Module 4: Working Capital Management

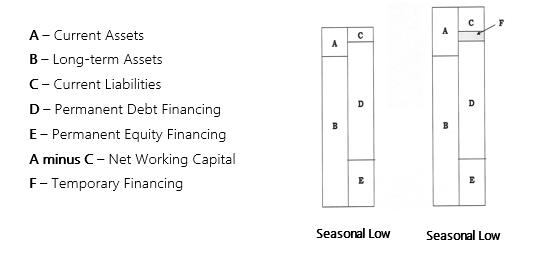

As discussed in the Module: Maturity Matching, companies have two major classes of assets, long-term assets and net working capital (NWC). Long-term assets include property, plant, and equipment and possibly intangible assets like patents, copyrights or licenses and their value is relatively stable throughout the year. Because these assets have longer lives, permanent debt and equity are used to match the maturities of these assets with their funding.

NWC is equal to current assets consisting primarily of cash and cash equivalents, accounts receivable, and inventory minus current liabilities which is mostly made up of accounts payable. NWC can vary considerably throughout a year depending on the seasonality of a business, but it never falls below the level at the seasonal low. As a result, NWC at the seasonal low is considered a long-term asset and is funded with permanent financing as well. During the seasonal highs, temporary financing is used to fund the seasonal build-up in NWC.

This module looks carefully at how a company manages its investment in NWC. The goal is not to minimize NWC but to maximize long-term profits by optimizing the level of current assets and liabilities. It may be more profitable to carry additional inventory, implement more generous credit policies, or pay creditors sooner even though they all raise the level of NWC. Once the optimal level of NWC is determined, a company must select the most cost-effective sources of temporary financing and invest any cash surpluses wisely.

4.1 | Managing Cash

Companies hold cash so they have sufficient funds to pay their obligations as they come due (called the transaction motive). They also hold cash as a reserve for financial emergencies (called the precautionary motive) or to quickly take advantage of investment opportunities (called the speculative motive). Cash is a difficult asset to manage because there are so many different cash inflows and outflows to consider. As discussed in Module: Financial Planning and Growth, cash inflows come primary from sales but also from debt and equity financing, interest and dividend revenue, maturing investments, tax refunds, and transfers from subsidiaries and joint ventures. Outflows relate primarily to operating expenses like wages and inventory purchases but also to capital purchases, debt repayment, share repurchases, interest expense and dividends, investments in securities, taxes, and transfers to subsidiaries and joint ventures. Estimating these amounts accurately is difficult especially if the company experiences significant seasonal and cyclical variations in sales and input price variability. Cash serves as a buffer against the inability to forecast these cash flows accurately.

Different mathematical models can be used to estimate a company’s target cash balance, but most firms simply rely on their past experience. A number of factors influence the amount of cash a company should hold. These include:

- Firms who have adopted a flexible maturity matching strategy invest their surplus cash in short-term debt securities during seasonal lows. These investments can be sold quickly reducing the need to hold additional cash for speculative and precautionary motives which lowers the target cash balance.

- Businesses with variable cash flows have greater transaction, speculative, and precautionary motives which raises the target cash balance.

- Companies with significant unused borrowing capacity or larger firms who can borrow more easily have lower precautionary and speculative motives which reduces the target cash balance.

A firm’s target cash balance increases as it grows and fluctuates due seasonal and cyclical variations in sales. Once this target is determined, the focus is on managing the available cash effectively. Effective cash management practices typically involve either accelerating cash collections or delaying payments. Before looking at different cash management practices, it is important to understand Canada’s payments system.

Payments System

The Canadian Payments Association (CPA) or Payments Canada is overseen by the Bank of Canada and works closely with banks, credit unions and other financial services providers in clearing and settling financial payments in Canada. Consumers, businesses, and governments continuously purchase items, make investments and transfer funds. Most transactions involve more than one financial institution. Clearing and settlement is how these institutions exchange funds and settle any balances owed. Maintaining public confidence in the payment system is critical to the smooth operation of the Canadian economy.

In 2017, CPA cleared over 21.9 billion transactions worth CAD 9.7 trillion. Electronic forms of payment have grown dramatically, but cash and cheques continue to play an important role in the Canadian payments system despite the higher cost of manually processing these transactions and protecting parties from fraud and theft. Studying three categories of payments helps to identify some important trends.

- Point-of-sale (POS).

- These consumer-to-business (C2B) transactions occur at physical or web-based store fronts and include in-app purchases made in mobile applications on smartphones or other devices. In 2017, there were 16.5 billion POS transactions worth CAD 868 billion. This accounts for 75% of total transaction volume but only 9% of value indicating there are a large number of small transactions.

Exhibit 1: POS Transactions

Payment Type 2012 Volume 2017 Volume 2012 Value 2017 Value Cash or cheques 47% 36% 17% 12% Debit cards 30% 35% 27% 28% Credit cards 22% 27% 55% 58% Prepaid debit cards 1% 2% 1% 2% The use of cash or cheques, primarily cash, is falling by transaction volume, but it is still the most common form of payment. Despite the growth of electronic payment and e-commerce, cash remains important due a core group of heavy users made up of younger, poorer, and rural users and those engaged in the underground economy including criminals.

Debit cards exceed credit cards in volume but not in value indicating they, like cash, are used for small transactions. The increased use of credit cards is supported by the expansion of e-commerce where only credit cards are usually accepted; high credit card ownership in Canada compared to other countries; valuable credit card rewards programs; the rising level of consumer debt in Canada; and the growing use of commercial credit cards for travel and other business expenses. The convenience of contactless debt cards has countered this trend somewhat as has the greater ability to use debit cards for online purchases (Interac Online Debit) or transfers (Interac E-transfer).

High credit card fees charged by card providers are a concern to merchants. The main fee is the bank interchange which consists of a flat amount plus a processing fee averaging 2.0% of the value of the transaction. The processing fee varies by card such as Visa, MasterCard, or American Express. Cards aimed at wealthier clients, commercial clients or those offering travel rewards or cash-back programs charge higher fees. Online, mobile, and card-not-present transactions (phone, mail, or internet) and transactions that are key-entered instead of being swipe through a reader have higher fees. Finally, smaller companies with fewer transactions pay higher fees as do riskier businesses as measured by the Merchant Category Code (MCC) assigned by the issuing bank. Interchange fees for debit cards are much lower than credit cards due to government regulation and are typically not a concern to merchants.

Prepaid debit cards are issued by credit card providers and are loaded with funds. Customers can spend up to this amount or make withdrawals at ATMs, but then must reload the card. These cards, unlike regular debit cards, can be used for online purchases and are excellent for those who do not qualify for a credit card, do not want to share their banking information, want to limit their expenditures, or are worried about credit card loss or theft. The volume and value of prepaid cards remains small. Gift cards are similar to prepaid debt cards except they can only be used at one retailer and cannot be reloaded.

Payment card use has also increased due to the introduction of mobile wallets. Mobile wallet apps or built-in features on some smartphones contain credit card, debit card, prepaid debit card, loyalty card, and coupon information. A merchant’s POS terminal automatically reads this information with near-field communication (NFC) using radio waves. All the customer does is hold their phone or other wearable communication device like a watch near the merchant’s NFC reader. Mobile wallets are useful for merchants that experience high transaction volumes and provide better security than payment cards as smartphones are harder to steal and have better encryption. Mobile wallets can also store additional information including driver’s licences, social insurance numbers, health cards, hotel keys, and tickets.

Other payment systems such as PayPal offer advantages similar to prepaid debit cards. PayPal accounts are connected to either a user’s credit card or chequing account which is useful if they do not qualify for a credit card. Users can transact with other PayPal accounts and engage in e-commerce. Funds are immediately available and they only have to release their banking information to PayPal. They can also send and receive funds internationally and PayPal offers lines of credit for those who need financing.

- Remote Consumer Transactions

- These payments include all non-POS transactions by consumers such a person-to-person (P2P) transfers between families and friends and payments to small traders such as repair people or babysitters. It also includes regular customer-to-business (C2B) transactions such payments for utilities, insurance, loans or leases, membership fees, or taxes. In 2017, there were 1.6 billion remote consumer transactions worth CAD 574 billion.

Exhibit 2: Remote Consumer Transactions

Payment Type 2012 Volume 2017 Volume 2012 Value 2017 Value Cash and cheques 27% 14% 31% 14% Credit cards 21% 25% 9% 8% Online transfers 2% 14% 4% 14% EFT 50% 47% 56% 64% The volume and value of cash and cheque payments are declining rapidly. Most cheque users are older and only write two cheques per month, primarily for rent and P2P transfers or payments. Cheques are being replaced by online transfers particularly INTERAC e-Transfers. For large, time-sensitive domestic and international payments in a variety of currencies, wire transfers using payment systems such as the Society for Worldwide Interbank Financial Telecommunication (SWIFT) are used. These transfers can be initiated face-to-face, by fax or e-mail, or using bank’s website.

Electronic funds transfer (EFT) accounts for the majority of remote consumer transactions using online/mobile banking systems for regular C2B payments. Credit card use is discouraged for these transactions due to high interchange fees.

- Business Transactions

- These payments include business-to-consumer (B2C), and business-to-business (B2B) transactions only and exclude government.Exhibit 3: Value of Business Payments

Payment Type 2017 Value Cash 6% Cheques 13% Debit cards 8% Credit cards 24% Prepaid cards 1% Online transfers 4% EFT 42% Other 2% Businesses have made great progress in adopting electronic payment. These methods, primarily credit cards and EFT, account for 80% of the value of all business transactions. This figure is deceiving as nearly 60% of businesses still use cheques on a regular basis. CPA research indicates that most businesses would move away from cheques further if better electronic payment services were available although, smaller, older businesses were found to be less likely to convert.

Business credit card use is rising due to an established payment system, not having to submit purchase requisitions and expense claims, faster transaction reporting, and the availability of short-term financing. Different types of procurement cards or p-cards are available. Travel and entertainment cards pay for an employee’s expenses when they are “on the road” or hosting clients. Fleet cards pay for gas and repair bills and possibly a driver’s food and lodging. Purchase cards buy inventory, supplies, equipment and other business services. All cards come with limitations on who can use them, how much can be charged, the type of expenditures that can be made, and expiry dates to control fraud. Some cards are limited to just one use (called single use cards) such as paying vendors. Instead of receiving an actual card, companies may only be assigned a billing number to give to suppliers (called a virtual card).

Most EFT consists of simple transactions such as direct deposits for payroll or pre-authorized payments for repetitive transactions. Businesses have been slow in adopting advanced EFT systems using electronic document interchange (EDI) that exchange invoices, payments with detailed remittance data, and messages. EDI is a standardized way of sending business documents like purchase orders, invoices, or bills of lading electronically so different computer systems can understand them. Improved payment products and education are needed, but EFT will continue to grow in importance with future technological innovations.

One recent innovation is real-time (RTP) payment systems that should transform how businesses, governments, and consumers transact with each other using EFT. An RTP system offers a number of advantages:

- 24/7/365 service

- Real-time operation

- nstant fund transfer

- Irrevocable transactions that cannot be changed or reversed

- Improved security

- Transaction data passed with payment

- Messaging

- Global compatibility

RTP systems are attractive to businesses. More data about a transaction is included with the actual payment, and parties can better communicate with each other to request payment or inquire about payment disposition. RTP systems do what current electronic payment systems do, they just do it faster, better and at a lower cost providing much needed competition for existing payment providers. Many merchants offer discounts to consumers to use RTP systems in response to high credit card interchange fees.

Effective Cash Management Practices

Small and medium-sized enterprises (SME) typically deal with just one bank. In contrast, large multinational firms usually have one lead banker that works with them managing their cash operations, but then retain other institutions to provide specialized services such as capital markets, mergers and acquisitions, or risk management. It is very prestigious for a bank to be selected as the lead bank for a large company so competition for these positions is intense. The institution chosen normally leads the lending syndicate that funds the company’s credit facilities.

Large companies have treasury management departments that house their cash management activities. They are responsible for:

- Cash collections and disbursements

- Short-term financial planning

- Raising temporary and permanent financing

- Investing excess funds

- International finance including currency and trade transactions

- Risk management and insurance

Effective cash management practices can be classified into three areas.

- Electronic payment

- Approximately 90% of the value of consumer payments and 80% of the value of business payments are made electronically. This transition should be completed soon, but businesses must concentrate on making the payment system more efficient through the better use of EFT, RTP and other innovations.

- Managing the float

- The net float is the difference between a company’s cash balance according to its books and its bank account. Companies will try to manage the net float so the book balance is less than the bank balance. This will occur if a company pays a supplier by cheque instead of electronically. The expense is recorded immediately reducing the book balance but it will take time for the cheque to get to the supplier (called mail float), be processed by them (called processing float), be cashed and have the funds taken from their account (called settlement float). The total of these periods is called the disbursement float. The company can continue to use this cash in their operations or invest it during this time.When companies receive payments by cheque through the mail instead of being paid electronically, the opposite is true. It takes time for the cheque to arrive, be processed, and then settled before funds are added to the company’s bank account. This is called the collection float. Collections are only transferred from accounts receivables to cash in the company’s books when the payment is received. The payment will likely be settled the same or next day and added to the company’s bank account, so only this short delay will be reflected in the net float. Clearly, if these collections could be received more quickly through the mail and processed faster, the company would be even better off.Managing the float is less important due to increased electronic payment, but cheques still account for a large portion of business transactions by both volume and value. Some options for accelerating collections include:

- Send invoices to customers electronically soon after a sale is finalized and ensure they are accurate to avoid payment delays later on.

- Strictly enforce credit terms.

- For consumers, install in-store POS terminals that support electronic payment and have them use online/mobile banking for other payments.

- For businesses, employ EFT, wire transfers, and e-transfers.

- Quickly process and deposit any cash receipts and cheques.

- If cheques are used, have the customer scan them and send them to the business electronically instead of through the mail or use pre-authorized cheques for regular payments. Pre-authorized cheques do not require a signature and can be originated by the company receiving payment with the appropriate authorizations.

- Contract out collections to service providers with greater expertise.

- Establish “locked boxes” throughout the sales region where customers can mail payments more quickly than sending them to company headquarters. These post office mail boxes are emptied and processed daily by a local bank who transfers the funds electronically to the company’s central bank account. Afterwards, the cheques are scanned or data is taken from them and sent electronically to the business for reconciliation. Less cheque handling also reduces processing costs and gives the company earlier notice of any dishonoured cheques.

- Establish company-owned collection offices throughout the sales region where customers can pay in-person or mail their payments so they can be immediately batched, deposited, and transferred electronically to the company’s central bank account.

To delay payment, companies should:

- Pay on the last day of the cash discount or credit period only.

- Negotiate longer credit terms.

- Pay by cheque instead of electronically.

- Mail cheques from distant locations using remote disbursements.

- Stretch payments beyond the credit period if penalties and interest can be avoided.

- Pay only when creditors call about late payments and not on the due date.

The last three ways to delay payment are unethical, but are still used in practice. To further improve efficiency, many companies outsource the printing and mailing of cheques or the entire cash disbursement function. Fraud detection services are also be purchased. Typically, companies provide their bank with a list of cheques and the bank only cashes those with the correct serial number, name, and amount.

- Cash concentration

- Larger companies have multiple offices, branches or stores and each location typically has a separate account at a local bank to deposit cash and cheque receipts using a designated business teller, night depository, armoured car service, or “smart safe.” Companies also use remote deposit capture (RDC) so cheques can be scanned by the business and deposited electronically. A “smart safe” is a safe provided by an armoured car service that is kept on a business’s premises. Deposits are made into it as funds are received and the company is given immediate credit for these deposits. The advantage is armoured car services do not have to pick up their deposits as frequently lowering operating costs.A business’s target cash balance can be reduced by having their bank automatically transfer the funds at their local bank branches to one centralized account at company headquarters. This allows the company to maintain a smaller cash balance overall, reduce the use of their overdraft facility, and more easily identify excess cash balances that they can be used to pay down debt, take advantage of supplier discounts, or invest in short-term securities. Investing in large amounts also helps companies meet the sizeable minimum deposit requirements for some investments. Global cash concentration is more complex as businesses utilize a number of banks and operate in multiple legal jurisdictions with different currencies. In most jurisdictions, funds can be transferred to one central account in another country, but the different entities must account for the transfer as an intercompany loan and pay a market interest rate on the amount borrowed.Firms use zero-balance accounts to better control certain expenditures such as payroll or supplier remittances. A separate account is established to process each type of payment and funds are only transferred to that account from a central account as needed. Because the disbursements made each day are uncertain, extra cash must be maintained as a safety stock in the central account. By having just one safety stock in the central account instead of each of the zero-balance accounts, the company is able to maintain a lower safety stock overall.

Investing Temporary Cash Surpluses

Companies often hold more cash than is required to meet their daily transactional, precautionary, and speculative needs. A business may be:

- Following a flexible maturity matching strategy where permanent financing is used to finance seasonal increases in NWC but then remains idle for the rest of the year.

- Accumulating cash to fund a major expenditure, interest or principal payment, or semi-annual dividend.

- Investing the proceeds from a stock or bond issue until they are used to finance a capital project.

- Establishing a contingency fund to protect the company against unforeseen events such as a failed product launch or to take advantage of unexpected opportunities such as a business acquisition.

A business chequing account pays little or no interest, so any surplus cash should be carefully invested to earn a competitive return. Since these funds will soon be needed in operations, a company should follow a conservative strategy and invest in a diversified domestic portfolio of short-term, fixed income securities that does not put the principal at risk. Holding a variety of high-quality government and corporate issues from different regions of the country helps minimize credit or default risk. Their short maturities also greatly reduce interest rate risk as rate changes have little effect on their market value. Liquidity risk is low since these investments mature quickly, are issued by large institutions, and often have active secondary markets if a company needs to sell early. Finally, buying securities issued in CAD eliminates exchange rate risk.

The money market consists of a variety of fixed income securities with maturities of less than a year although most have lives of just a few months. The main securities include:

- Treasury bills (T-bills)

- T-bills are issued by federal and provincial governments in Canada to help finance their short-term cash flow needs. The Bank of Canada serves as the fiscal agent for the Government of Canada and issues T-bills with maturities of three, six and twelve months at a weekly auction to a group of approved investment dealers and distributors. These dealers and distributions are major financial institutions who resell the T-bills to investors in amounts ranging from CAD 5,000 to CAD 100,000 making them accessible to smaller investors. T-bills are sold at a discount and their yields increase with maturity. An active secondary market exists so they can be redeemed very quickly if necessary. Provincial government T-bills offer slightly higher yields compared to federal government T-bills with minimal additional default or liquidity risk making them an excellent investment alternative. T-bills denoted in U.S. dollars can be purchased as part of currency hedging strategy but are sold in CAD 100,000 minimum amounts.

- Term deposits and certificates of deposits

- These deposits are available in minimum denominations ranging from CAD 1,000 to CAD 5,000 from Canadian financial institutions in USD, CAD, and GBP for periods of 1 day to 10 years making them suitable for small businesses. Interest on deposits that mature in less than a year is paid at maturity, while longer-term deposits can have their interest paid semi-annually, annually or compounded over the life of the investment and paid at maturity. Deposits may be redeemable or non-redeemable but redeemable deposits earn a lower return because of the greater flexibility they provide investors. Certificates of deposit differ from term deposits in that an actual certificate is issued that can be pledge as collateral for others loans or sold in a secondary market. Overnight deposits allow companies to invest surplus balances in their chequing accounts from the end of business day to the start of the next business day. These deposits are secured by the Canadian Deposit Insurance Corporation (CDIC).

- In addition to the chartered banks, other financial institutions including credit unions, trust companies, and mortgage companies offer term deposits and certificates of deposits as do direct or virtual banks. Direct banks operate without a branch network relying on mobile phones, Web, ATMs, or postal system to conduct business. Their reduced overhead allows them to offer more competitive rates while still providing CDIC protection.

- Bearer deposit notes

- These notes are issued by financial institutions to more sophisticated investors to finance their operations. They are sold in minimum investment of CAD 100,000 for terms of up to 365 days. The notes are unsecured and subordinate to the financial institution’s other debt and are either sold at a discount or as interest-bearing securities. Notes are sold through banks, investment dealers, and securities brokers and are not insured by the CDIC.

- Commercial paper, asset-backed commercial paper, sales finance paper, and bankers’ acceptances

- As will be discussed in the section on sources of temporary financing, these short-term investments are sold at a discount by large, credit worthy corporations and trusts for periods of under a year.

- Short-dated bonds

- These are long-term bonds with less than a year remaining till maturity. They have low interest risk due to their short remaining maturity so they are an alternative for investors who want to earn a higher return than T-bills or commercial paper. Publicly-traded bonds or debentures have an active secondary market if a company requires quick access to its cash and they are rated by the different credit rating agencies.

- Repurchase agreements

- These agreements (also called repos) are commonly used by security dealers to finance their inventories of marketable securities such as stocks or bonds. Instead of pledging these securities as collateral for a loan, dealers raise short-term financing by selling them at a modest discount while agreeing to repurchase them at face value in the very near future. By buying the collateral, investors are in a stronger financial position if difficulties occur. To the investor buying the securities and then selling them back, these agreements are called reverse repos. Repos are usually sold in CAD 100,000 multiples on a call or fixed-term basis although overnight agreements are the most common.

- Euro deposits

- These deposits are made by foreign investors in European banks and are denoted in Euros. Many European banks offer above market returns to attract needed capital. Euro deposits expose companies to exchange rate risk so they are not recommended for funds needed in operations, but they may be acceptable if used as part of a currency hedging strategy. Euro deposits are offered for varying periods of time and are sold in minimum denominations of EUR 10,000 or more. They are generally non-redeemable and have a limited secondary market. The popularity of Euro deposits has declined due to the European Central Bank’s negative interest rate policy.

- Money market funds (MMF)

- These funds are offered by major financial institutions who pool the surplus cash of small investors who cannot access most money market securities such as commercial paper on their own because of large minimum investments. MMFs also offer more professional management and greater diversification at a very modest management fee. These investments can be purchased as shares in a mutual fund or exchange traded fund (ETF). Shares in ETFs can be redeemed more quickly because they trade daily on stock exchanges. ETFs also offer lower management fees making them the best option for small investors.

Under IFRS, investments of surplus cash are classified as cash and cash equivalents, short-term investments, or long-term investments. Cash consists of any cash on hand plus demand deposits such as chequing accounts. Cash equivalents are “short-term, highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value” with an original term to maturity of three months or less. Short-term investments are similar to cash equivalents but they have an original term to maturity of more than three months and a remaining term to maturity of less than a year. Both cash and cash equivalents and short-term investments are both classified as current assets as they will mature within the year. Other securities with a remaining term to maturity of greater than a year are classified as long-term investments.

Exhibit 4 – Money Market Rates

| Treasury bills | |

| 3 months | 1.63% |

| 6 months | 1.67% |

| 1 year | 1.67% |

| Term deposits | |

| 3 months | 0.35% |

| Bankers’ acceptances | |

| 1 month | 1.82% |

| 3 months | 1.84% |

| Overnight repos | 1.75% |

| Euro deposits | Negative |

| Money market fund | 1.63% |

| Effective September 2019 |

Effective Cash Management Tip

Returns on money market securities are low because of their short durations and the high creditworthiness of the issuing institutions. Before investing in the money market, companies should always use their surplus cash to reduce their line of credit and other forms of short-term financing which generally charge a much higher interest rate. The company should also approach its suppliers to see if any are willing to give a discount on their accounts payable if they pay early. This discount will likely exceed the return the company can earn on any money market instrument and will provide financial assistance to a valued supply chain member as the discount will likely be less than what they are paying on their line of credit or other forms of short-term financing.

4.2 | Managing Accounts Receivable

Companies can adopt restrictive or more lenient credit policies. Implementing more generous credit terms and tolerant collection practices increases sales, but leads to higher financing charges for inventory and accounts receivable, greater bad debts and more early payment discounts. Mathematical models can be used to estimate the effects of offering different terms, but companies must actually offer them to determine exactly how customers and competitors will react and whether the additional profits generated are sufficient to cover the added costs. Reducing credit terms and being more forceful with collections may be the best option for improving a company’s bottom line.

Types of Credit

Credit extended to companies is trade or commercial credit, while individuals receive consumer credit. These types of financing can be offered different ways:

- Open account

- Customers must pass an initial credit check and, if approved, they can make purchases without any additional credit applications or purchase contracts. Companies will usually issue an invoice for each purchase and provide monthly statements. As long as the customer adheres to the credit terms, they will continue to receive financing subject to their approved credit limit and passing periodic credit reviews. All customer payments are applied to specific invoices after adjustments are made for discounts, allowances or returns which is referred to as an open-item system. Open accounts are the most common form of trade credit for business-to-business transactions. Promissory notes may be required for large purchases or if collection difficulties are expected to make these claims more easily enforceable in court if problems arise.

- Installment credit

- Customers sign a formal contract where they agree to pay for a purchase in blended payments of interest and principal over a specified time period at a set interest rate. Installment credit is an important form of consumer credit that is used to finance the purchase of costly consumer durables such as automobiles. Consumers must pass a credit check each time a product is purchased. Interest earned on installment credit by companies is usually a major source of revenue.

- Revolving credit

- A customer is assigned a credit limit based on an initial credit investigation. They are free to make purchases as long as they do not exceed the credit limit and make the minimum payments each month. Additional payments can be made at the customer’s discretion and interest is charged on the outstanding balance during each period. All payments are applied to the balance of the account and not individual transactions which is referred to as a balance-forward system. Revolving credit is commonly extended to consumers using credit cards. Open loop credit cards like Visa, MasterCard, or American Express can be used anywhere while closed loop cards such as retail store or gas cards can only be used at the card sponsor’s stores or service stations. Some closed loop card issuers have formed alliances with other companies to accept each other’s cards. Others firms offer cards in association with the major open looped card companies but place their own names and logos on the cards.

- Letters of credit

- Commercial letters of credit are used in international trade when an exporter is unwilling to extend normal trade credit to an importer because of a lack of familiarity with the customer. The importer requests that its bank provide a letter of credit to the exporter’s bank that guarantees payment. With this guarantee, exporters may still demand immediate payment from the importer or they may be willing to extend normal trade credit. Exporters can sell letters of credit at a discount early to raise needed cash or use them as collateral in a loan or other business transactions.

Credit Terms

As discussed in Module 2: Maturity Matching, trade credit terms can take many forms.

- Net 30

- Payment must be received within 30 days from the date of the invoice although other payment periods such as net 60, net 90 or net 120 are common. The longer the payment period, the greater the benefit to the customer but the higher the cost to the supplier.

- 2/10, Net 30

- Payment must be received within 30 days from the date of the invoice, but if a company pays within 10 days from the date of the invoice they receive 2% off the amount owed. The early payment period and early payment or cash discount vary depending on industry competition. The early payment discount is usually fixed although some companies use dynamic discounting where the discount increases if the customer pays earlier than the end of the discount period.

- 2/10, Net 30, EOM

- Payment must be received within 30 days from the end of the month (EOM), but if a company pays within 10 days from the end of the month they receive 2% off the amount owed. EOM is used when customers purchase inventory regularly. Having the same start date for credit terms reduces administrative costs as all of a customer’s orders can be processed together. A start date of the middle of the month (MOM) is also used.

- 3/15, Net 60, ROG

- Payment must be received within 60 days from the receipt of goods (ROG), but if a company pays within 15 days from the receipts of goods they receive 3% off the amount owed. ROG is common when shipping times for goods are long and regular credit terms will likely be over before the goods arrive. Businesses are not comfortable paying for products that they have not received and may need time to resell the product before they can pay.

- 2/10, Net 30, January 1

- Payment must be received within 30 days from a specified date which is not the invoice date, but if a company pays within 10 days of the specified date they receive 2% off the amount owed. This is referred to as seasonal dating and is common in industries with variable demand where customers need help financing large inventory buildups for seasonal items like toys at Christmas or greeting cards on Mother’s Day. Customers are not required to pay until the seasonal high has past and the products have been sold to the final consumer. Seasonal dating also encourages customers to buy earlier so suppliers can better forecast sales.

- Cash terms

- No credit is extended but customers are still given a week or more before they must pay. These terms are common for new customers who have not yet been approved for regular trade credit.

- Cash on delivery (COD)

- Payment must be received when goods are delivered by the supplier because of their unwillingness to provide trade credit due to a customer’s poor payment history. Putting existing customers on COD for non-payment may lead to bankruptcy as they generally need time to sell the product before they can pay a supplier.

- Cash before delivery (CBD)

- Payment must be received prior to the goods being shipped by the supplier. CBD may be adopted if the supplier does not want to risk having to absorb the cost of shipping and returning products if the customer does not pay.

- Consignment

- A supplier or consignor ships goods to a customer or consignee who does not pay for the product until it is sold. The consignee receives a sales commission for selling the product and forwards the remaining proceeds to the consignor who retains ownership until final sale to improve the quality of their collateral.

- Bill-to-bill

- No payment date is specified, but payment for past purchases must be received before any new shipments are made to the customer.

Length of Credit Terms

Credit terms vary by industry but are typically between 30 and 120 days. A number of factors influence the length of terms. These include:

- Customers with extended operating cycles receive longer terms as they need more help financing products until they are sold to the end consumer.

- Wholesale customers receive longer terms than retail customers because they are further upstream in the supply chain and more removed from final payment by the end consumer.

- Companies entering new territories or selling new products offer longer terms to attract customers.

- Sales of perishable items receive shorter terms as the collateral loses its value very quickly.

- Seasonal items sold in advance of sales peaks receive extended terms as it is longer to the final sale.

- Companies selling slow moving products and excess or obsolete inventory offer longer credit terms to encourage customers to buy these low turnover items.

- Companies operating in competitive markets offer extended terms as a means of attracting new customers.

- Highly profitable companies offer longer terms because of their greater financial resources – the opposite is true for companies with low profitability.

- Small accounts receive shorter terms as they are costly to manage and account for a small percentage of total sales.

- Larger accounts receive longer terms because of their importance and greater market power.

- Higher credit risk customers receive shorter terms to control bad debts.

- Lending covenants such as a minimum current ratio reduce the length of terms by restricting the amount of accounts receivable companies can hold.

Credit Approvals

Companies should conduct a thorough credit assessment of all potential customers before extending trade credit and then monitor their status on an on-going basis. This assessment is used to decide whether to lend and the size of the credit limit. Credit limits will likely be small for new customers, but will rise as they demonstrate a successful payment history. Large customers and governments may not be given credit limits at all. Credit limits help control credit risk while avoiding the cost of approving each purchase as it occurs.

Customers normally have to complete a credit application and provide credit references from former suppliers, lenders, or lessors. Larger accounts may also need to supply unaudited or audited financial statements. Many companies make use of a credit reporting agency to aid in their decision making. Dun & Bradstreet (D&B) is the world’s largest commercial credit reporting agency providing online, real-time credit reports for over 90 million companies globally including 1.5 million in Canada. These reports provide both historical and predicative information that varies in detail and cost depending on a company’s needs. Some of the information D&B provides includes:

- PAYDEX Score

- Measures what percentage of a customer’s dollar-weighted trade credit was paid on time over the last year. Scores of 80.0% or higher are considered acceptable by lenders.

- Failure Score

- Measures the probability that a customer will cease operations over the next 12 months without paying all of its creditors in full or will obtain relief from its creditors as part of a bankruptcy.

- Delinquency Score

- Measures the probability that a customer will be severely delinquent in their payments over the next 12 months. Severely delinquent is when 20% or more of its payments are 90 days or more past due.

- Maximum Credit Recommendation

- Recommends the maximum amount a company should lend to a customer based on the size of the organization and other risk factors.

- D&B Rating

- Determines the financial strength of a customer by calculating its tangible net worth which is equal to the value of its equity minus any intangible assets. The net tangible assets are source of potential funding if a customer experiences payment difficulty. Other risk measures are also considered when calculating this rating.

- Country/Region Insight

- Assesses the risk level of a country or region as low, moderate or high based on the opinion of a panel of experts as a basis for extending trade credit to companies in that area. Detailed country or region reports are also available.

- Financial information and ratios

- Provides summary financial statement information such as total assets and total liabilities along with key operating ratios such as the current ratio.

- Legal proceedings

- Summarizes the number of insolvencies, judgements, liens, and suits the customer is involved in and the total dollar value of all judgments and suits.

All credit information is supplied on a voluntary basis by suppliers so some credit assessments may be unreliable due to a small sample size. Besides commercial credit reporting agencies, banks can also provide credit information based on their dealings with these potential customers.

Consumer credit reporting agencies in Canada such as Equifax and TransUnion also provide credits reports based on creditor information and other sources such as court records and collection agencies. Based on these reports, credit agencies calculate a credit score. There are many different models and weighting systems for calculating these scores, but a typical breakdown provided by Equifax recommends:

- Payment history (35%)

- Frequency, length and size of delayed or missed payments on different loans such as credit cards, personal lines of credit, automobile loans, student loans, home equity loans, or mortgages are evaluated. Customers with the most on-time payments receive the highest credit scores.

- Credit utilization (30%)

- Customers with a low ratio of debt to total credit available are scored favorable. Those who have borrowed the maximum against a number of credit accounts and have opened new accounts recently will be classified as high-risk borrowers and have their credit scores reduced. Also suspect are customers with a limited variety of credit accounts such as numerous credit cards.

- Credit history (15%)

- Customers with credit accounts that have been in existence for a long time demonstrate that they can manage credit effectively and will receive a higher credit score.

- Public records (10%)

- Those with a history of bankruptcies, foreclosures, judgements, liens, or dealings with collection agencies will have their credit scores reduced.

- Inquiries (10%)

- Numerous credit file inquiries by lenders relating to new loan requests may indicate a customer is experiencing financial distress which will negatively affect their credit score.

In addition to a credit score, creditors consider other factors such as a customer’s income, years of employment, and home ownership when deciding whether to lend.

Some firms rate potential customers themselves using statistical credit scoring models that they have purchased or developed internally, or by implementing a more qualitative credit rating system based on the 5 Cs of credit assessment. These include:

- Character

- Is the perceived honesty of a customer that is usually measured by their past payment history.

- Capacity

- Are the current and future cash flows available to a customer from employment or operating a business that can be used to satisfy their obligations.

- Capital

- Comprises other resources such as investments that can be liquidated if a customer’s cash flows are insufficient to pay its debts.

- Collateral

- Includes the assets and any personal or third party guarantees pledged by a customer that can be used to satisfy their obligations if there are payment difficulties.

- Conditions

- Incorporates macroeconomic factors such as interest rates, exchange rates, or the business cycle that affect the strength of the economy and a customer’s ability to pay their obligations.

Collections

Once the decision to extend credit is made, terms ought to be strictly enforced. All payments should be received by the due date and penalties and interest charged on any overdue balances. Penalties and interest can be difficult to collect as many customers just refuse to pay, but at least having them lets the customer know how serious the company is about collections.

Despite advances in EFT, some customers will still want to pay using a paper cheque. This allows them a few extra days of credit while their cheque moves through the postal and cheque clearing systems. Cash discounts are sometimes used to encourage electronic payment, but companies can just require that payments be made electronically as a condition of receiving credit.

In order to get paid quickly, it is important that companies get accurate invoices out to their customers as quickly as possible. Mistakes and adjustments delay receipts as customers typically withhold payment on the full invoice until the errors are corrected. Electronic systems for invoicing and payment help to reduce turnaround times. Reminders may also be sent out to customers, especially new customers, before payment is due to welcome them, ensure they have received their invoice, and remind them of the need to pay on time.

A formal collection procedure with timelines should be established to deal with overdue accounts. Typically, companies will:

- Issue duplicate customer invoices or statements.

- Provide a verbal warning(s) followed by a written warning(s) if unsuccessful.

- Reduce credit limits, shorten credit terms, place customers on COD or CBD, or cut them off entirely until payment is received.

- Negotiate special repayment plans, secure post-dated cheques, or have them sign a formal promissory note that can be more easily enforced in the courts.

- Take court action, use a collection agency, or write-off accounts if further collection costs are not justified given the likelihood of payment.

It is important to apply the cost-benefit principle in collections. Focus a department’s efforts on larger accounts that are experiencing difficulties. Before taking legal action, ensure that the amount that can be collected is greater than the expected legal costs. Remember a creditor might also be able to pursue the personal assets of a consumer or owners of an unincorporated business. A company may be successful in court but if customers have no assets to pay the judgement then it is of no value. Small claims court can be used to collect minor amounts as a lawyer is not needed.

Companies should be firm in their collection practices but not overly aggressive as customers may take their business elsewhere. There will always be customers that abuse the credit system, but most are just experiencing temporary financial difficulties. Having a well-trained collection staff who can recognize these two groups pays off. They also know how to convince customers to pay promptly by stressing what is important to them such as protecting their valuable credit ratings, restoring their reputations, and being respectful of the long-term relationship they have established with the supplier. Collections staffers should have scripted responses to all possible excuses and know what legal actions the company will take next if payment is not received so they can communicate it to the customer.

A company’s sales and collections departments must closely coordinate their efforts to be effective. Salesforces are focused on meeting quotas, but they also have close working relationships with their clients. They will know if a struggling client has the potential to develop into a valued customer in the future. In these cases, a company might decide to be more lenient with collections until they have had a chance to recover. The collections department must be made aware of these decisions so they do not confuse and alienate customers with their aggressive collection efforts. Sometimes a personal call from a sales representative instead of an unknown collections’ staffer is all that is needed to secure payment.

Collections management can be a highly computerize process. Technology is expensive but it pays for itself through reduced labour costs, quicker credit approvals, faster communications and payments, and timely monitoring of past-due accounts. Some companies, particularly smaller seasonal firms, choose to contract out their credit management function to a factoring company. Factors supply financing by buying a company’s accounts receivables prior to the due date, but they also provide credit approval, monitoring, and collections as a standalone service.

Larger companies may establish separate sales finance subsidiaries to manage their consumer and trade credit. This creates administrative efficiencies and allows the company to secure financing at a lower cost by consolidating all their collateral into one business unit. Credit insurance can be purchased to protect the company from bad debts. The Export Development Corporation provides insurance for export receivables while private insurance companies cover other types of receivables.

Credit Monitoring

Thorough credit approvals and careful monitoring of active accounts is critical in controlling collection costs. Careful monitoring allows companies to identify problems early and take the appropriate actions to limit losses. Instead of reacting to credit problems, companies can act pre-emptively and build long-term relationships with their customers by helping them through difficult financial times.

- Days of sales outstanding (DSO)

- This ratio measures the number of days it takes a company to collect its credit sales. It is calculated:

- [latex]{\text{DSO}} = (\frac{{\frac{{365}}{{{\text{Sales}}}}}}{{{\text{Average Accounts Receivable}}}})[/latex]

- Instead of expressing this ratio in days, practitioners often use the receivables turnover ratio which is the denominator only (sales / average accounts receivable).

- The DSO should match the credit terms the company offers. For example, when terms are net 30, the DSO will be approximately 30 days as customers will not pay until the end of the payment period. If customers take longer, they are likely “stretching” their payables due to financial difficulties, taking advantage of the company’s lenient collection practices, or using their market power to exploit a smaller supplier. If a company also offers an early payment discount such as 2/10, net 30, the DSO should be approximately 10 days as customers will pay early to take advantage of this lucrative discount.

- Aging schedule

- This schedule indicates the percentage of a company’s accounts that are current (i.e. still within the credit terms) and those that are past due and by how long. Percentages vary with the seasons and can be compared against previous years or industry averages if available.

Exhibit 5: Aging Schedule

CAD April May June Sales 583,000 495,000 616,000 Accounts receivable 660,000 616,000 715,000 Current (under 30 days) 345,180 52.3% 297,528 48.3% 365,365 51.1% 0-30 days overdue 110,880 16.8% 112,728 18.3% 125,125 17.5% 31-60 days overdue 97,680 14.8% 93,016 15.1% 106,535 14.9% 61-90 days overdue 67,980 10.3% 72,688 11.8% 72,930 10.2% 91+ days overdue 38,280 5.8% 40,040 6.5% 45,045 6.3%

DSO ratios and aging schedules only provide an overall assessment of a company’s collections. Computerized credit management systems also provide numerous real-time credit reports showing status by customer, industry, country, division, product line, type of credit terms, or size of customer. Information about specific customers is obviously needed to begin collections, but these other reports are very useful. For example, if an industry is experiencing problems due to deteriorating economic conditions, a company may decide to lengthen its credit terms to provide additional financial assistance or strengthen the credit approval process to exclude problem customers. If smaller customers are a problem, this group may be put on CBD or COD or the company may stop servicing them entirely. Finally, if longer credit terms are a problem, reduce them and force customers to supplement their trade credit with other sources of temporary financing.

Besides internally generated reports, remaining current with industry news helps companies identify collection issues before companies begin experiencing difficulties.

4.3 | Managing Inventory

Inventory management incorporates the different technologies and techniques companies employ to order, transport, track and store the inputs used to manufacture products before delivering them to customers. Inventories include raw materials, parts, work-in-progress, finished goods, scrap, and supplies. The goal of inventory management is to meet a company’s specific production and sales targets while carrying the level of inventory that maximizes its profits. Too much stock leads to excessive carrying costs such as ordering, financing, storage, handling, insurance, and taxes and increased product damage, spoilage and obsolescence. It can also lead to cash flow problems during an economic downturn when excess inventory is much more difficult to sell. Too little stock causes production delays when key inputs are not available; rising manufacturing costs due to reduced economies of scale; lower customer satisfaction and lost sales due to stock-outs; fewer quantity discounts by not purchasing in bulk; an inability to guard against price increases, work stoppages or other supply interruptions by stockpiling inventory; or being unable to balance stable production with variable customer demand. Effective inventory management is an important competitive advantage that improves customer service and raises profits.

Inventory Management Techniques

Companies use a variety of technologies and techniques that directly or indirectly help better manage their inventories. Some of the most important include:

- Supply chain technology

- Advances in technology since the microcomputer revolution began in the early 1980s have transformed how companies manage their inventories. Periodic inventory systems have been replaced by perpetual systems that provide real time information on stock availability using barcodes, point-of-sale terminals, satellite and wireless communication systems, and hand-held inventory management devices. Traditional warehouses have been replaced by storage and retrieval systems with automated stock picking using robotics, computer-guided vehicles and conveyer systems. Inventory is delivered using driverless vehicles and drones and tracked using global positioning (GPS) systems that give suppliers and customers real-time delivery information. Advanced forecasting and optimization software and expert systems have improved the quality of production planning. Inside factories advances such as robotics, numerically controlled machines, and three-dimensional printing have made production more flexible and efficient reducing work-in-progress and finished goods inventories.

- ABC analysis

- The Pareto principle or the 80%/20% rule states that roughly 80% of the effects come from 20% of the causes. This principle has many applications in business such as the commonly quoted finding that 80% of a company’s sales comes from 20% of its customers. In inventory management, many companies also find that 80% of their costs of production come from 20% of their inputs. Since this small number of high value items contributes so much to total costs, ABC analysis says to devote considerably more resources to controlling this class of inventory and to keep their stock levels low to reduce costs. For other lower valued inventory classes, larger safety stocks can be carried to reduce the risk of stock-outs with little added expense. Fragile items or ones that are more likely to be stolen can also be added to the high-value class so they are better controlled. The name ABC analysis is used because companies divide their inventory into three or more classes.

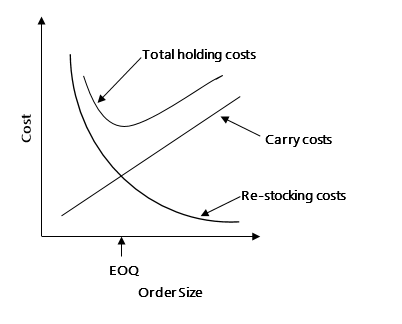

- Economic order quantity (EOQ)

- Significant carrying costs are incurred financing, storing, handling, insuring and paying taxes on large inventories. Damage, spoilage and obsolescence charges also rise as inventories grow. To lower these costs, companies may decide to carry less stock which means re-stocking it more often by placing smaller orders causing ordering, transportation and handling expenses to rise. EOQ is the order size that minimizes total holding costs which is the sum of carrying and re-stocking costs.

Exhibit 6: Carrying and Re-stocking Costs

-

- If we assume stable demand, total inventory holding costs can be calculated using the formula:

- Total holding costs = Carrying costs + Re-stocking costs

- If we assume stable demand, total inventory holding costs can be calculated using the formula:

-

-

- H = (C x ()) + (R x ())

- D = Yearly demand

- Q = Order quantity

- C = Carryings costs per unit

- R = Re-stocking costs per order

- H = Total holding costs

-

- As seen in Exhibit 5, total holding costs are minimized when carrying costs equal re-stocking costs. If the two components are equated to each other, the formula simplified, and Q isolated, Q is the EOQ.

- [latex]\begin{array}{rCl}({\text{C x }}(\frac{{\text{Q}}}{2}))&=&({\text{R x }}(\frac{{\text{D}}}{{\text{Q}}}))\\{\text{EOQ}}&=&\sqrt {\frac{{2{\text{DR}}}}{{\text{C}}}} \end{array}[/latex]

- EOQ can also be determined by taking the total holding cost equation and setting the derivative of the equation equal to zero. The derivative calculates the slope of an equation. The slope is zero at the minimum point of the total holding cost equation, which is the same as the crossover point of the carrying and re-stocking costs.

- [latex]\begin{array}{rCl}\frac{{d{\text{H}}}}{{d{\text{Q}}}}&=&\frac{{\text{C}}}{2} - \frac{{{\text{DR}}}}{{{{\text{Q}}^2}}}\\0&=&\frac{{\text{C}}}{2} - \frac{{{\text{DR}}}}{{{{\text{Q}}^2}}}\\{{\text{Q}}^2}&=&\frac{{2{\text{DR}}}}{{\text{C}}}\\{\text{EOQ}}&=&\sqrt {\frac{{2{\text{DR}}}}{{\text{C}}}} \end{array}[/latex]

- One limitation of the EOQ formula is that C and R are assumed to be variable costs, but they actually consist of both variable and fixed cost components. Economies of scale will reduce these costs as volume increases but for simplicity this is ignored.

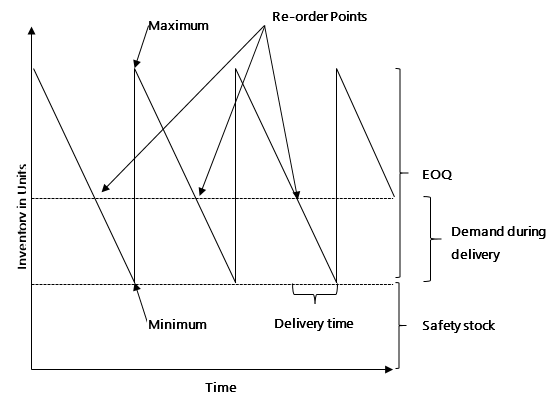

- EOQ is the optimal order size, but a company must also determine when to place the order. For example, if it takes 10 days on average for an order to be processed and delivered by the supplier and demand is normally 20 units daily, then the re-order point is 200 units. As the company waits for the order to arrive, they should have sufficient inventory to satisfy demand. The re-order point is also called the minimum and the maximum is equal to the re-order point plus the EOQ.

- The order time of 10 days and demand of 20 units per day are estimates. If order time is longer or demand is higher than expected, the company will experience a stockout causing customer ill will and potentially a lost sale if the customer decides to buy elsewhere instead of waiting. To guard against this, a company may carry additional inventory or a safety stock. Assuming order times can be accurately estimated, the optimal safety stock depends on the probability of demand being greater than expected, stockout costs, and the cost of carrying the additional safety stock. Greater demand uncertainty and higher stockout costs favors carrying a larger safety stock while higher carrying costs discourages it. Re-order points, EOQs, and safety stocks can be difficult to calculate in practice due to changing input values, but the approach has gained wide acceptance in industry.

Exhibit 7: EOQ Summary

- Materials resource planning (MRP)

- MRP is a computerized inventory management system. It starts with a company’s production schedule that is based on its sales forecasts. The MRP system then automatically determines the derived demand for raw materials, parts, sub-assemblies, and supplies that are needed to complete production after adjusting for current inventories. It determines when these materials are needed in production and the date inputs must be ordered so they arrive on time. Once production begins, the system adjusts in response to problems such as missed delivery dates or stock-outs.

- MRP II expands on MRP systems by managing more aspects of a manufacturer’s operations such as purchasing, materials management, shop floor planning and control, order fulfillment, capacity planning, and accounting. Enterprise resource planning (ERP) systems go even further managing all functions of an organization not just those related to manufacturing such as human resources, finance or marketing. MRP, MRP II, and ERP systems are highly complex systems that are both time consuming and expensive to operate. Using information technology effectively to provide timely, accurate data is critical to their success.

- Just-in-time (JIT)

- JIT inventory management is closely linked with MRP systems. Inputs arrive at the factory when they are needed in production and not simply stockpiled for future use. This system has large up-front costs and is difficult to manage but it can result in considerable long-term savings. Orders are smaller and arrive more frequently, usually daily, meaning companies only have a few hours of inventory on hand at any time. Deliveries must be on-time and contain the correct type and number of items or production quickly comes to a halt. Suppliers may need to establish new manufacturing facilities closer to their customers to meet faster delivery requirements and implement stricter quality-control procedures such as statistical process control (SPC) or total quality control (TQC) so defects do not slow production. JIT generally results in a greatly reduced number of suppliers and a much closer customer-supplier relationships where the two parties share production forecasts; establish integrated EDI systems to communicate with each other; work jointly on product development; and cooperate to reduce costs and improve quality using value analysis.

- Value analysis or value engineering determines best practices in product design, materials, purchasing, manufacturing, and other business processes that eliminate unnecessary costs without reducing a product’s required quality, effectiveness, and overall customer satisfaction. This technique not only minimizes costs it raises employee morale, encourages greater team work, and promotes a culture of continuous improvement.

- JIT principles can also be applied to manufacturing. Instead of producing in large batch sizes to minimize costs, flexible manufacturing allows companies to reduce the fixed costs associated with changing over their production line so they can quickly and cheaply convert their facilities to manufacture a variety of products. This results in smaller batch sizes that lowers inventories. Supply chain management professionals refer to this as a “pull” system as goods are manufactured in reaction to actual customer orders and are not “pushed” through the system after being produced in bulk.

- JIT inventory and manufacturing systems have the potential to greatly reduce a company’s operating costs, but they also expose it to considerable risk. By not having an inventory buffer, business interruptions such as natural disasters, political strife, weather delays, strikes and lockouts, quality control problems, or bankruptcies quickly lead to supply problems. Companies cannot avoid expected price increases, take advantage of quantity discounts, or benefit from economies of scale if they are unable to buy or produce in bulk. They will not be able to fill large unexpected orders quickly since products must be manufactured first. JIT systems are highly integrated and difficult to balance consistently without alienating customers. Suppliers who can meet the demanding supply schedules are difficult to find. A large investment in information technology systems is also required.

- Vendor-managed inventory (VMI)

- To justify the major commitment a supplier makes to a JIT inventory system, many are awarded single sourcing contracts and become the exclusive vendor for a group of products. These relationships are ongoing and regularly renewed as long as delivery dates and quality standards are met. The supplier’s degree of involvement varies, but in a VMI system they are given real-time access to inventory data, production schedules, and sales forecasts and are expected to deliver stock as required. Ongoing communications between the supplier and customer helps prevent stockouts caused by unexpected changes in demand and sales promotions. Deliveries may be based on established minimum/ maximum levels or left entirely up to the supplier providing a major incentive for them to manage inventories effectively. To meet their obligations, some suppliers place staff in the customer’s warehouse while others rent a separate production or storage facility near the customer and supply stock on a JIT basis from there. Others use drop shipping where a product is sent directly from the manufacturer to the final consumer to reduce shipping and handling costs.

- Payment can occur upon delivery subject to regular credit terms, but increasingly other methods are being used. Suppliers of high-value components can be paid-on-production to give them a needed cash infusion. Others might retain ownership as part of a consignment agreement and are only paid when/if the product is sold. Consignment encourages suppliers to manage inventories efficiently since they are responsible for most of the carrying costs. It also helps to address the “bull-whip” effect which finds inventories become more excessive as companies move upstream in the supply chain away from the final consumer.

- Concurrent engineering

- Successful manufacturers are careful to use integrated teams of marketing, design, engineering, and manufacturing specialists to develop new products. With all the disciplines working together concurrently applying value analysis principles, these teams consistently generate items with better styling and higher quality that can be manufactured at a lower cost. Concurrent engineering employs a number of related practices. Parts simplification is where engineers try to minimize the number of parts in a new product. Design for manufacturing means making products that are easier to assemble on the production line. Design for disassembly includes designing products that are simpler to take apart for maintenance or recycling at the end of their lives. Modularization involves introducing new parts only when they are essential to meeting customer needs and uses standardized parts for everything else. Platform building uses a shared platform for a family of products such as a truck chassis, body and engine that can be customized to suite customer needs by adding a variety of features. All these practices help to decrease the quantity and value of parts, work-in-progress, and finished goods inventories.

- Outsourcing

- This is an agreement with a third-party contractor to provide business services that are traditionally performed in-house. Some activities typically outsourced include accounting services, claims processing, manufacturing, information technology, and call centres. Outsourcing can take different forms. Offshoring moves work to another country where wages are typically lower. Nearshoring is the same as offshoring except operations are located in a nearby country to realize greater synergies. Farmshoring shifts work to rural areas where wages are lower and workers are less likely to unionize. Homeshoring moves work into home offices using independent contactors reducing wages and corporate overhead. Insourcing brings work back inhouse while reshoring returns it to the home country after being offshore to re-assert greater control over key businesses processes. Co-sourcing supplements a company’s internal capacity by adding outside contractors.

- Outsourcing is normally undertaken as a cost-cutting measure to reduce wages, but it offers a number of other potential advantages:

-

- Focus in-house on core business activities that are critical to a business’ success and outsource all remaining non-essential activities.

- Maximize the sustainable growth rate by utilizing internally generated capital to finance core activities only.

- Access technical expertise that is not available internally and would be difficult to develop given current skill shortages.

- Convert a fixed cost into a variable cost reducing a firm’s operating leverage and increasing its financial flexibility.

- Increase the speed to market for a new business or product.

- Realize economies of scale by having contractors provide the same services for a number of companies.

- Have contractors comply with complex regulatory requirements.

- Streamline the production process or accelerate a corporate reorganization.

- Use co-sourcing to temporary supplement existing staff in specialized areas.

- Outsourcing normally generates considerable cost savings, but third-party contractors may gain access to critical technology and sensitive operational information that could weaken a firm’s competitive position. The firm may also lose control over key areas such as product quality and customer service and be unable to enforce policies and procedures relating to issues such as child labour or work place health and safety. Language problems, time zone differences, and animosity between the company’s staff and its contractors can lead to communication problems that hurt performance.

- Lean manufacturing

- World class manufacturers are always trying to be more efficient. Lean manufacturing, developed by Toyota Motor in Japan, identifies eight types of waste (or Muda in Japanese) and focuses on ways to eliminate them.

-

- Overproduction

- Manufacturers realize economies of scale by producing in large batch sizes, but this can lead to high carrying costs including product spoilage or obsolescence charges if demand falls or consumer tastes change. Flexible manufacturing and JIT production help reduce overproduction waste.

-

- Over-processing

- Providing product features that are not important to the end consumer is expensive and the cost is never recovered through a higher selling price. Manufacturers should carefully determine what customers value and focus on providing it. Concurrent engineering and value analysis limit over-processing waste.

-

- Defects

- Defective products are costly in terms of scrap, re-work charges, production delays, customer ill will, and lost sales. Lean manufacturers re-engineer their business processes to make them mistake proof (or Poke-yoke) and install systems that automatically detect quality problems (or Jidoka). Concurrent engineering, parts simplification, design for manufacturing, SPC, and TQC ensure quality is built into a product and carefully monitored. A lean manufacturer’s goal is to have “zero defects” and they will halt production at any time to address quality issues. Releasing defective products to consumers is not an option.

-

- Unnecessary transportation

- Transporting work-in-progress from one location to the other adds costs but provides no value to the final consumer. Building products in just one facility and encouraging suppliers to locate close by as part of a single sourcing agreement mitigates transportation waste.

-

- Waiting

- Idle employees and machinery are costly and indicate that the next workstation is not ready to complete its task. Idle customers are also dissatisfied which usually leads to lost sales. Lean manufacturers reduce waiting time by re-engineering their production systems to create constant flow so products move from one workstation to the next on a JIT basis with minimal work-in-progress. Distances between workstations are reduced and employees are not asked to ramp up production temporarily to meet spikes in demand as this will lead to worker stress, production inefficiencies, and higher defects. Work-in-progress and finished goods inventory is used to balance stable production with unstable demand.

-

- Needless movement

- Lean manufacturing has 5s of workplace organization to help control waste due to the needless movement of people, inventory, and machinery. According to the 5s, employees should sort (or Seiri) through their materials so only those tools needed to complete their tasks remain. These tools are set in order (or Seiton) so tasks can be easily completed with no unnecessary movement. The workplace must shine (or Seiso) meaning it is clean and orderly. Workplace practices are standardized (or Seiketsu) so they are consistently followed and sustained (or Shitsuke) over time through regular audits.

-

- Waste of talent

- Valuable human resources are often squandered due a lack of training, ineffective employee communication, bureaucratic work methods, a lack of motivation, and ineffective teamwork. Full utilization of an employee’s skill set helps creates a more efficient workplace.

-

- Excess inventory

- Unneeded inventory is a by-product of the other forms of waste. ABC, EOQ, MRP, MRP II, ERP, JIT, VMI, and outsourcing all help to reduce waste relating to excess inventory.

- Paramount to the success of lean manufacturing is the principle of continuous improvement or Kaizen meaning “good change.” Instead of making a few major breakthroughs, companies should continuously strive for perfection through small incremental improvements overtime. Ideas come primary from customers and employees working in autonomous work teams and not from management, outside consultants, or equipment vendors. Workers are engaged and respected for their knowledge and take responsibility for the production process. The changes they recommend are usually quicker to implement and require fewer capital expenditures compared to those of management. Open communications between customers, employees and management is the norm.

- Lean Six Sigma is a popular industry program that combines the principles of lean manufacturing with the statistical quality control method Six Sigma developed by U.S.-based Motorola. Lean manufacturing focuses on streamlining business processes by reducing waste while Six Sigma’s goal is to eliminate deflects. Both techniques are heavily dependent on data collection and analysis. The American Society for Quality (ASQ) and other professional organizations offer certification programs in Lean Six Sigma. Graduates are awarded white, yellow, green and black belts like in the martial arts depending on their level of achievement.

Key Performance Indicators

A number of key performance indicators (KPIs) are useful in evaluating how efficiently a company manages its inventory.

Days of inventory on hand (DOH)

This ratio measures the number of days it takes a company to sell its inventory and earn a profit. It is calculated:

[latex]{\text{DOH}} = (\frac{{\frac{{365}}{{{\text{Cost of sales}}}}}}{{{\text{Average Inventory}}}})[/latex]