Module 6: Capital Budgeting

A factory manager believes some of their plant’s equipment is outdated so they schedule an appointment with a major supplier. The salesperson confirms the equipment should be replaced and proceeds to describe what their company has to offer. Does the factory manager make the purchase immediately? Of course not—in addition to getting a number of competing bids, the manager must carefully compute whether the expected future benefits from the new equipment exceed its initial and ongoing costs on a present value basis. If they do not, then the company is failing to earn its required rate or return (RRR) and the project should not proceed.

Capital budgeting is a critical activity at any business. It helps senior management establish a long-term strategic direction for the company by evaluating different growth opportunities such as introducing new products, expanding into new markets or acquiring competing firms. At the lower levels of the firm, it is invaluable in assessing product improvements ideas, cost-saving plans, or proposed capacity additions. Maintaining a constant flow of new investments is essential to a company’s long-term profitability and survival.

Although accountants typically take the lead in calculating a project’s net present value (NPV), specialists from the other business areas play a critical role in estimating a project’s future benefits and costs; determining an RRR that accurately reflects a project’s risk level; and ensuring a company’s strategic goals are met. This team approach results in a very thorough project evaluation that helps companies cope with the risk of high initial costs and uncertain future benefits.

6.1 Capital Budgeting Process

The capital budgeting process allocates a company’s investment funds to major projects. The process becomes more elaborate as organizations become larger and the value and complexity of projects increase. Many large companies have formal capital expenditure planning committees with detailed operating procedures that approve all major capital expenditures. These committees generally consist of a team of experts from across the company and its different disciplines including accounting, finance, marketing, operations, and human resources. They critically review all projects from their varying perspectives to ensure that they are financially and operationally sound and consistent with the company’s strategic plans. As the size of capital expenditures decrease and become more routine, investment decision making is pushed down into a company’s divisions and departments and the processes used to assess projects become simpler. Most organizations establish cost limits that determine which level of management has authority to approve a project.

The five steps in the capital budgeting process include:

- Step 1–Project idea generation. Ideas can be found internally or by scanning the external business environment, benchmarking the company against its competitors, or acquiring innovative companies or product ideas. Smaller investment proposals may originate at the department level among junior managers and line workers formed into autonomous work teams. As projects grow in value, divisional and corporate management becomes more involved. Pay and human resource systems at all levels should be designed to encourage employees to contribute.

- Step 2–Screening of proposals. Before committing to an expensive evaluation of a project, the capital expenditure planning committee or senior management will review the project to ensure it has a reasonable chance of success and is consistent with the company’s strategic plans.

- Step 3–Project evaluation. A project’s profitability is determined using different evaluation methods including payback period, discounted payback period, accounting rate of return (ARR), net present value (NPV), internal rate of return (IRR), or profitability indexes (PI). In addition to a thorough quantitative analysis, business units must also prepare a written description and justification which describes how the project supports the organization’s strategic goals. All forecasts should be consistent with a common economic outlook provided by the company.

- Step 4–Preparation of the capital budget. All unprofitable or strategically undesirable projects are eliminated and the remaining projects are ranked based on their profitability along with any resource constraints such as limited funding or a lack of manpower availability. Some projects are mandatory and must be done in order to comply with health and safety or environmental regulations in which case the goal to complete the project efficiently. Others may lose money but are accepted anyway for strategic reasons to give the company exposure to a new industry or to development new competencies in hopes of earning positive returns in the future. Pet projects championed by influential managers that usually do not go through the normal approval process or are approved based on overly optimistic projections should be avoided.

- Step 5–Monitoring and post-completion audits. During implementation, a project must be monitored on an ongoing basis to ensure that construction targets are met, there are no cost overruns, and key inputs such as the price of the product do not need to be adjusted. If problems arise, the company has to decide whether to stay the course, alter its plans, or abandon the project. Post-completion audits also occur at the end of a project to help improve a company’s capital budgeting system. Benefits include:

- Ascertains why variation between planned and actual performance occurred so any lessons learned can be applied to current and future projects.

- Strengthens a manager’s estimating abilities by holding them accountable for their forecasts and project selections.

- Detects biases by managers who consistently over estimate benefits or underestimate costs.

- Discourages pet projects by influential managers.

- Provides an excellent training opportunity for new managers and can be part of their performance review.

- Provides an excellent source of new project ideas.

- Monitoring and post-completion audits should be conducted by individuals who are not involved in the project selection process to ensure their objectivity and help eliminate the psychological and internal political barriers to cancelling a project. Once a manager or business unit receives approval for a project, they are very hesitant to admit that they might have made a mistake and relinquish resources. Losses will continue longer than necessary especially if these managers are able to use their connections within the organization to gather support.

Project Evaluation Methods

There are six different methods companies commonly use to evaluate capital projects. Most are based on cash flow estimates instead of accounting estimates which are heavily influenced by the accounting policies adopted.

- Payback period. This is the time it takes to recover a project’s initial investment from its future cash flows. Companies may decide to only accept projects with a payback period below some specified cut-off point such as five years or use it to supplement other evaluation methods like NPV or IRR. The advantages of this approach are that it is 1) simply to use, 2) easy to understand and 3) conservative meaning it focuses on risk by measuring how quickly a company gets back its initial investment. Its disadvantages are 1) it does not use present value leading to faulty decisions, 2) the riskiness of the project is not reflected in the discount rate, 3) the cut-off point is arbitrarily selected, 4) it only measures a project’s breakeven point resulting in a bias against long-term projects with extended payback periods but higher overall profitability, and 5) it focuses too much on breaking even and not earning a profit which it the reason for going into business.

Exhibit 1: Failure to Consider the Time Value of Money

Period Project 1 Project 2 0 CAD (40,000) CAD (40,000) 1 20,000 10,000 2 10,000 10,000 3 10,000 20,000 4 50,000 50,000 Payback 3 Years 3 Years NPV CAD 31,782 CAD 30,461 Projects have the same payback period but Project 1 is more profitable due to the time value of money so it is the preferred project. Total cash flows of the two projects are the same, but Project 1 is more profitable because its cash inflows are received quicker. Exhibit 2: Bias Against Long-term Projects

Period Project 1 Project 2 0 CAD (30,000) CAD (30,000) 1 20,000 10,000 2 10,000 10,000 3 – 10,000 4 – 20,000 Payback 2 Years 3 Years NPV CAD 2,908 CAD 10,472 Project 1 has a shorter payback period but loses money on a present value basis. Project 2 has a longer payback period but earns a much higher profit so it is the preferred project. - Discounted payback period. This is the time it takes to recover a project’s initial investment from its discounted future cash flows. The advantages and disadvantage of this method are similar to the payback period method except present value is used and the discount rate can be adjusted to reflect varying levels of risk. If a project pays back its investment on a discounted basis it will make a profit, but it still may be rejected if the arbitrary cut-off point is not reached.

- Accounting rate of return (ARR). It is a project’s average net income divided by the average assets used to earn that income over its life. This is the only method that uses accounting estimates instead of cash flow estimates to determine a project’s rate of return. Even though this approach does not use cash flows or present value, it is popular among manager’s because it shows how a proposed project will affect a company’s rate of return assets over the life of the project.

- Net present value (NPV). This is the present value of a project’s future cash flows minus the initial investment or its profitability in dollar terms. The discount rate used to determine the present value of future cash flows is the RRR that investors require to be fairly compensated for a project’s risk. A project with a positive NPV is generating a higher return than the RRR or what economists call excess profits. In competitive markets, there should be few excess profits due to the entry of new competitors. The advantages of this method are the NPV is in dollars so it can be added directly to the company’s market value to determine the effect on share price. Also, the RRR can be adjusted to reflect the varying risk levels of different projects or specific cash flows within project. In order to maximize a company’s share price, all positive NPV projects should be accepted. Excel provides a function to calculate a project’s NPV.

- Internal rate of return (IRR). This a project’s rate of return that equates its initial investment with its future cash flows. If the IRR was used as the RRR, a project’s NPV would be zero. The difference between the IRR and RRR is the project’s excess profits expressed as a percentage. Some company’s prefer IRR because it is easier to communicate than NPV which is in dollars. IRR can also be used if a company cannot accurately estimate its RRR. Its disadvantages are IRR cannot be adjusted for the risk of specific projects or cash flows like the RRR. Also, IRR has a number of mathematical problems that may result in the wrong project being selected. Excel provides a function to calculate a project’s IRR.

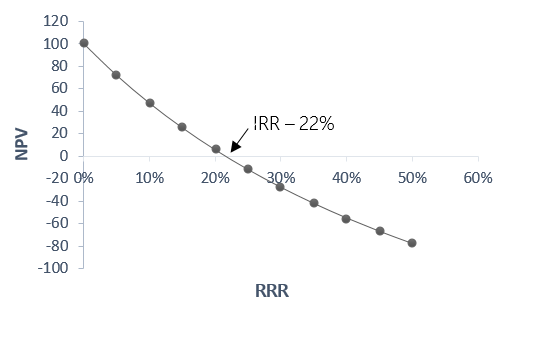

- The NPV and IRR approaches are very similar. To relate these two methods, analysts sometimes create an NPV profile that graphical shows a project’s NPV at different RRRs and its IRR. Exhibit 3 shows a project with an initial investment of CAD 300 that generates yearly cash flows of CAD 200 over two years.

- Exhibit 3: NPV Profile

- Profitability index (PI). This is the ratio of the present value of a project’s future cash flows to the initial investment. A project has a positive NPV if its profitability index is higher than one.

NPV is the preferred method for evaluating capital projects especially for large companies who better understand the limitations of the other approaches. Payback and IRR are used to supplement NPV, but are typically not the primary methods partially because of the mathematical problems with the IRR. The remainder of this module will focus on the NPV method after carefully considering these problems.

Mathematical Problems with IRR

The IRR method’s mathematical problems relate to the re-investment rate used for the cash flows generated by the project, the potential for multiple IRRs, and faulty decisions when choosing between mutually exclusive projects.

- Re-investment rate. IRR is the rate of return that equates a project’s initial investment with its future cash flows. This method assumes that when cash flows are received over a project’s life that they are re-invested at the IRR. In practice, this assumption may not be accurate as funds will likely be re-invested in other capital budgeting projects or investments with varying rates of return. If the rate of return on the project and the re-investment rate are expected to be materially different, then a modified IRR (MIRR) should be calculated. Using this method, the future values (i.e. not present value) of all recurring cash flows are calculated at the end of the project’s life using the re-investment rate. The interest rate that equates the total of these future values with the initial investment is the project’s modified IRR. The re-investment rate is usually assumed to be the RRR as this is what a firm will earn on average on all its projects if markets are competitive. Excel provides a function to calculate a project’s MIRR.

- Multiple IRRs. As the RRR rises, a project’s NPV should logically fall. As the example in Exhibit 4 shows, this is not true if the cash flows are non-conventional and switch signs over a project’s life. The sign may change if a company expects to lose money at different points possibly during a major product retrofit or if it must incur significant costs to restore a mine or factory site at completion.

Exhibit 4: Understanding Multiple IRRs

RRR Cash Flows (CAD) Difference (CAD) NPV (CAD) Year 0 Year 1 Year 2 0.0 -58.00 +149.00 % Change -94.00 % Change +55.00 -3.00 11.4 -58.00 +133.75 -10.23% -75.75 +19.41% +58.00 +0.00 26.2 -58.00 +118.07 -11.72% -59.02 +22.09% +59.05 +1.05 45.5 -58.00 +102.41 -13.26% -44.04 +24.77% +58.00 +0.00 50.0 -58.00 +99.33 -3.01% -41.78 +5.90% +57.56 -0.44 - In this example, the project has a negative NPV at an RRR of 0.0%, but then the NPV rises as the RRR rises. This is because the present value of the positive cash inflow in Year 1 falls as the RRR rises, but the negative cash outflow in Year 2 rises at a faster percentage rate as it is further in the future. If the negative cash flow in Year 2 rises at a faster rate, then the difference between the Year 1 and Year 2 cash flows will become more positive causing the NPV to rise. If the RRR rises to 11.4%, the project will actually breakeven after which the NPV will become positive. The NPV will remain positive until the RRR reaches 45.5% when the NPV will become negative again. This is because the benefit from the different rates of change in the positive and negative cash flows decreases as the RRR rises and is eventually surpassed by the decline in present value due to the increase in the RRR.

- Again, the IRR is the RRR that results in an NPV of zero. Since the NPV was zero at both an RRR of 11.4% and 45.5%, this means there are two IRRs. The maximum number of IRRs is equal to the number of times the sign of the cash flows changes. The actual number depends on the magnitude of the individual cash flows which will vary with each project. There is usually only one IRR, but users should be aware of potentially confusing results. Using the MIRR instead of the IRR, will eliminate the multiple IRR problem.

- Mutually exclusive projects. IRR and NPV methods give conflicting results when deciding between two mutually exclusive projects. Consider the projects in Exhibit 5:

Exhibit 5: Deciding Between Two Mutually Exclusive Projects

Year Project 1 Project 2 0 -CAD 220 -CAD 220 1 100 30 2 80 70 3 80 110 4 60 130 Total Cash Inflows CAD 320 CAD 340 IRR 18% 16% RRR Project 1 NPV (CAD) Project 2 NPV (CAD) 0% 100.00 120.00 5% 66.27 74.04 6% 60.23 65.93 7% 54.41 58.15 8% 48.79 50.67 9% 43.36 43.48 10% 38.11 36.56 15% 14.35 5.67 20% -5.88 -20.04 Project 1 has a higher IRR than Project 2, but Project 2 has a higher NPV up to an RRR of 9%. After 9%, Project 1 has the higher NPV of the two projects. The NPV results change because even though Project 2 has higher total cash inflows, they are further in the future so are more greatly affected by an increase in the RRR. As the RRR rises, Project 2’s NPV will fall faster than Project 1’s NPV until Project 1 eventually has the highest NPV. Because of this problem, the NPV method should always be used to choose between mutually exclusive projects.

-

6.2 Applying NPV Analysis

Types of Capital Budgeting Decisions

There are two general types of capital budgeting decisions.

- Replacement. NPV measures the difference in cash flows between two alternatives which are to continuing operating an existing asset or to replace it with another asset that is more efficient.

- Standalone. NPV measures the difference in cash flows between two alternatives which are to do nothing or to expand/change a company’s operations in some way.

Data must be collected for both alternatives in a replacement decision. No information is needed for the do nothing alternative in a standalone decision. NPV in each case will measure how much better or worse off a company will be if they undertake the project.

Projects can also be classified as independent, mutually exclusive, or contingent. Independent means they can be accepted along with any other project. Mutually exclusive means two or more projects cannot be done together as they are likely options to accomplish the same task. Contingent means one project has to be completed before another product can begin.

NPV Checklist

When using the NPV method, the following checklist helps ensure that all relevant cash outflows and inflows are considered:

- Initial cash flows

- Cost of assets (cash outflow)

- CCA tax shield on assets (cash inflow)

- Increase or decrease in NWC (cash outflow or inflow)

- Recurring cash flows

- Incremental after-tax net cash flows (cash inflow)

- Terminal cash flows

- Disposal value of assets (cash inflow)

- Lost tax shield on disposal of assets (cash outflow)

- Return of NWC to previous levels (cash inflow or outflow)

- Decommissioning costs (cash outflow

Initial cash flows occur at the start of a project and include the cost of any fixed assets and the tax savings that are realized from claiming depreciation on these assets. Most new projects also require additional net working capital (NWC) although sometimes NWC will fall if more efficient equipment is purchased that operates faster or is less prone to break down. Recurring cash flows include the after-tax net cash flows expected on an ongoing basis over a project’s life. These can come from selling new products, selling additional units of existing products, price increases or cost reductions. Terminal cash flows occur at the end of a project. They include the proceeds from any asset disposals and the lost tax savings from no longer being able to claim depreciation on these amounts. NWC will also return to previous levels. In some industries, companies have to incur considerable decommissioning costs closing down a factory or mine and potentially rehabilitating the site to prevent future environmental problems.

Estimating Cash Flows

When estimating and discounting cash flows using the NPV method, there are a number of important principles to remember.

- Include relevant incremental after-tax cash flows. Only incremental cash flows that specifically relate to a project are relevant in NPV analysis. These cash flows measure the actual costs incurred and benefits received at specific points in time over a project’s life and are not affected by the accounting policies adopted. Determining the effect of taxation on cash flows can be difficult but these amounts are usually significant so they cannot be ignored. Be careful not to miss any relevant cash flows or double count them.

- Use opportunity cost. Projects sometimes use assets that a company already owns. The cost of these assets is not their current net book value but their opportunity cost. Opportunity cost is the price that outsiders are willing to pay for an asset, so it is what the company is giving up when the asset is used in a project. It is determined by an asset’s best alternative use. For example, if a patent was purchased for CAD 50,000, but an outsider is willing to pay CAD 100,000, then CAD 100,000 is what should be included as the initial cost in NPV analysis. If CAD 10,000 is all the company can negotiate, then that amount should be included.

- Ignore sunk costs. Sunk costs are expenditures that cannot be recovered through a sale. Because they cannot be recovered, they are not relevant to a decision. Management accountants say “a sunk cost is no cost.” For example, if a company has already spent CAD 50,000 on a feasibility study for a new project, no cost should be included in NPV analysis unless it can be recovered by selling it to an outside group who is interested in taking over the project. NPV should only include a project’s future costs and benefits and not any sunk costs.

- Incorporate side effects. Consider whether a proposed project will cannibalize or stimulate sales of existing company products. If so, the lost or additional contribution margins should be included in NPV analysis. Also consider how competitors will respond such as by lowering prices or entering the new market. With competition, most excess profits are usually eliminated.

- Consider qualitative factors. A project may have negative side effects like lowering employee morale due to layoffs, environmental problems, or community or political opposition that are difficult to quantify. These factors should be considered and may cause a profitable project to be rejected.

- Be cautious of overhead allocation. Allocations of existing factory or corporate overhead should be ignored. Only include increases in overhead caused by the project and be careful not to underestimate the additional expenditures required.

- Ignore financing costs. Financing costs such as interest paid to debt holders and dividends payments to equity investors should not be included as cash outflows since they are already reflected in the RRR used to determine a project’s NPV. The only exception are issuance costs relating to any new debt or equity raised to finance the project as these costs are usually not be included in the RRR.

- Apply the correct discount rate. RRRs are typically nominal interest rates that include inflation, so future cash flow estimates must incorporate inflation as well otherwise the project’s NPV will be understated. RRR should reflect the riskiness of the proposed project and not the company’s overall cost of capital which is the average of all its existing business units. RRR should also not be the cost of any financing specifically used to fund the project such as a new loan.

Capital Cost Allowance

Under the Income Tax Act (ITC), businesses must adopt capital cost allowance (CCA) as their depreciation method for tax purposes. CCA is a declining-balance depreciation method which categorizes assets into one of 18 different classes. The cost of individual assets in each class are pooled together to calculate CCA. Each class has its own depreciation or CCA rate that is applied to the declining balance or undepreciated capital cost (UCC). This rate generally reflects the expected life of the assets in that class (i.e. longer lasting assets have lower rates) but other considerations such as stimulating investment may result in higher rates (sometimes 100%) and a faster tax write-off.

Most asset classes are subject to the half-year rule which only allows half of the net acquisitions to be included in the class each fiscal year with the remainder added in the subsequent year. Net acquisitions are the net of all asset purchases and sales. The half-year rule was introduced because companies regularly bought assets at yearend but still claimed a full year’s CCA. For convenience, instead of requiring companies to prorate CCA based on the date of purchase, the half-year rule assumes all assets are bought half way through the year. A typical asset class might look like in Exhibit 6:

Exhibit 6: Mechanics or a CCA Pool

| Acquisitions and Disposals | |

|---|---|

| Sales of assets | CAD 7,000 |

| Acquisitions | CAD 31,000 |

| Net acquisitions | CAD 24,000 |

| CCA rate | 20% |

| CCA Class | |

| UCC beginning | CAD 28,000 |

| Half of net acquisitions | 12,000 |

| Balance | 40,000 |

| CCA – Year 1 | (8,000) |

| UCC ending | CAD 32,000 |

| Half of net acquisitions | 12,000 |

| Balance | 44,000 |

| CCA – Year 2 | (8,800) |

| UCC ending | CAD 35,200 |

Although CCA is a non-cash expense and should not be deducted in calculating NPV, being able to deduct CCA for tax purposes does reduce taxes payable which is a cash item. This benefit is referred to as the CCA tax shield and its present value over an asset’s life can be calculated using the formula:

[latex]\text{Present value of CCA tax shield}=\text{(Investment)}\text{(Marginal tax rate)}(\frac{{\text{CCA rate}}}{{\text{CCA rate + RRR}}})(\frac{{2+\text{RRR}}}{{2(1+\text{RRR})}})[/latex]

There are a few asset classes that do not use the declining balance method and the half-year rule to calculate CCA. For example, Class 14 assets (franchises, concessions, patents, and licences) are amortized on a straight-line basis over the life of the property with a full-year’s CCA in the year of acquisition. The present value of the CCA tax shield has to be calculated separately for these classes.

6.3 Incorporating Inflation

In developed economies, central banks typically have general inflation targets of 2.0% per year but in developing markets inflation can be much higher. It is unreasonable to assume that inflation is negligible.

Inflation is incorporated into NPV analysis using either the nominal or real approaches. With the nominal approach, recurring and terminal cash flows are expressed in future dollars which includes an allowance for inflation. To be consistent, the RRR must be expressed in nominal terms as well meaning it has an inflation component. With the real approach, future cash flows are expressed in today’s dollars so no adjustment is made for inflation. Since inflation is not included in future cash flows, it must be taken out of the discount rate resulting in a real RRR. Companies must be careful not to mix up the two methods by expressing all cash flows in today’s dollars while using a nominal RRR.

Rates of return are normally expressed nominally in the financial markets, so the inflation component must be removed from the RRR if the real approach is adopted. If the nominal RRR was 8.0% and inflation was 2.0%, then the real RRR would be 6.0%. This real RRR is only an approximation. An exact rate can be calculated using a formula referred to as the Fischer Effect:

[latex]\text{Nominal rate}=(1+\text{Real rate})\times(1+\text{Inflation rate})-1[/latex]

[latex]0.08=(1.0+\text{Real rate})\times(1.0+0.02)-1.0[/latex]

[latex]\text{Real rate}=0.0588\text{ or }5.88%[/latex]

This formula recognizes that investors must be compensated for inflation on both the original investment (as represented by 1.0 in the formula) as well as the real rate earned during the year. The difference between the Fischer Effect formula and just subtracting the real rate and inflation rate is small, so the Fischer Effect is often ignored.

When incorporating inflation, do not assume the same inflation rate applies to all cash inflows and outflows. Even though the general inflation rate of the economy might be 2.0%, the inflation rate for individual cash flows can vary. For example, commodity price can change dramatically due to shifts in supply and demand and geopolitical forces. Accurate inflation or price forecasts relating to all key inputs and outputs are essential.

Inflation is also problematic for businesses because once any capital costs are added to a CCA pool, they are not subsequently indexed for inflation. This reduces the value of the tax benefits companies receive from deducting CCA. The federal government has considered indexing the value of CCA pools to counter this effect, but has decided against it due to the magnitude of lost tax revenues.

6.4 Capital Rationing

The general rule in capital budgeting is a company should accept all projects with a positive NPV, but this is not always possible. At the divisional level, managers normally receive a limited budget to spend on capital items. If this budget is insufficient to finance all profitable projects, then the division will have to decide how to best allocate or ration these limited funds to maximize NPV. When capital rationing is done at the divisional level, it is referred to as soft rationing.

If divisions are underfunded, it would be logical for a company to simply raise more capital for them. As a company’s assets grow, they are financed with a combination of debt and equity based on the company’s optimal capital structure so not to overleverage the firm. Raising new capital, especially equity, is not always easy. Stock markets can be undervalued for extended periods of time making it ill-advised to issue new equity. Even if stock markets are fairly valued, companies have an aversion to issuing new equity due to high issuance costs and potential control problems. Retained earnings may be insufficient to fund maximum growth given a desired level of dividends, so a company may have no choice but to reduce its growth and ration its limited capital to maximize NPV. A company could also have difficulty raising new funds if it is experiencing financial distress or its loan conditions prevent any additional borrowing. Sometimes, the limitation on the size of the capital is not due to a lack of financing, but a shortage of other non-financial resources such human resources including qualified executives, engineers or marketing specialists. When capital rationing is done at the corporate level, it is referred to as hard rationing.

Capital Rationing Using Solver

If a company has a large number of positive NPV projects to choose from, it would be very difficult to determine which combination maximizes NPV manually. For this, the Solver feature in Excel is an excellent tool. To demonstrate capital rationing using Solver, enter the spreadsheet in Exhibit 7 containing the initial investment and NPV for five different projects along with the formulas. The total amount available to spend on all capital projects is CAD 2,500,000 and Projects A and B are mutually exclusive meaning they cannot both be done. All other projects are independent of each other.

Exhibit 7: Capital Rationing Using Solver

| A | B | C | D | E | F | |

|---|---|---|---|---|---|---|

| 1 | Project | Initial Investment | NPV | Selection | Investment | NPV |

| 2 | A | 1,000,000 | 700,000 | =D2*B2 | =D2*C2 | |

| 3 | B | 2,000,000 | 1,000,000 | =D3*B3 | =D3*C3 | |

| 4 | C | 500,000 | 100,000 | =D4*B4 | =D4*C4 | |

| 5 | D | 500,000 | 85,000 | =D5*B5 | =D5*C5 | |

| 6 | E | 500,000 | 75,000 | =D6*B6 | =D6*C6 | |

| 7 | Total | =Sum (E2…E6) | =Sum (F2…F6 |

Open Solver under the Data tab in Excel. In the drop box, complete the following:

Maximize F7. Done by setting F7 as the objective function and instructing Excel to maximize that value. F7 is the total NPV of all projects selected.

By changing variable cells D2:D6. Excel will select all possible combinations of D2:D6 subject to any constraints.

Constraints.

-

- D2:D6 = Binary. Excel will only select combinations where D2:D6 are either “1” or “0”. A “1” means the project is selected, while “0” means it is not.

- A7 ≤ 1. Cell A7 equals the addition of D2 and D3 which can only be “0” or “1” if Project A and B are mutually exclusive.

- E7 ≤ CAD 2,500,000. Excel will not consider a combination of projects if E7 exceeds the total capital budget of CAD 2,500,000. E7 is the total investment in all projects selected.

Solve. Excel maximizes F7 subject to the constraints and selects Projects B and C with a maximum NPV of CAD 1,100,000.

Instead of using Solver, some companies rank projects based on either their PI or IRR and simply go down the list accepting projects until the capital budget is completely spent. This approach should not be used as it can generate a group of projects that do not maximize NPV. Exhibit 8 contains the same example using a PI ranking.

Exhibit 8: Capital Rationing by Ranking PIs

| Project | Initial Investment (CAD) | Present Value (CAD) | PI |

|---|---|---|---|

| A | 1,000,000 | 1,700,000 | 1.70 |

| B | 2,000,000 | 3,000,000 | 1.50 |

| C | 500,000 | 600,000 | 1.20 |

| D | 500,000 | 585,000 | 1.17 |

| E | 500,000 | 575,000 | 1.15 |

Based on the PI ranking, Projects A, C, D, and E should be chosen. The entire capital budget of CAD 2,500,000 is spent and projects A and B, which are mutually exclusive, are not both selected. As can be seen in Alternative 1 and 2 below, the selection of A, C, D, and E does not maximize NPV though. Alterative 2 maximizes NPV because even though Project B has a slightly lower PI than Project A, the lower PI is earned on a larger investment (CAD 2,000,000 versus CAD 1,000,000) leading to a higher overall NPV.

Exhibit 9: Incorrect Ranking Using PIs

| Alternative 1 | |||

|---|---|---|---|

| Project | Initial Investment (CAD) | Present Value (CAD) | NPV (CAD) |

| A | 1,000,000 | 1,700,000 | 700,000 |

| C | 500,000 | 600,000 | 100,000 |

| D | 500,000 | 585,000 | 85,000 |

| E | 500,000 | 575,000 | 75,000 |

| Total | 2,500,000 | 3,460,000 | 960,000 |

| Alternative 2 | |||

|---|---|---|---|

| Project | Initial Investment (CAD) | Present Value (CAD) | NPV (CAD) |

| B | 2,000,000 | 3,000,000 | 1,000,000 |

| C | 500,000 | 600,000 | 100,000 |

| Total | 2,500,000 | 3,600,000 | 1,100,000 |

6.5 Comparing Projects of Varying Lives

Much of the equipment a company buys such as water pumps or metal lathes is needed on an ongoing basis and must be replaced a number of times in succession as assets wear out. A difficulty in analyzing these types of capital projects is that the equipment options being considered likely have different economic lives making a comparison of their NPVs difficult. Two similar methods for dealing with this problem are chaining and equal annual annuity (EAA). To demonstrate these methods, consider the example in Exhibit 10 of two mutually exclusive equipment options with an RRR of 10.0% and varying lives of three and six years.

Exhibit 10: Chaining and EAA

| Year | Equipment A (CAD) | Equipment B (CAD) |

|---|---|---|

| 0 | -25,000 | -21,000 |

| 1 | 11,640 | 7,325 |

| 2 | 11,640 | 7,325 |

| 3 | 11,640 | 7,325 |

| 4 | 7,325 | |

| 5 | 7,325 | |

| 6 | 7,325 |

Chaining

The lowest common multiple for the lives of the two equipment options is six years. To meet its needs during this six-year period, the company has to purchase Equipment A twice or Equipment B once. For Equipment A, NPV for the first three-year period is added to NPV for the second three-year period. NPV for the second three-year period is discounted for three year since its implementation is deferred. For Equipment B, NPV is calculated for the six-year period. The option with the highest total NPV is selected.

Equipment A

[latex]\text{First 3-year period: }11,640\frac{{1-(1+1.10)^{-3}}}{{.10}}-25,000=3,946.96[/latex]

[latex]\text{Second 3-year period: }\frac{{3,946.96}}{{(1+.10)^{3}}}=2,965.41[/latex]

[latex]\text{Total NPV: }3,946.96+2,965.41=6,912.37[/latex]

Equipment B

[latex]\text{Total NPV: }7,325\frac{{1-(1+.10)^{.6}}}{{.10}}-21,000=10,902.28[/latex]

Equipment Option B is preferred.

EAA

Calculate an annual annuity that is equivalent to the NPV of Equipment A and B. The equipment option with the highest annual annuity is preferred as this annuity will be earned each year regardless how many times the project is undertaken.

Equipment A

[latex]\text{NPV: }11,640\frac{{1-(1+.10)^{-3}}}{{.10}}-25,000=3,946.96[/latex]

[latex]\text{EAA: }3,946.96=P\frac{{1-(1+.10)^{-3}}}{{.10}}P=\text{CAD}1,587.13[/latex]

Equipment B

[latex]\text{NPV: }7,325\frac{{1-(1+.10)^{-6}}}{{.10}}-21,000=10,902.28[/latex]

[latex]\text{EAA: }10,902.28=P\frac{{1-(1+.10)^{-6}}}{{.10}}P=\text{CAD}2,503.24[/latex]

Equipment Option B is preferred.

The chaining and EAA methods can be used to choose between mutually exclusive projects that repeat themselves in the future. The method should not be used to compare one-time projects with different lives. Also, for the project that will be repeated most often, analysts may want to include in the analysis changes in asset replacement costs caused by inflation or changes in technology that make the newer asset more efficient or profitable. In practice, the materially principle and the ability to make accurate estimates should be considered before going to this level of detail.

6.6 Changes in NWC

Previously, any additional NWC relating to a proposed capital project was classified as an initial cash outflow. When the NWC was liquidated at the end of the project, it was classified as a terminal cash inflow. This treatment is an over-simplification as NWC actually changes continuously as sales change over a project’s life and not just at the beginning and end of the project. Sales typically rise quickly but then level out and eventually fall based on a product’s or business’s life cycle. Changes in NWC each period can be estimated using the financial ratio:

This ratio is equivalent to:

[latex]\text{NWC Turnover}=\frac{{\text{Sales}}}{{\text{NWC}}}[/latex]

[latex]\text{NWC}=\frac{{\text{Sales}}}{{\text{NWC Turnover}}}[/latex]

Sales estimates for the proposed project are available. The relationship between sales and NWC as measured by NWC turnover may be assumed to remain constant or can be adjusted to reflect the project’s varying NWC requirements. Knowing sales and NWC turnover, a project’s NWC needs can be calculated each period and the change can be included as either a cash inflow or outflow.

6.7 Taxation Effects of Terminal Cash Flows

With large capital projects involving land, building, equipment and government assistance, determining the relevant cash flows including the tax effects can be complex.

- Land. A negative cash flow is included when land is purchased at the beginning of a project and a positive cash flow is recognized when it is sold at the end. Land is a non-depreciating asset so there are no CCA tax savings, but there is a tax effect relating to any capital gain or loss recognized on the sale of land that must be included in NPV. Under the ITA, only 50.0% of capital gains are taxable and only 50.0% of capital losses can be applied to reduce other capital gains to zero that year. If taxable capital gains are insufficient that tax year to absorb all taxable capital losses, the losses can be applied to taxable capital gains going back three years and forward indefinitely until they are fully realized. By only taxing half of capital gains, the government is encouraging risk taking and recognizing that a significant portion of the capital gain is due to inflation.

- Building. A negative cash flow is included when a building is purchased at the beginning of a project and a positive cash flow is recognized when it is sold at the end. A building is a depreciating asset so the present value of the CCA tax savings are recognized. When the building is sold, the sale price is deducted from the class’s UCC and either a recapture or terminal loss is realized. If the building is sold above its original cost, the original cost is instead deducted from the CCA pool and a capital gain is recognized on the additional amount received. Capital losses cannot occur on depreciable assets. The tax effect of any recaptures, terminal losses or capital gains are included in NPV.

- Equipment. A negative cash flow is included when equipment is purchased at the beginning of a project and a positive cash flow is recognized when it is sold at the end. Equipment is a depreciating asset so the present value of the CCA tax savings are recognized. When equipment is sold, the sale price is deducted from the appropriate class’s UCC. A terminal loss or recapture can occur. If the equipment is sold above original cost, the original cost is instead deducted from the class’s UCC and a capital gain is calculated on the difference. Capital losses cannot occur on depreciable assets. Capital gains on equipment are rare because they generally depreciate in value unlike land and many buildings.

- Government assistance. Both federal and provincial governments provide investment tax credits (ITC) to encourage economic growth. ITC are for investments such as new building and equipment, research and development, resource exploration, or employee training. They are expressed as a percentage of the eligible expenditures and are paid by reducing taxes payable. When ITC are given for the purchase of buildings or equipment, the capital cost added to the CCA class is reduced by the amount of the assistance so the company does not benefit twice. Government assistance is also given in the form of cash grants or wage, rent, interest, and property tax subsidies. The related cash flows should be reduced by the amounts of these payments.

More on Terminal Losses and Recaptures

A terminal loss occurs when an asset class’s UCC is positive and there are no assets remaining in the class. The positive UCC indicates that a company has not taken enough depreciation in the past and can now recognized a tax benefit equal to the class’s UCC times the company’s marginal tax rate. Terminal losses can occur with buildings because each building is held in its own class which must be close out when that building is sold. They are far less likely with equipment as the classes generally contain a number of different pieces of equipment meaning the class is rarely empty.

Recaptures occur whenever an asset class’s UCC is negative regardless of whether the class is empty or not. The negative UCC indicates that a company has taken too much depreciation in the past and now must pay taxes equal to the class’s UCC times the company’s marginal tax rate. Recaptures occur can with buildings because, even though they are depreciable assets, they frequently appreciate in value leading to a negative UCC when the asset is sold. Recaptures are far less likely to occur with equipment because of the positive UCC in the class relating to other assets in the pool and equipment generally does not appreciate in value. If the company is growing at a reasonable rate, this UCC should be sufficient to absorb any asset sales. Even if it is not, good tax planners will arrange to buy needed assets that year so the UCC remains positive thus preventing any recaptures.

As discussed, the tax effect of any capital gains, terminal losses or recaptures relating to equipment must be included in NPV but they are rare. What must be included is the present value of future CCA tax savings relating to the difference between the UCC of the piece of equipment being sold and the amount received from its sale. If this difference is positive, the company will continue to benefit from future CCA tax savings, but if negative, they will lose future CCA tax savings.

6.8 Managing Risk

Capital budgeting is an uncertain process. Companies may be able to estimate a project’s initial cash flows with a high degree of certainty, but recurring and terminal cash flows that are five, ten, or fifteen years away are obviously much more difficult to forecast. Because of this uncertainty, projects that were initially thought to be profitable may actually lose money for the company. This risk cannot be avoided, but it can be reduced. Common methods for managing risk include:

- Establish a minimum payback period. Although NPV should be the primary method used to evaluate projects, companies can adopt a low discounted payback period cut-off point to reduce the risk of losing money. Only projects that meet this more conservative target are considered.

- Subjectively adjust the RRR. Introducing a new product in an unfamiliar market is obviously riskier than replacing existing equipment. If a company uses its weighted average cost of capital as the RRR, the average level of risk for all its current projects is captured. The RRR can be subjectively adjusted upwards or downwards by management to reflect the risk of a specific project as in Exhibit 11.

Exhibit 11: Adjusting RRR for Project Risk

| Category | Project Types | Adjustment Factor | Discount Rate |

|---|---|---|---|

| High risk | New products | +3.0% | 12.0% |

| Moderate risk | New equipment Expansions of existing equipment |

-0.0% | 9.0% |

| Low risk | Replacement of existing equipment | -2.0% | 7.0% |

| Note: Company’s weighted average cost of capital is 9.0% | |||

- Use sensitivity or scenario analysis. Understanding the effect that changes in key variables like price or sales growth have on NPV, IRR or discounted payback period can help companies better manage project risk. Sensitivity analysis can be conducted using the Data Tables feature in Excel to see the effect of changing one variable at a time on NPV. Excel’s Scenario Manager provides companies the option to define and save a number of scenarios consisting of a number of variables and also provides a scenario summary report. The best-case, worst-case, most-likely case scenarios are commonly used in business forecasting.

- Use simulation. This technique is an advanced form of scenario analysis where a large number of variables are selected. A probability distribution is determined for each variable including its mean and standard deviation. By conducting a large number of “runs” where all variables change concurrently based on their probability distributions, a more reliable estimate of the project’s NPV distribution can be made. The mathematical complexity of this methods limits it use, but it is becoming more common in practice. A simulation add-in in Excel called @Risk is available.

- Incorporate management options using decision trees. Selecting a project is not a one-time decision requiring a company to make the entire investment upfront. Large projects are usually divided into multiple stages with specific spending commitments at each stage. Management only proceeds from one stage to the next if further investment is warranted based on new information such as proof of technical or market feasibility or customer demand. Managers also make other decisions subsequent to the commencement of the project based on additional information that increases the project’s NPV and reduces the risk of losing money. These decisions are called management or real options and typically include:

-

- Abandonment. Scale back or abandon a project before the end of its life if sufficient demand does not materialize or costs are higher than expected.

- Timing. Slow or accelerate the implementation of a project in reaction to new information.

- Growth. Expand a project by increasing existing capacity, entering additional markets, or adding complementary products if demand if higher than expected.

- Flexibility. Vary prices, inputs, outputs, and production methods over a project’s life in order to maximize profits.

6.9 Complex Capital Budgeting with Spreadsheets

Advantages of Using Spreadsheets

Spreadsheets are invaluable in capital budgeting as they help to organize and automate a very complex process. By using an input page that defines all of a project’s variables in one place, estimates can be easily changed and sensitivity and scenario analysis employed to test various alternatives.

Need for More Frequent Cash Flow Estimates

For simplicity, when first learning about capital budgeting, students assume that cash inflows and outflows all occur at year end. As shown in Exhibit 12, this yearend assumption can lead to erroneous results when using NPV.

Exhibit 12: Erroneous Resulting Using the Yearend Cash Flow Assumption

| Project A | Project B |

| Capital cost: CAD 10,000 | Capital cost: CAD 10,000 |

| Annual cash inflows: CAD 5,000 | Annual cash inflows: CAD 50,000 |

| Annual cash outflows: CAD 2,000 | Annual cash outflows: CAD 47,000 |

| Life of project: 10 years | Life of project: 10 years |

| RRR: 8.0%, compounded yearly | RRR: 8.0%, compounded yearly |

| NPV Under Different Cash Flows Assumptions | NPV Under Different Cash Flow Assumptions |

| Year-end: CAD 10,130 | Year-end: CAD 10,130 |

| Revenue year-end, costs monthly: CAD 9,645 | Revenue year-end, costs monthly: -CAD 1,273 |

Projects A and B are very similar except for their annual cash inflows and outflows. For both projects, the net cash flows are CAD 3,000 per year over each project’s 10-year life, but the individual cash inflows and outflows are much larger in Project B. If the year-end assumption is used, Project A and B will have the same NPV. But what if the company receives its revenue at year-end and incurs its costs uniformly thorough the year? For Project A, the NPV falls slightly because the costs are being paid sooner, so they are higher on a present value basis thus lowering the NPV. For Project B, the NPV falls by much more and actually becomes negative. This is explained by the size of the individual cash outflows. Because the cash outflows are so large, paying them monthly instead of annually will lead to a much bigger increase in costs thus lowering the NPV.

This example demonstrates that adopting the year-end assumption without reference to the actual timing of cash flows can greatly distort the NPV. It this case, the company would have accepted a project that should have been refused. The year-end assumption will lead to erroneous results when: 1) cash inflows and outflows are large in relation to their net values, and 2) cash inflows and outflows have different frequencies (i.e. monthly or yearly). Both these are true in the case of Project B and are very common in practice. To avoid this problem, cash flows should be measured on a monthly or quarterly basis so they are more accurately timed.

Capital Budgeting Using Spreadsheet

When using spreadsheets to analyze capital budgeting projects as om Exhibit 13, relevant cash flows are still classified as initial, recurring, and terminal, but with some changes. Instead of classifying the present value of the tax savings relating to CCA on the building and equipment as initial cash flows, they are classified as recurring cash flows each month resulting in lower income tax and higher net operating cash flows. The changes to NWC occur over the life of the project and are classified as initial, recurring and terminal cash flows. The tax effects of any capital gains, terminal losses and recaptures on the disposal of land, building and equipment are included in terminal cash flows.

Once the net cash flows are determined for each period, the initial and monthly NPV are calculated by applying the RRR and these amounts are summed to yield the total NPV for the project. The IRR is calculated using Excel’s IRR function with the net cash flows as the data range. This is the monthly IRR since the net cash flows are monthly, so the result must be multiplied by 12 months to yield the annual IRR. Cumulative initial and monthly NPV is an aggregate total of all initial and monthly NPVs. The discounted payback period occurs when this amount becomes positive and remains positive.

Exhibit 13: Format of a Capital Budgeting Spreadsheet

|

|

Initial | Year 1

Month 1 |

Year 10

Month 12 |

|

| Initial cash flows | ||||

| Land | $$$ | |||

| Building | $$$ | |||

| Equipment | $$$ | |||

| Initial change in NWC | $$$ | |||

| Recurring cash flows | ||||

| Sales | $$$ | $$$ | ||

| Cost of sales | $$$ | $$$ | ||

| Non-traceable factory costs | $$$ | $$$ | ||

| Selling costs | $$$ | $$$ | ||

| Administration costs | $$$ | $$$ | ||

| CCA | $$$ | $$$ | ||

| Income tax | $$$ | $$$ | ||

| Net operating cash flows | $$$ | $$$ | ||

| Recurring change in NWC | $$$ | |||

| Terminal cash flows | ||||

| Sale of land | $$$ | |||

| Capital gains tax | $$$ | |||

| Sale of building | $$$ | |||

| Recapture or terminal loss | $$$ | |||

| Sale of equipment | $$$ | |||

| Present value of future CCA deductions | $$$ | |||

| Terminal change in NWC | $$$ | |||

| Net cash flows | $$$ | $$$ | $$$ | |

| RRR | %%% | %%% | %%% | |

| Initial and monthly NPV | $$$ | $$$ | $$$ | |

| Cumulative initial and monthly NPV | $$$ | $$$ | $$$ | |

| Total NPV | $$$ | |||

| Annual IRR | %%% | |||

| Discounted payback | Date |

6.10 Capital Budgeting at Canadian Companies

Capital Budgeting in Practice

The capital budgeting techniques described in this module are all used in industry to varying degrees. Which practices are preferred by companies is an area of considerable research. Academics are trying to determine how closely practice follows current corporate finance theory which is what was studied in this module. More closely adhering to current theory increases corporate profitability and overall economic efficiency and, therefore, is of significant interest. A recent study1 of Canadian businesses found:

- Use of discounted cash flows. Project evaluation methods that use discounted cash flows are “often or always” used by 84% of companies, with 58% using them as their primary method, and 26% using them as their secondary method. Usage is higher among large firms due to their greater sophistication and resources.

- Preferred project evaluation methods. The NPV, IRR, and payback period are the most popular methods. As Exhibit 14 shows, NPV is the preferred method followed closely by IRR and payback period although large firms favour the IRR approach. As discussed, companies typically used more than one method when evaluating a capital project. NPV provides the most reliable measure of profitability, but IRR conveniently expresses the return in percentage form, and payback period provides a valuable measure of project risk.

Exhibit 14: Preferred Project Evaluation Methods in Canada

| Evaluation Method | % Often or Always | Full Sample | Firm Size | |

| Large | Small | |||

| NPV | 74.6 | 2.93 | 2.92 | 2.95 |

| IRR | 68.4 | 2.81 | 3.40 | 2.52 |

| Payback period | 67.2 | 2.78 | 3.04 | 2.73 |

| ARR | 39.7 | 1.76 | 2.04 | 1.67 |

| Discounted payback | 24.8 | 1.18 | 0.61 | 1.34 |

| Adjusted present value | 17.2 | 0.90 | 1.04 | 0.88 |

| Profitability index | 11.2 | 0.53 | 0.32 | 0.60 |

| MIRR | 12.0 | 0.52 | 0.40 | 0.53 |

| Management options | 10.4 | 0.47 | 0.68 | 0.35 |

| Respondents indicate frequency level based on a five-point scale where 0=never, 1=rarely, 2=sometimes, 3=often, and 4=always. | ||||

- Adoption of management options. Researchers generally feel that management options is the most efficient way to allocate capital between projects because of its ability to incorporate flexible decision making into NPV analysis. Regardless, management options is only “often or always” used by 10.4% of firms. It is used primarily by large companies that make major capital investments, are subject to considerable project uncertainty, and have greater flexibility in their investment decision making. This includes mainly natural resource, pharmaceutical and biotechnology enterprises. Companies who do not use management options said it was because of a lack of expertise, its complexity and an inapplicability to their business.

- Incorporating risk. Companies do adjust for project risk when evaluating capital projects but most do so subjectively base on their personal judgement. Sensitivity analysis is also used extensively but more complex methods such as scenario analysis, decision trees, or simulation are not. Large firms are more likely than small firms to incorporate risk into project analysis.

Exhibit 15: Use of Risk-adjustment Methods in Canada

| Risk-adjustment Method | % Often or Always |

| Judgement | 76.9% |

| Sensitivity analysis | 73.5% |

| Scenario analysis and decision trees | 31.9% |

| Simulation | 12.9% |

| Adjusting the payback | 8.6% |

- Judgement is also employed to estimate a project’s future cash flows with 94.0% of firms “moderately or highly” dependent on this approach. Quantitative forecasting methods are “moderately or highly” used by 70.1% of companies, and expert consensus opinion is “moderately or highly” used by 42.7% of companies. Usage of these methods does not vary by firm size.

- Capital rationing. Capital rationing is employed to allocate capital to competing projects when adequate funds are not available. Small firms utilize capital rationing approximately 43% of the time, while large firms utilize it only 34%.

- Differences between countries. U.S. companies are more likely to adopt capital budgeting methods that are consistent with corporate finance theory because that country has a more rigorous corporate governance system and larger firms.

Agency Costs in Capital Budgeting

Another important area of research relates to how agency costs affect the capital budgeting process. According to corporate finance theory, firms should work in the best interest of their shareholders and attempt to maximize the value of the firm by selecting projects with the highest NPV. In practice, managers pursuing their own self-interests prevent companies from achieving this goal. Some typical management behaviours include:

- Empire building. Managers prefer running larger firms especially if their pay is more closely linked to the size of the company and not its financial success. This causes firms to overinvest in capital projects especially if they have considerable financial flexibility in the form of high cash balances or low financial leverage.

- Quiet life. Managers avoid difficult decisions. This results in underinvestment if profitable projects are not pursued, or overinvestment if underperforming products, plants, or divisions are not discontinued.

- Short-term behaviour. Managers select projects that increase short-term instead of long-term share performance. They also underinvest in less noticeable assets like maintenance, employee training, or R&D to improve current results. This short-term focus maximizes a manager’s pay which is closely linked to near-term share performance under most executive compensation plans. It also enhances a manager’s reputation and their current value in the labour market.

- Herding. Managers follow industry investment trends with little regard for the profit potential of the different projects. They feel comfort in following others, and can more easily rationalize their actions and defend their failures.

- Competence. Managers play it safe and avoid investments, especially risker and more costly projects, to hide their lack of competence and avoid being evaluated.

- Overconfidence. Managers are overly optimistic about the assets they control. This causes them to overinvest by exaggerating the profitability of new projects, not cancelling poorly performing products or business units, and overpaying for acquisitions.

- Willingness to issue equity. Managers think their company’s shares are undervalued and are reluctant to issue new equity. This results in underinvestment as companies are forced to ration their capital and turn down positive NPV projects.

Senior management and capital expenditure planning committees must be cognizant of these problems and take steps to mitigate their impact. A company’s strategic plans and performance evaluation and compensation systems must be adjusted so they do not encourage these behaviours.

1Baker, H., Dutta, S., Saadi, S. (2011). Corporate Finance Practices in Canada: Where Do We Stand? Multinational Finance Journal, vol. 15, no. 3/4, 157-192.

6.11 | Exercises

A. Problem: Project Evaluation Methods at Topley

Topley Ltd. is analyzing the purchase of new equipment at a cost of CAD 220,000. It is estimated that it will reduce company cash outflows from operations by CAD 50,000 per year. Its estimated life is ten years, and it will have zero terminal disposal value. The RRR is 16.0%.

REQUIRED:

- Compute the payback period.

- Compute the discounted payback period.

- Compute the NPV.

- Compute the IRR.

- Computer MIRR.

- Compute the PI.

B. Problem: Project Evaluation Methods at Cott Beverages

Cott Beverages is considering the purchase of a bottling machine for CAD 28,000. It is expected to have a useful life of seven years with a zero terminal disposal price. The plant manager estimates the following cash savings:

| Year | Amount (CAD) |

| 1 | 10,000 |

| 2 | 8,000 |

| 3 | 6,000 |

| 4 | 5,000 |

| 5 | 4,000 |

| 6 | 3,000 |

| 7 | 3,000 |

| Total | 39,000 |

Cott has an RRR of 16.0%.

REQUIRED:

- Compute the payback period.

- Compute the discounted payback period.

- Compute the NPV.

- Compute the IRR.

- Compute PI.

C. Problem: Standalone Decision at Rogers

Rogers Company has the opportunity to invest in a new business which requires the purchase of a machine for CAD 120,000. The machine is expected to last for four years and have a salvage value of CAD 10,000. Rogers’ staff has prepared the following budgeted income statement for each of the four years, based on expected sales of 450 units per year.

| Revenues | CAD 90,000 |

| Operating expenses | |

| Operator’s salary | 22,000 |

| Variable supplies | 6,000 |

| Building rental | 3,300 |

| Variable lubrication | 7,000 |

| Depreciation | 27,500 |

| Variable cleaning | 9,000 |

| Total operating expenses | CAD 74,800 |

| Operating income | CAD 15,200 |

Other Information

- The above financial data is based on one shift. The company is confident they can generate sales of 450 units per year.

- A second shift would have to be introduced to produce more than 450 units. The operator for this second shift would have to be paid full salary even if the machine did not operate at capacity and the operator could not be asked to do other work due to strict work rules in the collective agreement.

- The machine would require an additional CAD 5,000 in raw materials and work-in-process inventory to be maintained at all times during the machine’s life.

- The equipment belongs to a CCA class with a 25% rate. The company has many other assets belonging to this class.

- The company’s tax rate is 45% and it has an RRR of 12.0%.

- The inflation rate is negligible.

REQUIRED:

- Should Rogers purchase the new machine?

- Would the recommendation change if the company estimated it could sell 650 units per year?

D. Problem: Replacement Decision at Ruby

On January 1, 2003, Ruby Company was contemplating whether to replace a lathe that it uses to produce Widgets. The current contribution margin (profit after variable costs) is CAD 4.00 per unit.

A new lathe could be purchased for CAD 500,000 and it would last eight years at which time it would be worth CAD 80,000. The old lathe could be sold for CAD 50,000 currently, but could continue to be used for another eight years after which it would have a salvage value of CAD 10,000.

The company currently produces and sells 200,000 Widgets a year, which is expected to increase by 20,000 units with the purchase of the new lathe. Variable production costs are expected to fall by CAD 2.00 per unit. Inventory requirements are expected to increase by CAD 10,000 initially.

The lathe is subject to a CCA rate of 20%. Ruby’s RRR is 10.0% and its tax rate is 35%. The inflation rate is negligible.

REQUIRED:

- Should Ruby buy this new lathe?

E. Problem: Replacement Decision at Zebra

Zebra Technology Ltd. is a manufacturing firm specializing in the production of sophisticated product components. The company is considering the purchase of a new piece of equipment.

The equipment would cost CAD 141,000 and have a salvage value of CAD 18,000 at the end of its six-year life. The new equipment would replace existing devices that are fully depreciated, but have a current market value of CAD 10,000. If the old equipment is kept for another six years, it would have a salvage value of zero.

Zebra Technology is currently selling 50,000 units a year. The new equipment should allow it to sell 15,000 additional units per year over the next six years.

Each unit sells for CAD 12.00 and this is not expected to change over the next six years. Variable costs of production are CAD 7.50 per unit, but this should fall to CAD 5.75 per unit with the more efficient machine. Fixed costs are expected to fall by CAD 10,000 per year. The new equipment will also reduce the required investment in NWC by CAD 30,000.

Zebra Technology has an RRR of 11.5% after tax. These two pieces of equipment are both in a CCA pool with a rate of 20%. The marginal tax rate is 31%. The inflation rate is negligible.

REQUIRED:

- Should Zebra Technology buy this new equipment?

F. Problem: Standalone Decision with Inflation at Weatherly

Weatherly Ltd. operates a large mine. The company wants to purchase equipment to mine additional ore from an undeveloped area of the site. Bernice Janzen, Weatherly’s controller, is analyzing whether to undertake this project.

The cost of purchasing and installing the equipment is CAD 3.5 million. The useful life of the equipment is five years with a salvage value of CAD 450,000.

Weatherly estimates that an additional 6,000 pounds of the metal (16 ounces per pound) will be mined annually for the next five years using the equipment. Janzen has estimated the price of this metal will average CAD 17.21 per ounce over this period. The metal prices are uncertain and are a significant risk in this project.

Two new employees are required to operate the new equipment. Salary and benefit costs for each of these employees are estimated to be CAD 115,000 annually over the next five years. Equipment maintenance is expected to be CAD 65,000 per year.

The variable costs to mine and process the ore is CAD 5.24 per ounce. Allocated existing fixed overhead is CAD 1.95 per ounce.

Janzen uses an RRR of 9.0% and a 21% tax rate to analyze this project. The equipment has a 30% CCA rate. Inflation is estimated to be 2.0% over the next five years.

REQUIRED:

- Determine the NPV of this investment using the nominal approach.

- Determine the NPV using the real approach.

- Is the inflation assumption realistic? Explain.

G. Problem: Standalone Decision with Inflation at Quaker

Quaker Ltd. produces breakfast cereal, but is considering expanding into the packaged salad business. This expansion will require an initial investment in new equipment of CAD 2,500,000. The new equipment will be placed in a class with a CCA rate of 20%. At the end of the project, the equipment is estimated to have a salvage value of CAD 350,000.

Sales from the new venture are forecasted at CAD 2,900,000 per year for the first six years and CAD 3,500,000 per year for years 7 through 12.

Variable operating costs for the new venture are estimated at CAD 1,900,000 for the first six years, and CAD 2,100,000 for years 7 through 12. Fixed costs will be CAD 800,000 per year for the entire 12-year period which includes rent for the new production facility. NWC will average 30.0% of sales throughout the life of the project.

At the end of year 6, an CAD 850,000 overhaul of the new equipment will be undertaken. Under the Income Tax Act, this expenditure is capitalized in the same pool as the original equipment. The half-year rule applies to this expenditure.

It is assumed that at the end of year 12, the equipment will be sold for its estimated salvage value and the overhaul will not affect this estimate. The firm’s marginal tax rate is 30%. The acquisition of the new equipment and any subsequent betterment are subject to an ITC of 5%.

Its RRR is 5.0%, which is used in all NPV analysis. Company policy is to add an additional 3.0% to this discount rate to allow for the extra risk resulting from a new project.

All estimates are expressed in today’s dollars and inflation is estimated to be 2.5% per year for the duration of the project.

REQUIRED:

- Should the proposed project be undertaken? Use the real NPV approach.

H. Problem: Capital Rationing at Bosie

Bosie Ltd. is considering the following capital projects:

| Project | Cost (CAD) | Profitability Index |

| Alpha | 4,000,000 | 1.18 |

| Beta | 3,000,000 | 1.08 |

| Charlie | 5,000,000 | 1.33 |

| Delta | 6,000,000 | 1.31 |

| Echo | 4,000,000 | 1.19 |

| Foxtrot | 6,000,000 | 1.20 |

| Golf | 4,000,000 | 1.18 |

Bosie’s capital budget is CAD 12 million and Charlie and Delta are mutually exclusive.

REQUIRED:

- What projects should be undertaken to make optimal use of the company’s limited capital budget? Use Solver in Excel.

I. Problem: Projects of Varying Lives at Wilson

Wilson Company is trying to decide between two mutually exclusive projects. The relevant cash flows are:

| Year | Project 1 | Project 2 |

| 0 | -55,000 | -60,000 |

| 1 | 23,000 | 15,000 |

| 2 | 23,000 | 15,000 |

| 3 | 23,000 | 15,000 |

| 4 | 23,000 | 15,000 |

| 5 | 23,000 | 15,000 |

| 6 | 15,000 | |

| 7 | 15,000 | |

| 8 | 15,000 | |

| 9 | 15,000 | |

| 10 | 15,000 |

Wilson’s RRR is 7.0%.

REQUIRED:

- Which project would be selected using the chaining method?

- Which project would be selected using the equal annuity method?

- What assumption is made when using both these methods? Is it always accurate?

J. Problem: Projects of Varying Lives at Jensen

Jensen Industries is considering two mutually exclusive investments. The relevant cash flows are:

| Year | Investment A (CAD) |

Investment B (CAD) |

| 0 | -65,000 | -79,000 |

| 1 | 40,000 | 27,000 |

| 2 | 38,000 | 27,000 |

| 3 | 42,000 | 27,000 |

| 4 | 27,000 | |

| 5 | 27,000 | |

| 6 | 27,000 |

The RRR is 8.0%.

REQUIRED:

- Which project should be selected using the chaining method?

- Which project should be selected using the equal annuity method?

- What assumption is made when using either of these two methods? Is it always accurate?

K. Problem: Changes in Net Working Capital at Amsterdam

Amsterdam Ltd. has the option to buy a new machine that will increase sales each year over the project’s 3-year life beginning in 2013.

| 2012 | 2013 |

2014 |

2015 |

| CAD 2,500,000 | CAD 3,400,000 | CAD 3,800,000 | CAD 3,900,000 |

Prior to the undertaking the project in 2013, Amsterdam’s NWC turnover ratio in days was 40.0. This is estimated to increase to 46 days in 2013 due to increased inventory requirements relating to the new machine and then remain the same over the life of the project.

REQUIRED:

- Calculate the changes in net working capital in 2013, 2014, and 2015 that need to be incorporated into the NPV analysis.

L. Problem: Taxation Effects of Terminal Cash Flows

REQUIRED:

For each case below, determine the relevant incremental terminal cash flows.

- Case 1

- A piece of land is purchased for CAD 1,000,000 at the beginning of a project and is sold 10 years later at the end of the project for CAD 4,000,000. The tax rate is 35% and the capital gain inclusion rate is 50%. Inflation is negligible.

- What if the land is sold for CAD 500,000?

- Case 2

- A building is purchased for CAD 500,000 at the beginning of a project and is sold four years later at the end of the project for CAD 600,000. The asset is in a pool with a CCA rate of 10%. The half-year rule applies. The tax rate is 35% and the capital gain inclusion rate is 50%. Inflation is negligible.

-

Year 1 Year 2 Year 3 Year 4 Year 5 UCC CAD 500,000 CAD 475,000 CAD 427,500 CAD 384,750 CAD 346,275 CCA CAD 25,000 CAD 47,500 CAD 42,750 CAD 38,475 - What if the building is sold for CAD 100,000?

- Case 3

- A piece of equipment is purchased for CAD 500,000 at the beginning of a project and is sold five years later at the end of the project for CAD 50,000. The asset is in a pool with a CCA rate of 30%. The half-year rule applies. The equipment is one of many assets in the pool. The RRR is 10.0%. The tax rate is 35% and the capital gain inclusion rate is 50%. Inflation is negligible.

-

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 UCC CAD 500,000 CAD 425,000 CAD 297,500 CAD 208,250 CAD 145,775 CAD 102,042 CCA CAD 75,000 CAD 127,500 CAD 89,250 CAD 62,475 CAD 43,733 - What if the equipment is sold for CAD 120,000?

- What if the equipment is sold for CAD 600,000?

M. Problem: Managing Risk by Adjusting the Discount Rate at Rexall

On June 1, 2006, Rexall Ltd. was investigating whether to replace one of its existing injection molding machines with a new model being sold by one of its equipment vendors.

The new equipment will cost CAD 85,600 plus sales taxes of CAD 5,992, transportation of CAD 1,000, and installation of CAD 2,500. It is expected to last 10 years at which time it will have an estimated salvage value of CAD 12,000. The current injection molding machine has a market value of CAD 45,500 and will also last another 10 years at which time it will have a salvage value of approximately CAD 1,500.

The current machine produces 580,000 units per year, which sell at CAD 1.50. The new model is expected to increase output by 55,000 units and decrease current variable production costs of CAD 1.29 by CAD 0.35. Fixed costs will rise by an estimated CAD 10,000 per year due to more complicated maintenance. The new machine is considered more reliable than the current model, so the company feels it will be able to reduce its inventory requirements by CAD 25,000. All additional output can be sold.

Engineers estimate that the machine will have to be overhauled after five years and that this will cost CAD 200,000. Output is expected to be no more than 580,000 units for the five years after the overhaul.

The injection-molding machine is subject to a CCA rate of 25%. Rexall’s nominal RRR is 11.0%, and profits are subject to a marginal tax rate of 32%. Inflation is estimated to remain at 2.5% over the life of the machine.

The policy at Rexall is to adjust the company’s required rate of return to reflect the specific risk of each project. The following adjustment table is used:

| Category | Examples | Adjustment Factor |

| High risk | New products | +2.0% |

| Average risk | New equipment | 0.0% |

| Low risk | Replacement of existing equipment | -2.0% |

| Mandatory | Pollution control equipment | Not applicable |

REQUIRED:

- Should the proposed project be undertaken? Use the real NPV method.

N. Problem: Managing Risk by Adjusting the Discount Rate at Dodson

Dodson Industries is trying to select the best of three mutually exclusive projects with varying levels of risk. Project A is in risk class 5, Project B is in risk class 2, and Project C is in risk class 3.

| Project A | Project B | Project C | |

| Initial Investment | CAD 185,000 | CAD 240,000 | CAD 315,000 |

| Year | After-tax Cash Inflows | ||

| 1 | CAD 85,000 | CAD 55,000 | CAD 95,000 |

| 2 | 75,000 | 65,000 | 95,000 |

| 3 | 75,000 | 75,000 | 95,000 |

| 4 | 65,000 | 85,000 | 95,000 |

| 5 | 65,000 | 95,000 | 95,000 |

| Risk Class | Name | Risk-Adjusted RRR (%) |

| 1 | Low risk | 7.0 |

| 2 | Low-to-average risk | 10.0 |

| 3 | Average risk | 12.0 |

| 4 | Average-to-high risk | 16.0 |

| 5 | High risk | 19.0 |

Inflation is negligible.

REQUIRED:

- Which project should be undertaken?

O. Problem: Managing Risk through Management Options at Hansen

Hansen Industries is contemplating developing a new product for sale in the domestic market. It has decided to utilized decision tree analysis with management options and has broken down the project into the following phases:

Phase 1

At the start of Year 1, Hansen will complete a technical feasibility study at a cost of CAD 620,000. They estimate there is a 70% chance that the results will favour further development.

Phase 2

At the start of Year 2, if Hansen decides to proceed, they will invest CAD 1,000,000 to build a protype of the product. Hansen estimates there is 60% chance that the protype will be suitable for sale.

Phase 3

At the end of Year 2, if Hansen decides to proceed, they will build a manufacturing facility for CAD 9,000,000

Phase 4

During Year 3, Hansen will begin selling their product. There is a 50% chance that demand will be strong generating net cash flows of CAD 17,500,000 a year for three years. There is a 30% chance that demand will be average generating net cash flows of CAD 7,500,000 a year for three years. There is also a 20% chance that demand will be low generating negative net cash flows of CAD 3,000,000 a year for three years. If demand is low in Year 3, the firm will terminate the project and avoid the negative cash flows in Years 4 and 5. If demand is high, the capacity of the plant will be expanded and the price of the product raised increasing cash flows to CAD 22,500,000 in Years 4 and 5.