shortages. The stock dividend supposedly sends a signal to investors that even though the regular dividend is being cut now, this action is only temporary. This does not appear to be the practice based on industry research.

Stock dividends are not common in Canada because they are taxed as regular dividends by the Canada Revenue Agency (CRA). Once equity is transferred from retained earnings to share capital, any distributions from share capital are considered a liquidating dividend and are not taxable, so the CRA charges tax at the time of the transfer.

1.3 | Stock Repurchases

Stock repurchases or buybacks are an alternative to paying cash dividends. Companies distribute surplus cash to shareholders by re-acquiring their shares. Only shareholders who choose to sell will receive part of this cash distribution and their percentage ownership in the company will fall. These shares are either cancelled or held as treasury shares which can be re-sold more quickly. Regardless, they no longer have a vote or pay a dividend, and are excluded in the calculation of earnings per share.

Historically, paying dividends was the dominant method of distributing cash to shareholders but that has changed dramatically. The value of stock repurchases now exceeds dividends and the proportion of companies using stock repurchases surpasses those paying dividends. This trend started in the U.S. in the early 1980’s when U.S. regulators decided to no longer considered stock repurchases to be a form of insider trading even though the company’s management was in possession of material, non-public information about the firm. Stock repurchases are now gaining importance in other developed economies in both Europe and Asia.

There are many reasons for the popularity of stock repurchases:

- Provide companies with greater financial flexibility since their management is no longer committed to maintaining large regular dividends, but can instead focus spending on research and development, capital expenditures, and other important corporate expenses.

- Can be easily postponed, reduced, or eliminated as they are not viewed as permanent by shareholders like a regular dividend. If a company reduces its dividend, market pessimism will likely increase and its share price will decline. It is safer for a firm to fulfill its investment needs first and then distribute whatever remains to shareholders using a stock repurchase.

- Used to support the share price when a company is issuing new equity or in reaction to negative market news such as an executive resignation or a decline in earnings.

- Signal to investors that a company’s shares are undervalued as management is thought to have superior information about the company’s future performance and would rationally only buy shares if they are undervalued. This causes the share price to increase as investors buy shares hoping to earn a profit. The S&P 500 Buyback Index measures the performance of the 100 S&P 500 stocks with the highest buyback ratios over the past 12 months. Exchange traded funds (ETFs) are available that track this and other similar indexes and these funds typically generate positive excess returns compared to their benchmarks.

- Used by companies to time the equity markets by repurchasing shares when prices are undervalued and reselling them when overvalued. As mentioned, managers are trading while in possession of insider information which is most valuable when shareholders are less informed retail investors and not sophisticated institutional investors or insiders such as managers. The discrepancy between public and private information is greatest in this case.

- Increase executive compensation by inflating a company’s earnings per share and share price by reducing the number of shares outstanding. Well-designed pay plans should adjust their performance targets like earnings per share for the effect of stock repurchases so managers are not unfairly rewarded.

- Offset the dilution of earnings per share caused by share-based compensation plans by repurchasing shares and limiting the net increase in stock.

- Quickly adjust a company’s capital structure to the optimal borrowing level or over leverage the firm as part of a takeover defense.

- Distribute surplus, low-yielding cash balances to shareholders to limit agency costs.

- Reduce taxes as capital gains earned in a share repurchase are taxed at a lower rate than dividends in many countries.

- Improve shareholder cash and tax planning. Shares can be sold as part of a stock repurchase if cash is needed, otherwise shareholders can remain invested and continue to defer capital gains taxes.

Mechanics of Stock Repurchases

The use of stock repurchases is limited in many countries to protect both shareholders and creditors. The Canada Business Corporation Act (CBCA) does not allow a company to pay a dividend or repurchase stock if it renders it unable to pay its liabilities or makes it insolvent (i.e., assets are less than liabilities). A corporation’s by-laws can stipulate that shareholders need to approve all share buyback plans. Bank loan conditions usually limit the size of stock repurchases to keep more cash in a business so it can better service its debts. Finally, stock exchanges generally prescribe the repurchase procedure that companies must follow to ensure all investors are treated fairly.

Stock repurchases in Canada can be done in one of four ways:

- Open-Market Share Repurchase: Under a Normal Course Issuer Bid (NCIB) through the Toronto Stock Exchange’s (TSX), a company can repurchase up to 5% of its shares over a 12-month period at the market price with no more than 2% purchased in a given 30-day period. Since the buyback is small, the exchange does not feel that the transparency of a public tender offer is required.

- Fixed-Price Tender Offer: With the TSX’s permission, the company can repurchase over 5 per cent of its shares in a short period of time. The number of shares and the repurchase price are specified and the price is usually set at a substantial premium over the market price (approximately 20 per cent) before the public repurchase announcement. This formal tender offer is required by the stock exchange to ensure all investors can participate in the offer. If more than the desired number of shares are tendered, repurchases are made on a prorate basis. If less are tendered, the offer can be cancelled, only the shares offered can be purchased, or the expiration date can be extended.

- Dutch-Auction Bid: With the TSX’s permission, the company indicates the number of shares it wishes to repurchase and provides a set price range. Investors offer to sell blocks of shares at varying prices in the range. The company then determines one bid price at or below it will be able to purchase the number of shares it wants . This method allows companies to buy back shares at the best possible price. If too few shares are offered up then the company can either cancel the auction or buy the shares offered at the maximum price.

- Targeted (selective) Stock Repurchases: This method buys the stock of specific shareholders to 1) reduce the administration costs of servicing small investor groups; 2) provide a legal remedy when a shareholder group has been found to have been treated unfairly by the company; or 3) buy out large blocks of shares from particular investors at a premium to block a corporate takeover or silence their criticism of the firm. Use of this method is limited by the TSX because it doesn’t offer the same price to all investors but it may be allowed in special cases.

Open-market share repurchase plans are substitutes for paying regular dividends and account for over 95% of buybacks globally. They allow companies to repurchase relatively small numbers of shares to distribute surplus cash to shareholders, but also pursue other financial goals such as supporting the share price or timing the equity markets. Fixed-price tender offers and Dutch-auction bids are used to buy much larger blocks of shares as part of a corporate takeover defense or other forms of business restructuring.

Open-market share repurchase plans are generally announced with great fanfare as either a dollar amount or a percentage of the company’s outstanding shares to send a positive signal to the stock market. The effect on the company’s share price varies with the size of the repurchase announced and the likelihood that it will be completed. Repurchase plans are very flexible allowing managers to buy back shares at the most opportune time over a number of years when their liquidity is strongest or the share price is the most undervalued. These plans are not binding so management can cancel them at any time or only buy back a portion of the shares.

Companies buy back approximately 80% of the shares that they initially announce. This completion rate is positively correlated with the firm’s reputation, particularly with its track record of completing previous stock repurchases. Also, the more undervalued its share, the more likely a company is to complete the plan because of the higher profit potential. Finally, companies with more uncertain cash flows generally have lower completion rates. Many firms also decide to buy back considerably more shares than they initially announced. These factors support the theory that open-market share repurchases plans provide management with greater financial flexibility than paying regular dividends. As discussed, not fulfilling share repurchase obligations also has little negative effect on the share price as compared to reducing a regular dividend.

If a company has a poor track record of completing share buybacks, it can enhance its reputation by using accelerated share repurchases (ASRs). First, the company enters into an agreement with an investment bank to have them purchase the announced number of shares in the future. The company pays the investment bank upfront for these shares at an agreed upon price. Second, the investment bank borrows the shares from their clients or security lenders and then transfers them to the company who immediately reduces the number of shares outstanding. Third, in the coming days or months, the investment bank purchases the company’s shares in the open market and hopefully earns a profit before returning them to their clients or security lenders. Security lending allows investors to earn fee income on securities in their portfolios that they lend. The transaction is very safe for investors as it is secured by collateral pledged by the investment banker who also compensates the security lender for any missed dividends or rights distributions.

The primary advantage of ASRs is that the buyback plan is executed immediately, which enhances the company’s reputation. Fast completion may also be important if the company is trying to manipulate its earnings before awarding executive compensation or hiding recently issued stock options before reporting to shareholders. The investment bank also absorbs any price risk related to the share repurchase by agreeing to a set price with the company at the beginning of the process. Finally, investment banks can buy back shares in the stock market at any time, while companies are unable to trade during earnings blackout periods. This increases the potential to time the equity markets. A blackout period is the period of time before a corporate earnings announcement when the company and its directors and specific employees are unable to trade in the company’s share because they are in possession of insider information.

1.4 | Is Dividend Policy Relevant?

In perfectly efficient capital markets, investors have full information and act rationally, and the markets are free of frictions such as transaction costs, issuance costs, or taxes that may influence the trading of assets. In these types of markets, dividend policy is irrelevant because dividends can be gotten by selling shares (homemade dividends) or avoided by buying additional shares with the dividends received.

Markets are not perfectly efficient though and a number of factors support paying either a higher or lower dividend thus making a company’s dividend policy relevant. These factors include:

- Transaction Costs.

- Brokerage costs are incurred by investors when selling and buying shares. This supports paying higher dividends as investors avoid the cost of selling shares to raise needed cash.

- Issuance Costs.

- Issuance or flotation costs are high on the sale of new debt and equity especially for startup companies or companies experiencing financial difficulties. This supports paying lower dividends as more cash is retained, reducing the need to issue new debt or equity.

- Irrational Investor Behavior. Some investors discipline themselves to preserve their investment capital by spending only the cash return (“live off the dividends, invest the capital”). This supports paying higher dividends as investors have a higher cash return each year.

- Taxes.

- Capital gains may be taxed at a lower rate than dividends and offer a tax deferral. Business income is also usually taxed at a lower rate than personal income. This supports paying low dividends as retaining funds allows businesses to take advantage of lower tax rates on capital gains and business income and defer income taxes.

- Agency Costs.

- Some managers view paying dividends as a sign of failure and instead retain their earnings and waste them on new projects having negative net present values, overpaying for corporate takeovers, or investing in low-yielding marketable securities that do not earn the cost of capital. This supports paying higher dividends as agency costs are reduced by getting excess funds out of a business to its shareholder so they are not wasted by management

- Asymmetric Information.

- Managers have better information about the operation of their companies and the markets react when they act based on this knowledge. This supports paying higher dividends as it indicates to investors that a company’s prospects are improving when it is able to pay higher dividends.

- Bird-in-Hand Argument.

- It is better to receive a smaller dividend now instead of possibly a larger dividend in the future if earnings are reinvested successfully. This supports paying higher dividends as current dividends have more certainty in the minds of shareholders about a business’s financial health.

- Financial Flexibility.

- Having more cash allows companies to better respond to unforeseen operating problems or capitalize on sudden investment opportunities. This supports paying lower dividends to increase cash reserves.

Dividend Policy over the Business Life Cycle

The importance of some of the factors that influence dividend policy vary over a business’ life cycle.

Exhibit 2: Varying Influence of Factors

| Source of Market Friction | Start-Up | IPO | Rapid Growth | Maturity | Decline |

|---|---|---|---|---|---|

| Taxes to equity holders | High | High to majority owners | Declining with the addition of new equity owners | Declining with growing institutional ownership | Declining with institutional and corporate ownership |

| Agency costs | Low | Low | Growing | High | Very high |

| Asymmetric information | Extremely High | Very high | Moderating | Falling | Modest |

| Flotation costs | High | High | Moderating | Low | Low |

| Transactions costs | High | High | Moderating | Falling | Low |

| Implied dividend policy | No dividends | No dividends | Low-dividend payout policy | Growing dividend payout policy | Generous dividend payout policy |

Adapted from: Lease, R. C., John, K., Kalay, A., Loewenstein, U., and Sarig, O. H. (2000). Dividend policy: Its impact on firm value. Boston, MA: Harvard Business School Press.

- Taxation to equity holders.

- Market friction relating to this factor is high in the start-up and IPO phases as any dividends received by founders, controlling shareholders, angels, and venture capitalists are normally taxable. During the rapid growth and maturity phases non-taxable institutional and corporate investors make up a larger proportion of the ownership group. This factor has decreasing importance over the business life cycle.

- Agency Costs.

- Market friction relating to this factor is low in the start-up and IPO phases as managers of new businesses are normally the founders or controlling shareholders who will act in their own best interest. During the rapid growth and maturity phases, professional managers are hired to lead the company and the founders may assume a more passive role, lose control, or sell out entirely. Once this occurs, agency costs relating to the separation of management and ownership can become quite high. This factor has increasing importance over the business life cycle.

- Asymmetric Information.

- Market friction relating to this factor is high for businesses in the start-up and IPO phases are typically privately held so their shares are not traded publicly. Since outside equity analysts do not follow private companies closely, little investment information is available other than what is provided by management making this information very valuable. In the rapid growth and maturity phases, more information becomes available as more equity analysts follow the stock once the company goes public and share trading volume increases. This factor has decreasing importance over the business life cycle.

- Flotation Costs.

- Market friction relating to this factor is high in the start-up and IPO phases as new entrepreneurs have great difficulty raising new equity. They have limited capital of their own and angels and venture capitalists demand a high percentage of businesses in exchange for their investment. Raising equity publicly is not an option until an initial public offering (IPO) is completed which is expensive. Flotation costs for subsequent share issuances are high to moderate until the business matures. This factor has decreasing importance over the business life cycle.

- Transaction Costs.

- Market friction relating to this factor is high for investors in the start-up and IPO phases as trading costs for shares in private or small public companies are high due to a lack of market liquidity. As businesses grow and then mature, market liquidity improves as the number of investors interested in buying these shares increases. This factor has decreasing importance over the business life cycle.

Other Factors Influencing Dividend Decisions

Besides market imperfections, a number of practical considerations also influence the dividend decision.

- Liquidity Position.

- As discussed, the Canada Business Corporations Act does not allow a company to pay dividends or repurchase stock if it is then unable to pay its liabilities or made insolvent. Even a highly profitable company can be “cash poor” if its resources are used to finance additional working capital, fixed asset purchases, or debt reduction. Businesses with liquidity problems must restrict their dividends.

- Restrictive Lending Conditions.

- Loan agreements usually limit a company’s dividends or prevent them from being paid at all until its debts are repaid. These agreements also contain liquidity requirements like maintaining a minimum current ratio that affect how a business can spend its cash. Preferred share agreements also stipulate that companies cannot pay common share dividends if their preferred share dividends are in arrears.

- Control Issues.

- Issuing shares may result in the current owners of a business losing control. This is especially important for many small and medium-sized enterprises where the founder and their family still own the majority of shares. Dividends may have to be lowered to curb the number of shares issued.

- Limited Access to External Financing.

- Small and medium-sized enterprises have limited access to capital markets because of their smaller size and minimal credit history. Their earnings have to be retained instead of being paid out as dividends.

- Growth Rate.

- High-growth companies may need to restrict dividends to finance their rapid expansion. Conversely, mature companies generally have considerably more funds than they need.

- Earnings Stability.

- Businesses with volatile earnings due to cyclical sales, intense competition, variable input prices, or high operating leverage need to reduce their dividends so they have sufficient cash resources in a downturn.

- Financial Leverage.

- Companies with high debt ratios are more likely to retain their profits instead of paying dividends because of large interest and principal payments.

1.5 | Dividend Theories

Market imperfections and other factors that affect the dividend decision have resulted in a number of theories that help to explain the dividend policies that companies adopt. These include:

-

Clientele Effect

Specific groups of investors prefer different dividend policies, such as paying high or paying low dividends, and will invest in companies that consistently follow these policies to minimize their transactions costs (i.e., buying and selling of shares) as they attempt to meet their cash flow needs. Erratic dividend decisions mean a dividend policy cannot be identified, so investors will buy fewer shares, hurting the share price. Companies are very aware of what their investor clientele wants and are careful to consistently meet their needs.

Investors in higher dividend companies include:

- “Widows and orphans” who need high dividends to meet their living expenses.

- Endowments or trusts that are limited by statute or contract to spending only the dividends earned and not the capital of a fund.

- Investors who are subject to government regulations that encourage safe investing by only allowing investments in companies with established dividend records.

- Mutual funds whose investment strategy is to buy high dividend yield stocks.

- Corporations that do not pay tax on inter-corporate dividends but do pay tax on capital gains.

Investors in lower dividend companies include:

- Long-term investors outside of a tax-sheltered account who prefer capital gains due to a lower tax rate and tax deferral.

Investors who are indifferent to dividend levels include:

- Investors in tax-sheltered accounts such as company pension plans, RRSPs or TFSAs.

- Non-profit organizations and charitable endowments who are not taxed.

-

Signaling Theory

When managers and outside investors have the same information about a company, a situation of symmetric information exists. Asymmetric information exists when managers have additional insider information. This is normally the case due to their senior positions in the company so investors interpret dividend changes as asymmetric information about the company’s future performance. For example:

-

- Falling dividends mean a company is having difficulty and cannot support its previous dividend level so share prices fall.

- Increasing dividends mean a company has good prospects and can support the higher dividend level in the future so share prices rise.

- Regular dividend increases have a stronger positive affect on the share price than increases in special or extra dividends as the increase is viewed as permanent.

- Dividend increases have a greater positive effect on the share price if accompanied by active share repurchases by managers as they are investing their own money.

- Dividend increases have a greater positive effect on share prices for high-growth than low-growth firms because high-growth firms are more difficult to value due to their more uncertain futures thus making the asymmetric information provided by management of greater value.

- Dividend increases are recommended if the share is undervalued and the company wants to increase the share price before going to the equity markets to raise capital.

- Tender offers as opposed to Dutch auction share repurchases are viewed more favourably because the company is committed to paying a large premium so share prices rise further.

-

-

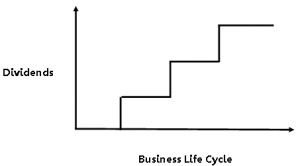

Residual Dividend Theory

Companies undertake and finance all positive net present value projects with a combination of retained earnings and debt in accordance with their optimal capital structure. They only issue new shares as a last resort due to high equity issuance costs, control issues, and the possibility that shares will have to be sold when the share price is undervalued. Any residual income remaining after this is paid out as dividends as it is not needed by the company.

A company’s residual income will increase over its life cycle. It will be minimal in the development and growth stages as all retained earnings are needed to finance rapid growth but will rise as the business expands, matures, and potentially declines. A company’s dividend payout ratio increases over time.

Exhibit 3: Dividend Distributions over the Business Life Cycle

Phase Dividend Level Development No cash dividends Growth Low cash dividends Expansion Low to moderate cash dividends Maturity Moderate to high cash dividends Residual income may vary in the short term depending on the company’s profitability, the volatility of its earnings and the availability of positive net present value projects in a particular year. Greater profitability means more higher dividends can be paid while more volatility earnings favours paying lower dividends to ensure that funds are always available to finance positive net present value projects.

The term “free cash flow to equity” is sometimes used instead of residual income. Free cash flows to equity are the net of cash flows from operations minus cash flows from investing plus any net borrowing. It is the cash remaining each year after paying for the replacement of depreciated assets and asset growth. If a company only invests in projects with positive net present values, this amount should be what is paid out as dividends as it is not needed by the company.

-

Managed Dividends Theory

Investors prefer constant dividends for planning purposes and falling dividends signal poor company performance in the future. Dividends are only increased if it is felt they can be sustained in a downturn. Companies attempt to maintain a record of constantly increasing dividends to maintain investor confidence.

Dividends are kept intentionally low to maintain financial flexibility, which is the ability to deal with unforeseen operating problems and to exploit unforeseen investment opportunities quickly. Companies in cyclical, growth or highly competitive industries are especially concerned about financial flexibility. Dividends will only be reduced in financial emergency so companies may use excessive amounts of debt or even delay positive net present value projects to maintain the dividend level.

Extra or special dividends can be paid if the company has surplus cash but does not feel it can maintain that dividend level. Extra or special dividends may be perceived as regular dividends if they are paid too often, and could hurt the share price if they are discontinued. Stock repurchases can be used to prevent this, as they are viewed as one-time events.

Which Dividend Theory is Right?

All four dividend theories have an important role in helping to explain changing corporate dividend policies over a business’s life cycle.

Exhibit 4: How Dividend Policies Change over the Business Life Cycle

-

Long-Term Horizon

- Residual Dividend Theory:

- Dividend levels increase as companies move through the development, growth, expansion, and maturity phases of the business life cycle since a declining portion of their earnings is needed to fund operations.

-

- Clientele Effect:

- A firm’s shareholder composition changes from those wanting capital gains in the growth and development phases to those wanting dividends in the expansion and maturity phases.

Short-Term Horizon

- Managed Dividends Theory:

- Dividends are managed so they grow at a steady rate to inspire investor confidence and are kept low enough to maximize financial flexibility. Stock repurchases are used to avoid increasing regular dividends until the company is sure a higher dividend level can be maintained.

-

- Signaling Theory:

- Dividend cuts are avoided due to the negative impact they have on investor confidence and the share price. A steadily increasing dividend reflects positively on a company’s performance.

Warning Signs of Future Dividend Declines

Lowering dividends should be avoided as it typically has a negative impact on a company’s share price. Equity analysts who follow companies view the following as possible warning signs that the regular dividend is not sustainable and will be reduced in the near future:

- Company is borrowing excessively to finance its dividend.

- Dividend payout or yield ratios are higher than the average of previous years or the current industry average.

Dividend payout and yield ratios should include both regular dividends and share repurchases to properly measure a company’s payout level.

1.6 | Dividend Policy in Practice

Industry research shows that companies are divided into two groups based on their dividend policies. The first group consists of the largest companies who are very profitable and pay large and growing dividends. The second group consists of smaller companies who pay no dividends because they are either 1) experiencing financial difficulties or 2) are growth companies that are substituting stock repurchases for dividends (DeAngelo et al., 2004).

A survey of the managers of these two groups (Brav et al., 2005) indicates the following:

- Maintaining current dividends is critical to dividend paying companies because the market penalizes dividend cuts very harshly. Only companies with stable and consistently increasing earnings will initiate or increase their dividend. Dividends are only reduced in extreme cases.

- Instead of trying to maintain a constant dividend payout ratio in the long-term, companies are instead focusing on just maintaining their current dividend and ensuring they have sufficient funds to meet their liquidity and investment requirements. They will not raise dividends until these requirements are met.

- Non-dividend paying companies are very reluctant to initiate regular dividends because of their reduced financial flexibility. Most dividend paying companies regret ever beginning to pay a dividend and the high amounts they are committed to paying.

- Retail and institutional investors do not have a preference between stock repurchases and dividends—taxes do not appear to be an important factor in establishing a dividend policy.

Most managers prefer to rely on stock repurchases exclusively to increase their financial flexibility. In their view, stock repurchases:

- Are not perceived by investors as permanent and can be reduced as needed without market penalty, although once a stock repurchase plan is announced publicly, investors feel it should be completed.

- Make having sufficient capital to finance changing investment opportunities the focus of the business and not funding the dividend—cash is distributed only when profitable projects are not available.

- Ensures that expensive external equity financing is not used to fund dividends but only profitable investment projects.

- Can be used to make money for investors by timing the equity markets.

- Can be used to raise earnings per share, increase or support the share price, or offset stock option dilution.

- Can be used to distribute excess, low-yielding cash balances to shareholders in order to reduce agency costs.

It is expected that the use of stock repurchases will continue to increase as managers place even greater emphasis on financial flexibility.

1.7 | Dividend Policies at Canadian Companies

All companies have unique dividend policies that are influenced by many factors. To examine the policy of a specific firm, analysts should consult the investor relations or corporate information section of their company website. Here a company provides important financial information to its different stakeholders through its annual report, annual information form, and management information circular. These documents can also be found on the System for Electronic Data Analysis and Retrieval (SEDAR) website sponsored by Canada’s securities regulators. In the U.S., similar reports are available on the company’s website or through the Electronic Data Gathering Analysis Retrieval (EDGAR) system hosted by the U.S. Securities Exchange Commission (SEC). By reviewing two companies, Canadian Tire and Lululemon Athletica, students can see examples of the two groups of companies (those that pays dividends and those that do not) described in the previous section.

Canadian Tire Corporation

Canadian Tire Corporation (CTC) is a preeminent Canadian institution consisting of a family of businesses divided into three operating segments. The retail segment is the largest with such famous brands as Canadian Tire, Canadian Tire Gas, Mark’s, PartSource, Helly Hansen, and Sportcheck. CTC also operates a real estate investment trust (REIT) segment that owns the stores and distribution centres in its retail unit. The financial services segment offers credit cards, insurance, warranties and other financial services to its customers and the dealers who operate many of its stores. CTC has chosen to focus primarily on Canada because of past difficulties entering the U.S. market.

Exhibit 4: Select Financial Information for CTC

| 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|

| Share price (CAD) | 147.37 | 165.62 | 131.28 | 106.34 | 107.34 |

| Net income (CAD million) | 692.1 | 735.0 | 669.1 | 659.4 | 604.0 |

| Normalized earnings (CAD million) | 777.5 | 735.0 | 669.1 | 659.4 | 632.0 |

| Dividends (CAD million) | 239.6 | 193.0 | 170.3 | 162.4 | 154.1 |

| Debt ratio (%) | 69 | 64 | 63 | 61 | 61 |

| Basic shares outstanding | 64,887,724 | 68,678,840 | 72,360,303 | 76,151,321 | 78,960,025 |

| Dilutive shares outstanding | 65,062,581 | 68,871,847 | 72,555,732 | 76,581,602 | 79,612,957 |

| Basic EPS (CAD) | 10.67 | 10.70 | 9.25 | 8.66 | 7.65 |

| Diluted EPS (CAD) | 10.64 | 10.67 | 9.22 | 8.61 | 7.59 |

| DRIP (no. of shares) | 73,010 | 60,785 | 68,069 | 65,760 | 62,357 |

| DRIP (CAD million) | 11.9 | 9.4 | 9.3 | 8.3 | 6.9 |

| Repurchases (no. of shares) | 3,661,111 | 4,318,005 | 3,382,275 | 3,450,981 | 2,600,000 |

| Repurchases (CAD million) | 588.9 | 659.30 | 449.4 | 434.6 | 290.6 |

| Basic DPS (CAD) | 3.43 | 2.47 | 2.18 | 2.00 | 1.79 |

| Diluted DPS (CAD) | 3.42 | 2.46 | 2.17 | 1.99 | 1.78 |

| Dividend payout ratio (%) | 29 | 23 | 24 | 23 | 22 |

| Dividend and stock repurchase payout ratio (%) | 103 | 112 | 89 | 88 | 67 |

Dividends are paid at the discretion of the board of directors who base their decision on CTC’s “current cash position, future cash requirements, capital market conditions and investment opportunities.” The company pays a regular cash dividend each quarter which has increased continuously over the past 20 years. In November 2017, the company announced its goal to maintain a dividend payout ratio of 30% to 40% of normalized earnings going forward, which was increased from 25% to 30%. Normalized earnings provide users with a truer measure of income by eliminating all non-recurring items from net income.

Computershare is CTC’s transfer agent who maintains a record of the number of shares each investor owns and distributes their dividends each quarter. CTC’s share price has increased from CAD 8.15 in January, 1995 to CAD 147.37 in January, 2018. No stock splits, reverse stock splits, or stock dividends were used to keep the share price in a preferred trading range.

CTC offers a DRIP to all Class A Non-Voting shareholders who are Canadian residents. They can purchase additional stock at the average share price for the five days preceding the payment date−fractional shares (up to 3 decimal places) are awarded. The DRIP does not offer share price discounts nor an OCP feature so investors can buy additional shares. Shareholders can leave the DRIP at any time as long as they inform the transfer agent by the cut-off date just prior to the date of payment each quarter.

Under a NCIB with the TSX, CTC regularly announces stock repurchase plans each November that are to be completed by the end of the following fiscal year. Recent plans have had a 100% completion rate and CTC also repurchases additional shares as an anti-dilutive measure to negate the effect of new shares issued under the company’s share-based compensation plans. Executives have the option of receiving a cash payment equal to the difference between the share price and a stock option’s exercise price, so few new shares are actually issued.

Some of CTC’s trust indentures relating to its medium-term notes place restrictions on the size of its dividend payments, but none of these conditions currently apply.

Overall, CTC is a mature company with stable net income that increased at a modest 3.5% compounded annual growth rate (CAGR) over the five-year period ending in 2018. Although it has made a number of major acquisitions recently, such as Helley Hansen, the company still generates sizeable cash surpluses that are not needed to finance its growth. CTC is wisely returning these funds to its shareholders to reduce agency costs by steadying increasing the regular cash dividend and announcing a higher payout ratio range of 30% to 35%. In addition, CTC has returned surplus cash by repurchasing a large number of shares each year. Some additional shares have been issued under a DRIP but the funds raised are very modest compared to the size of the repurchases. The result is that CTC is paying out over 100% of its normalized earnings if both the regular cash dividends and share buybacks are considered. These high stock repurchases are not sustainable, but CTC is using them to raise their financial leverage to the optimal level. Its debt ratio has risen from 61% to 69% from 2014 to 2018, which now approximates the ratio at some of its comparable companies such as Walmart at 67% or Target at 73%. CTC has maintained its financial flexibility by not committing to higher regular dividends and using stock repurchases instead. They are also sending a positive signal to the market concerning the company’s performance with its rising earnings and dividends per share and sizeable stock repurchases.

Lululemon Athletica

Lululemon is a “designer, distributer, and retailer of healthy lifestyle inspired athletic apparel and accessories ” headquartered in Vancouver, Canada that first went public in 2007. It targets women, men, and female youth under the Lululemon and Ivivva brands using an increasing number of company-owned stores and expanding on-line presence. The company operates primarily in the U.S. and Canada, but it is also growing internationally, particularly in Australia, China, and the United Kingdom.Lululemon has built a fervid reputation for stylish and high-quality products among its customers, although some critics say the company is cult-like in its human relations and marketing practices and that its products are overpriced. The keys to its success have been a passionate and motivated sales team; making all customers feel great about themselves regardless of their level of fitness; an innovative design team that creates practical new products based on extensive customer feedback; technically advanced fabrics; and outsourcing of all production.

Exhibit 5: Selected Financial Information for Lululemon

| 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|

| Net income (USD thousands) | 483,801 | 258,662 | 303,381 | 266,047 | 239,033 |

| Dividends (USD thousands) | 0 | 0 | 0 | 0 | 0 |

| Basic shares outstanding | 133,413,000 | 135,988,000 | 137,086,000 | 140,365,000 | 143,935,000 |

| Dilutive shares outstanding | 133,971,000 | 136,198,000 | 137,302,000 | 140,610,000 | 144,298,000 |

| Basic EPS (USD) | 3.63 | 1.90 | 2.21 | 1.90 | 1.66 |

| Diluted EPS (USD) | 3.61 | 1.90 | 2.21 | 1.89 | 1.66 |

| Repurchases (no. of shares) | 4,900,000 | 1,900,000 | 500,000 | 5,000,000 | 3,700,000 |

| Repurchases (USD thousand) | 598,340 | 100,261 | 29,327 | 274,193 | 147,431 |

| Stock repurchase payout ratio (%) | 124 | 39 | 10 | 103 | 62 |

Lululemon is a growth company whose sales increased at a CAGR of 19.3% over the five-year period ending in 2018. Instead of paying regular cash dividends, Lululemon distributes all of its surplus cash using stock repurchases to enhance its financial flexibility. Not only does Lululemon need this latitude to fund the high R&D, training, and capital expenditures necessary to support its rapid growth, it must also deal with greater uncertainty due to intense industry competition, rapidly changing fashion trends, and unstable demand stemming from selling higher-priced, consumer-discretionary items. To further improve its financial flexibility, Lululemon maintains a significant amount of unused borrowing capacity by not issuing any long-term debt and keeping a 5-year, backup revolving credit agreement for financial emergencies.

Besides increasing financial flexibility, Lululemon uses stock repurchases for a number of other reasons. They offset the dilution of earnings per share caused by the issuance of a large number of new shares under the company’s stock-based compensation plans. They also are used to signal to the market that its share price is undervalued and to time the equity markets to benefit their current shareholders. Finally, as a growth company, Lululemon’s clientele likely consists of a significant number of long-term investors who do not want a cash dividend but prefer to remain invested and defer taxes.

The value of Lululemon’s open-market stock repurchases vary markedly each year depending on its cash flow needs. All plans are approved by its board of directors and are in accordance with the U.S. Securities Exchange Act as Lululemon is an U.S. listed (NASDAQ) company. The timing and number of shares repurchased depends on market conditions, eligibility to trade, and other factors. The company has a record of completing all its stock repurchase plans and does go to the board to increase the amount of any announced buybacks if economic conditions warrant it.

After going public in 2007, Lululemon implemented a 2-for-1 stock split in 2011, but has not conducted any splits since. Its share price has risen from under CAD 20 in 2007 to approximately CAD 165 in 2019, which indicates that the company does not have a preferred price range for its share.

1.8 | Exercises

-

Problem: Stock Transactions

Elmer Ltd. has a capital structure consisting of 1,250,000 common shares. Each share currently trades at CAD 86 on the TSX. The company is considering three alternative changes to its capital structure:

- Implement a 3-for-1 split

- Issue a 10% stock dividends

- Implement a 1-for-2 reverse split

Heather Topley currently owns 50,000 shares in Elmer and is contemplating what effect these changes would have on her percentage ownership in the company and the value of her investment.

REQUIRED:

- What is Topley’s percentage ownership in Elmer under the three alternatives?

- What is the value of Topley’s investment under the three alternatives?

- Could any of these alternatives lead to an increase in the value of Topley’s investment? Explain.

-

Problem: Factors Influencing Dividend Decisions

- Smithers Ltd. is growth business that is controlled by its founder who owns 55% of the company’s shares.

- Rampart Industries’ debt ratio is 20% lower than the industry average.

- Stella Inc. operates in a cyclical industry with high working capital and capital spending requirements.

- Dexter Enterprises is a small technology start-up that recently went public. Its assets largely consist of patents and deferred product development costs.

- Rascal Co.’s loans stipulate that it must maintain a current ratio above 2.0.

- Abigale Ltd. recently paid equity issuance costs equal to 12% of the capital raised.

- Oscar Industries maintains a large portfolio of short-term investments as a contingency fund for financial emergencies.

- Waterson Inc.’s share is currently undervalued due to a number of plant closings but their prospects are still bright with four major projects under development.

- Tutor Ltd.’s largest shareholder is an endowment fund that supports the members of a wealthy Ontario family.

- Wilson Co. is a technology firm whose shareholders consist largely of long-term investors that are saving outside of an RRSP or TFSA.

- Dempsey Consolidated may have the opportunity to participate in a number of oil and gas joint ventures due to a recent decline in commodity prices that has caused other firms to re-think their investments.

- Grison Associates is a mature service business that is largely sheltered from international competition.

REQUIRED:

- Indicate whether the company should favour paying higher or lower dividends in each of the above scenarios.

-

Problem: Different Dividend Policies

- Hecla Ltd. is a mature company operating in a cyclical industry. After a protracted period of strong earnings, the company wants to distribute its surplus cash to its shareholders but is concerned about the ramifications if it raises its dividend now but is then forced to reduce it in the next downturn.

- Jefferson Inc. sold a major product line as part of a corporate reorganization. The company has no use for these one-time funds at this time.

- Jasmine Industries has surplus cash that it plans to distribute to its shareholders in the coming months. Its shareholders consist primarily of institutional investors, including pension plans and endowments funds.

- Big Sky Entreprises is a recent start-up that has grown quickly using its retained earnings and new equity raised from venture capitalists.

- Floyd Co. wishes to eliminate its regular dividend to help finance a new growth opportunity but needs to communicate to shareholders that its future prospects are good and it will continue paying dividends once this project is completed.

- Hanna Ltd. needs to reduce its high equity issuance costs without reducing its current dividend.

- Able Co.’s share typically trades in the CAD 35 to CAD 50 range. After a period of rapid growth, the share price has risen to CAD 110.

- Due to intense industry competition, Lincoln Industries’ share price has fallen to CAD 1 from its preferred price range of CAD 25 to CAD 30. The company feels that the price decline is permanent.

- Devers Ltd. is liquidating a number of its mining properties and is returning share capital to investors.

- Helmond Enterprises’ CEO resigned after being accused of insider trading by the Ontario Securities Commission.

- Crandle Inc. has issued a large number of stock options to its senior executives that are expected to cause significant earnings per share dilution in the next annual report.

- Ramone Consolidated has a large cash reserve that is being invested in short-term debt securities until the company can complete a number of acquisitions in the coming year. It hopes to expand into a new industry to diversify its sales.

- Simpson Ltd. is considering implementing its first regular cash dividend but finds that investment opportunities in its industry are erratic.

- Cadence Co. feels its shares are undervalued and it wants to communicate this to its investors.

- Edson Inc. plans to increase its debt ratio to the optimal level by repurchasing a large block of its shares at the best price possible.

- Atlantic Enterprises wants to immediately increase its earnings per share so executives can attain their earnings targets and claim the maximum yearend bonuses.

- Cleveland Co. plans to announce a stock repurchase to increase its share price but needs the flexibility to freely time the equity markets and purchase a lessor or greater number of shares than announced depending on economic circumstances.

- Henderson Inc. wants to establish a loyal clientele of long-term retail investors.

REQUIRED:

- Describe the most appropriate action to take in each of the above scenarios.

-

Problem: Dividend Policy for a Mature Firm

Maple Leaf Ltd. is a manufacturer of auto parts with a number of plants in eastern Canada. The company has the following characteristics:

- Mature company with large free cash flows to equity, modest growth opportunities, and high cash balances.

- Free cash flows to equity are subject to considerable cyclical variations.

- All positive net present value projects have been undertaken.

- Debt ratio approximates the industry average.

- Owned primarily by another auto parts producer and two pension funds.

- Managers own a limited number of shares.

REQUIRED:

- Describe an appropriate dividend policy for Maple Leaf Ltd.

-

Problem: Dividend Policy for a Growth Firm

Agnes Company is a hi-tech firm specializing in the production of hand-held GPS devices. The company has the following characteristics:

- 5-year old start-up with significant free cash flows to equity and high growth prospects.

- No dividend paying history.

- Limited ability to borrow from financial institutions because of the intangible nature of the company’s collateral and the uncertain and competitive nature of the industry.

- Investors are primarily the founding owner, a local angel investor, and managers.

- Local angel and some of the other investors are looking to cash out using an initial public offering.

REQUIRED:

- Describe an appropriate dividend policy for Agnes Company.

-

Problem: Change in Dividend Policy

VAC is a large cap company trading on the Toronto Stock Exchange. Approximately five years ago, the company began a major expansion into wind and solar generators from its base in the production of aviation parts (a mature industry) in order to invest excess cash. Sales have continued to grow modestly, but free cash flows have declined and are quite erratic due to operational difficulties in the new units and the cyclical nature of the industries.Approximately 60 per cent of VAC’s shares are owned by various company pension plans, but few shares are owed by board members and the board’s compensation committee makes limited use of stock options as senior executive compensation. The company’s share price has fallen dramatically over the last five years due to a falling rate of return on equity resulting from poor profitability in its new units. Also, with the expansion, the company’s debt ratio has risen to well above the industry average.VAC has reduced its high payout ratio to approximately 5 per cent over the last five years to help finance the expansion, but its investors are now complaining.

REQUIRED:- Analyze VAC’s current dividend policy and make recommendations, if any, for change.

Brav, A., Graham, J., Harvey, C., Michaely, R. (2005). Payout policy in the 21st Century. Journal of Financial Economics, 77, 483-527.

DeAngelo, H., DeAngelo, L., Skinner, D. (2004). Are dividends disappearing? Dividend concentration and the consolidation of earnings. Journal of Financial Economics, 72, 425-456.