Module 7: Business Valuation

Accountants and financial analysts must frequently estimate the fair market value of a business enterprise, its individual assets and liabilities, or damages that it has caused or incurred as a result of actions such as breach of contract or patent infringement. Fair market value is the price that willing and rational buyers and sellers with full information agree upon.

Business valuation is a complex process that is prone to errors because of difficulties accurately forecasting a company’s future operations. This is why having an experienced professional with a background in valuations is so important to an organization. In Canada, professionals can earn the Chartered Business Valuator (CBV) or Chartered Financial Analyst (CFA) designations to develop their skills in this important area. Many public accounting firms offer business valuation services in addition to their traditional services in business advisory, taxation, financial reporting and insolvency. Investment bankers apply valuation principles when advising clients on public offerings or corporate restructurings. Venture capitalists employ them to price start-up companies.

The income, market multiples, asset-based and residual income approaches are used to value a business. With the income approach, a business’ future operating cash flows are forecasted and then discounted using an appropriate cost of capital. The market multiples approach is a simpler method that uses industry average ratios such as price/ earnings, price/book value or price/sales. These ratios are multiplied by a company’s own earnings, book value, or sales per share to determine its fair market value. The asset-based approach takes a business’ historical cost balance sheet and restates its total assets and liabilities at fair value and possibly includes an estimate of goodwill. Finally, residual income starts with a firm’s book value and adds any income a business expects to earn in excess of its equity investor’s required rate of return.

These business valuation methods are also used in Module: Mergers and Acquisitions and Corporate Restructuring to determine take-over bids for business acquisitions.

7.1 | Business Valuation Basics

Definitions of Value

The value of a business can be defined in a number of different ways.

- Market value. The price that a business or its specific assets or liabilities trade at in efficient markets.

- Fair market value. The price that a business or its specific assets or liabilities should trade at in efficient markets. Fair market value is estimated by business valuators when a market value is not available or markets are not operating efficiently.

- Investment or acquisition value. By combining two companies, the acquirer is able to realize synergies such higher prices or economies of scale that justify paying more than the target firm’s fair market value.

- Intrinsic value. This is what an equity analyst believes a firm is truly worth after considering all relevant information and eliminating any short-term pricing irregularities. If financial markets are efficient, the intrinsic value should match the market value or the fair market value meaning there is no mispricing due to market inefficiencies. Passive investors believe markets are efficient and typically invest in stock index mutual funds or exchange traded funds (ETFs) with minimal stock turnover. Active investors think that abnormal returns or alphas can be earned by identifying mispriced shares. If the current share price in lower than its intrinsic value, the analyst will issue a buy recommendation believing the company is undervalued. The opposite will happen if the share price in above its intrinsic value. Continuous trading in search of alpha results in high stock turnover.

- Going-concern value. The value of a company and its specific assets and liabilities when it is assumed the business will continue to operate with the goal of maximizing shareholder value. Companies trade at a premium to the value of their net assets and liabilities because of the goodwill an organization is able to generate through its strong reputation, experienced workforce, and established systems and procedures. Market, investment, and intrinsic value all assume a business will continue to operate as a going concern.

- Liquidation or breakup value. The value of a business or its specific assets or liabilities when it is assumed that the company will discontinue its operations. The liquidation value is generally below the going-concern value, but in some cases when a company is poorly managed, under competitive pressure, or experiencing financial distress, this may not be true. These firms are said to be worth more “dead than alive.”

Applications of Business Valuation

There are many situations where a company needs to value a business or its specific assets or liabilities. The most important include:

- Private company transactions. The majority of corporations are privately held by a small group of investors including the founder(s), their family members, managers, and employees. These investors may want to buy additional shares or to sell them upon their death, disability, termination of employment or if they decide to retire, change jobs, or diversify their investment portfolios. These shares do not trade publicly, so business valuators provide a fair market value estimate. Valuators also help improve the company’s operations prior to sale so shareholders receive the best possible price. This includes finding interested buyers, overseeing the bidding processes, and completing all formal purchase or shareholder/partner rights agreements.

- Initial or secondary public offerings. Private companies go public to increase their access to capital and provide investors with greater market liquidity when selling their shares. Secondary offerings are used by public companies to raise additional equity capital to fund growth opportunities when retained earnings are insufficient. Business valuators help determine an appropriate offering price in both situations.

- Buy, sell or hold recommendations. Major public companies are followed on an on-going basis by a group of equity analysts who regularly issue earnings forecasts and formal research reports. In these reports, analysts make buy, sell or hold recommendations to their clients based on a thorough review of the company, its industry, and the overall economy and an estimate of the share’s intrinsic value.

- Timing stock repurchases. Stock repurchases provide management with greater financial flexibility as they are not committed to paying regular cash dividends. Repurchases are best made when a company’s shares are undervalued so to benefit the remaining shareholders. A business valuation helps determine when these shares are mispriced.

- Internal management. A manager’s primary goal is to maximize shareholder value, so they want to know if their firm’s share is undervalued. If it is, they will act to correct the market’s misperception. Management also wants to know the effect new strategic initiates will have on the share price, so they can better sell these ideas to the firm’s board of directors, shareholders, and stock analysts.

- Take-over bids. Companies sometimes buy other businesses to generate synergies for themselves or the target firm leading to a higher share price post acquisition. Business valuators carefully measure these synergies so the acquirer does not over pay.

- Fairness opinions. If shareholders receive a take-over bid from a potential acquirer, management must provide them with a fairness opinion before the offer expires. This opinion includes a valuation of the company and a recommendation whether to accept or reject the offer.

- Ownership percentages for venture capitalist. Venture capitalists provide needed financing to risky start-up companies when other investors will not. The value of a start-up must be measured, so the venture capitalist receives an appropriate portion of the firm’s equity in exchange for their investment. This is particularly difficult for new companies as their growth prospects are uncertain and their shares do not yet trade publicly.

- Valuing divestiture, spin-off or going private transactions. A company may sell or spin-off part of its operations for a variety of reasons such as to focus on its core business or to raise needed capital. A majority owner or group of managers may also decide to take a public company private to avoid the scrutiny of the financial markets so they can focus on a business turnaround. A business valuator needs to determine an appropriate asking price.

- Liquidations or reorganizations. When a company experiences financial distress and is declared bankrupt by the courts, it can either sell its assets and pay what it raises to its creditors (i.e. liquidation) or attempt to restructure its operations with the goal of successfully re-emerging from bankruptcy (i.e. reorganization). Being able to accurately value a business’ assets is critical to getting the most possible for creditors in a liquidation. In a reorganization, valuation principles are used to determine the percentage ownership creditors will receive in a debt-for-equity swap or in exchange for new equity financing.

- Share-based compensation. A large portion of management compensation comes from stock options and restricted shares in order to directly tie pay to share performance thus reducing agency costs. Business valuation tools are used to design these plans so they provide adequate compensation.

- Fair value accounting in financial reporting. International Financial Reporting Standards (IFRS) allow companies to report many of their tangible and intangible assets and liabilities at fair market value instead of historical cost to improve the quality of financial reporting. Intangible assets like brand names or trademarks are particularly difficult to appraise. Valuation principles are also used to allocate the purchase price in a business acquisition between a company’s fixed assets, intangible assets, and goodwill and to measure any subsequent goodwill impairments.

- Transfer pricing. Transfer pricing provides an accurate measure of a division’s or geographic area’s performance by fairly valuing intercompany sales. Companies may manipulate transfer prices to lower taxable income in a high-tax jurisdiction or increase profits in a certain business unit. Business valuators can help companies establish fair transfer pricing systems, mediate any company disputes, and provide expert testimony when the fairness of transfer prices is challenged in the courts.

- Fair value of assets for tax purposes. Under the Income Tax Act (ITA), an asset’s fair market value is used to calculate any capital gains taxes owed in a deemed disposition of property or a non-arm’s length transaction. A deemed disposition occurs when a person is considered to have disposed of property even though a sale did not occur. This is common with the transfer of property as a gift or when a business is given or sold to a family member upon the death of a taxpayer. Non-arm’s length transactions are with related persons where the fairness of the consideration is usually questioned.

- Litigation support. The fair market value of damages must be quantified for cases such as breach of contract, insurance claims, intellectual property infringement, business interruption, product or professional liability, asset expropriations, construction contract matters, personal injury, matrimonial property issues, or disputes with minority shareholders. If the parties cannot reach an agreement, the matter is referred to the courts and a business valuation professional may be asked to provide expert testimony concerning appropriate damages.

Sell-Side and Buy-Side Analysts

Financial markets are divided into sell-side and buy-side activities. The sell-side primarily consists of investment bankers who construct, promote and sell financial instruments such as stocks, bonds, and derivatives. These securities are sold to the buy-side of the market consisting of both retail and institutional investors including pension plans, insurance companies, banks, trust companies, hedge funds, mutual funds, ETF companies, and other investment management firms.

Investment banks employ sell-side analysts to assist in pricing initial and secondary public offerings and provide ongoing coverage of these shares in the secondary market. The earnings forecasts, research reports, and buy, sell, or hold recommendations these sell-side analysts provide are valuable sources of information. The website of a large corporation typically lists the sell-side analysts that follow their firm.

Buy-side analysts work for institutional investors making recommendations that are used in managing their funds. These analysts collect information from company financial disclosures, sell-side analysts, conference calls with management, company visits, and financial information firms such as Bloomberg or Thomson Financial. Any information is typically used by the institutional investor only and is not shared with the public.

Whether the investment recommendations made by sell-side analysts are objective is a contentious issue in the investment industry. Investment bankers directly benefit from any favorable coverage provided by their sell-side analysts through a higher initial public offering price or a corporate client’s promise of future investment banking work. Many investment bankers also provide investment advisory services to individual and institutional investors. Financial firms do attempt to separate the activities of these units through strict ethical standards relating to the exchange of information. Despite this, investment advisory clients worry that financial advisors will be forced to purchase shares on their behalf to support a corporate client’s share price contrary to their best interests. The movement of insider information between the investment banking and investment advisory units about possible corporate acquisitions, changes in dividend policy, or other corporate finance issues that will affect the share price is also a concern.

7.2 | Income Approach – Dividend Discount Model

The value of any asset is equal to the present value of the future cash flows investors will receive. For a rental property, the cash flows are the rental payments minus any cash expenses. For a bond, they are the regular interest payments plus the return of principal at the end of the bond’s life. Determining the value of a business and its equity securities is no different. A share’s value is equal to the present value of all future dividends that are paid to the common shareholders. Preferred share dividends are not included as they are considered debt payments for valuation purposes. These shareholders are not entitled to any of the business’ residual income like common shareholders but only fixed payments like bond holders.

It is impossible to tell exactly how long most companies will survive, so valuators adopt the going concern principle and assume that their dividends will grow indefinitely. Lower dividends now will mean higher dividends in the future as earnings are re-invested in the business. Obviously, it is very difficult to accurately estimate the value of anything over an indefinite period. To deal with this uncertainty, business valuators use three variations of the dividend discount model (DDM).

Variations of the DDM

- One-stage or constant growth. This model assumes that dividends grow indefinitely at the same rate. Using the present value of a perpetuity with growth formula, the intrinsic value (V0) of a business today can be determine based on estimates of next year’s dividend (D1), the appropriate cost of common equity (kc), and the expected long-term growth rate of the company’s dividends (gd).

- [latex]V_{0}=\frac{{D_{1}}}{{k_{c}-g_{d}}}[/latex]

- This model is best used to value mature companies with stable long-term earnings and dividend growth rates and a consistent relationship of dividends to earnings (i.e. a stable dividend payout ratio) over time.

- The growth rate cannot exceed the nominal growth rate of the economy which is normally 2.0% to 3.0% or the company will essentially become the economy over the long term, but it can be less for slow-growth, no-growth or negative-growth companies. The cost of common equity reflects the risk level of the asset being valued. Calculating the appropriate cost of common equity, cost of debt and the weighted average cost of capital were examined in Module: Cost of Capital. For simplicity, the capital asset pricing model (CAPM) will be used throughout this unit to estimate the cost of common equity. CAPM states:

-

[latex]k_{c}=k_{f}+B_{a}(k_{m}-k_{f})[/latex] [latex]k_{c}=\text{Cost of common equity}[/latex] [latex]k_{f}=\text{Risk-free rate}[/latex] [latex]B_{a}=\text{Beta of an asset}[/latex] [latex]k_{m}=\text{Market rate}[/latex] [latex]k_{m}-k_{f}=\text{Market risk premium}[/latex] - Two-stage. This model is more flexible as it allows for a high-growth stage of varying lengths initially possibly due to a new product innovation followed by a mature-growth stage with lower growth once industry competition intensifies, new companies enter the market, and demand stabilizes. The value of the firm relating to the mature-growth stage only is called the investment’s terminal value.

- [latex]V_{0}\frac{{(D_{0})(1+g_{\text{d high}})^{1}}}{{(1+k_{c})^{1}}}+\frac{{(D_{0})(1+g_{\text{d high}})^{2}}}{{(1+k_{c})^{2}}}+\frac{{(D_{0})(1+g_{\text{d high}})^{3}}}{{(1+k_{c})^{3}}}+\frac{{\frac{{(D_{0})(1+g_{\text{d high}})^{3}(1+g_{\text{d low}})^{1}}}{{(k_{e}-g_{\text{d low}})}}}}{{(1+k_{c})^{3}}}[/latex]

- In practice, a valuator typically includes a supernormal growth rate estimate based on their own research for the first stage which is usually three to five years. Estimating growth accurately after that is difficult, so valuators typically assume a second-stage growth rate that approximates the long-term growth rate of the economy or less as in the one-stage DDM.

- Three-stage. This model improves on the two-stage model by allowing a more gradual transition from the high-growth to the mature-growth stage by introducing a middle stage where the growth rate declines in a linear pattern. It is unreasonable to expect the change in the growth rate to occur in just one year. The length of this transition stage is subjectively determined and varies with each analyst. If the high-growth rate immediately starts to decline over a period of time until it reaches the mature-growth rate this is referred to as the H-Model.

Estimating the Dividend Growth Rate

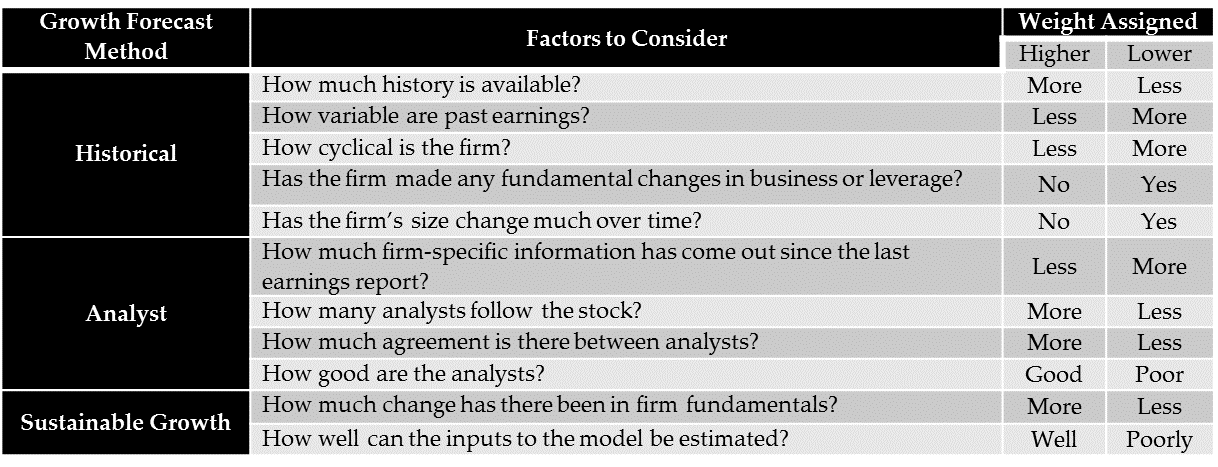

Dividend growth rate can be estimated using a company’s historical growth rate, forward-looking growth rate, or sustainable growth rate (SGR).

- Historical growth rate. This growth rate is calculated based on either dividends or earnings or sales as a proxy for dividends. Dividends are typically more stable than earnings or sales, but the trend of substituting stock repurchases for dividends makes this amount less reliable. Stock repurchases can be incorporated into the DDM by using total distributions which are cash dividends plus stock repurchases, but repurchases are typically unstable making them difficult to forecast.

- Geometric mean provides a more accurate measure of growth compared to arithmetic mean especially when the historical growth rates have been erratic. Geometric mean is less accurate when only the first and last values are used or if either of these two values are negative, so regression smoothing should be employed. Always estimate growth over a full business cycle to average out yearly fluctuations. Adjust earnings for aggressive revenue recognition, excessive cost capitalization, deferral of discretionary costs, timing of gains and losses, or non-recurring items if the information is available. Earnings should be expressed on a diluted per share basis otherwise earnings can be raised simply by issuing more equity and earning a return.

- Research indicates that historical growth rates are not highly correlated with future growth rates. More variable historical growth rates are poorer indicators of future growth. Historical growth rates are also not good predictors of future growth rates if a company is experiencing changing competitive forces, government regulations, business mix, operations, capital structure, or dividend policy.

- Forward-looking growth rate. This growth rate is generally more accurate than a historical growth rate as it is based on forward-looking information that is not reflected in past earnings. Valuators can use their own estimates, the estimates of a particular equity analyst who follows the company, or a consensus forecast of these analysts. Financial information service firms provide consensus growth forecasts. When using the future growth rate estimates of other analysts, ensure they are not sell-side analysts that work for financial firms who have a business relationship with the company being valued. Buy-side analysts are usually much more objective.

- Research shows that forward-looking growth rates are more accurate than historical growth rates in the short term, but provide little superiority past three to five years. Using a high number of quality analysts provides better forecasts, so select analysts with the most accurate past predictions. More disagreement among analysts means consensus forecasts are less reliable.

- Sustainable growth rate. This is the growth rate of sales that a company can support using retained earnings only while maintaining constant financial fundamentals including its rate of return on equity (ROE) and retention ratio (R). ROE is a function of a firm’s rate of return on assets (ROA) and debt ratio (DR) while ROA is determined by its net profit margin (NPM) and total asset turnover (TAT). Growth rate in sales is a proxy for earnings and dividends growth.

- [latex]\text{Formula 1 }SGR=\frac{{((ROE)(R))}}{{(1-(ROE)(R))}}[/latex]

- [latex]\text{Forumla 2 }ROE=\frac{{(\text{Net income / Sales})\times(\text{Sales / Total assets})}}{{(1-(\text{Total debt})/(\text{Total assets}))}}[/latex]

- Most companies try to grow using retained earnings only because:

- Issuing new equity may create control problems for existing shareholders.

- Issuance costs for new equity are high especially for start-ups and small businesses.

- Start-ups and small businesses may have exhausted all sources of new equity.

- Earnings per share is diluted in the short-term as it takes time for new equity to be effectively utilized.

- Managers are concerned about raising new equity when their shares are undervalued as it hurts existing shareholders.

- SGR is also useful for valuing firms that have recently undergone significant operational and financial changes as their historical data is not representative of the future.

The historical growth rate, forward-looking growth rate, or SGR can be used alone or combined by calculating a weighted average of the three methods. Exhibit 1 outlines the different factors that should be considered when choosing the best method or deciding on the appropriate weights.

Exhibit 1: Selecting a Growth Rate

Source: Damodaran, Investment Valuation, 1996.

Applying DDM

Other factors to consider when applying the DDM include:

- The higher the growth rate during the growth stage, the shorter the growth period will likely be as growth regresses to the mean faster.

- Multi-stage models allow for non-payment of dividends initially but in practice this is difficult to implement because a lack of dividend history makes estimating future dividends problematic.

- Payout ratios, betas, growth rates, ROAs, and debt ratios vary by DDM stage. Spreadsheet modelling is used to deal with this complexity and ensure all estimates are consistently applied. As companies go from the growth to the mature stage, ROA falls as growth opportunities disappear and competition eliminates abnormally high profit margins. Payout ratios rise as less funds are needed for expansion. Debt ratios rise as mature companies become more stable and appealing to lenders. Beta falls as investments become less risky.

- Business valuators typically put little effort into determining the terminal value of a company other than to estimate the long-term growth rate, yet it accounts for a very high proportion of the firm’s value.

- Small variations in inputs such as kc and gd result in significant differences in valuations, so great care must be taken estimating these variables. Sensitivity or scenario analysis are used to test the effect of any potential errors.

- DDM only determines the fair market value of a non-controlling stake in a business when investors have no ability to influence the dividends paid. If an investor acquires a controlling interest, then another valuation approach should be adopted.

Implied kc or gd

Sometimes business valuators are not interested in the exact value of an asset, but only want to know if it is currently under or overvalued. This can be determined by using the one-stage, two-stage or three-stage models and manipulating the formula to isolate for either kc or gd.

[latex]k_{c}=\frac{{(D_{0})(1+g_{d})}}{{V_{0}}}+g_{d}[/latex]

[latex]g_{c}=\frac{{(V_{0})(k_{c})-D_{0}}}{{V_{0}+D_{0}}}[/latex]

All other values are then entered into the formula, and an implied kc or gd is calculated. If kc is higher than the appropriate benchmark value, then the asset is likely undervalued as its current price is based on too high of a risk level. Overtime, the price should rise as the kc falls to the appropriate benchmark as market inefficiencies are corrected. If gd is higher than the appropriate benchmark value, then the asset is likely overvalued as its current price is based on too high of a growth rate. Overtime, the price should decline as the gd falls to the appropriate benchmark as market inefficiencies are corrected. The analysis is reversed if the kc and gd are initially lower than the benchmark.

Business valuators may apply this technique to individual companies, entire industries, or the stock market as a whole to determine if they are over or under valued. Many investors do not purchase individual stocks, but instead buy or sell entire industries or stock indexes based on their assessment of whether they are mispriced.

7.3 | Income Approach – Free Cash Flows

Free Cash flow to Equity

The present value of dividends does not always accurately measure a firm’s value. Some companies do not pay dividends, while others pay dividends that are either well below or above what they should be paying for different reasons such as:

- Do not want to signal to the stock market that they are experiencing financial difficulties.

- Increase their financial flexibility by maintaining high cash reserves and a sub-optimal debt level.

- Reduce issuance costs by using retaining earnings only to fund growth.

- Retain cash for unprofitable investments and expensive management perks.

- Substitute stock repurchases for cash dividends to lower taxes paid by investors.

- Deceive the stock market into thinking their performance is better than justified.

To correct this problem, free cash flow to equity (FCFE) is substituted for dividends. FCFE is the residual cash remaining after a company pays for all its capital investments net of any financing. Agency theory says this cash should be paid out as dividends to the common shareholders since the company has no other positive net present value projects in which to invest. Shareholders can then redeploy this capital to other more profitable investments. FCFE is useful when an investor acquires a controlling position in another company as they have the ability to adjust the dividend to the level that maximizes shareholder value.

FCFE is calculated as:

[latex]\text{Formula 1 } FCFE=NI+NCC-\delta NWC-CE+NB[/latex]

Explaining the FCFE formula, net income (NI) is converted into cash flow by adding back non-cash charges (NCC) such as depreciation (D) and gains/losses on asset sales and deducting any change in net working capital (NWC). Capital expenditures (CE) are then deducted. Only a portion of CE are paid for in cash, so new debt minus principal payments or net borrowing (NB) is added back.

FCFE can also be calculated using two other equivalent formulas:

[latex]\text{Formula 2 }FCFE=CFO-CE+NB[/latex]

[latex]\text{Formula 3 }FCFE=NI-(CE-D)(1-DR)-\Delta NWC(1-DR)[/latex]

The formula 2 is equivalent as CFO includes adjustments for NCC and the change in NWC. Formula 3 is an algebraic manipulation of formula 1, except it only includes D instead of all NCC as it assumes D is the largest component of NCC which it is normally true.1 Multiplying by one minus the debt ratio (1 – DR) provides the portion of CE or the change in NWC that is paid in cash. Multiplying by (1 – DR) also allows valuators to use an estimate of the forward-looking debt ratio instead of the current NB.

Once FCFE is estimated for future periods, it can be substituted for dividends in the one-stage, two-stage, or three-stage growth models to calculate the value of the firm. Like dividends, FCFE is carefully estimated for each of the next three to five years and then more generally in subsequent periods. Proforma financial statements are prepared using the percentage of sales method based on a sales forecast. Inputs for any of the formulas can be taken from these proformas. These skills are developed in Module: Financial Planning and Growth and Module: Business Forecasting.

Applying the FCFE Model

Other factors to consider when applying the FCFE model include:

- Preferred shares are considered debt and not equity for valuation purposes so any dividends or sinking fund payment should be treated as interest and principal.

- CE and NWC needs will vary with growth in sales.

- CE are normally greater than D in the growth stage but this difference narrows and approaches zero as the company matures.

- Like DDM, small variations in inputs such as kc and gd result in significant differences in valuations, so great care should be taken estimating these variables. Sensitivity or scenario analysis are used to test the effect of any potential errors.

- If an investor acquires a controlling interest in another company, any potential synergies can be included in FCFE to determine the firm’s investment or acquisition value.

Free Cash Flow to the Firm

Some analysts feel using free cash flow to the firm (FCFF) produces a more accurate business valuation than FCFE. FCFF is the residual cash remaining for investors after making all investments in NWC and CE. Investors include not only common shareholders but debt holders and preferred shareholders as well. FCFF can be calculated using either of two equivalent formulas:

[latex]\text{Formula 1 }FCFF=EBIT(1-TR)+NCC-CE-\Delta NWC[/latex]

[latex]\text{Formula 2 }FCFF=CFO+(I)(1-TR)-CE[/latex]

The FCFF formula is similar to the formula for FCFE except interest (I) is removed from NI by using earnings before interest and taxes (EBIT) times one minus the tax rate (1- TR). NB is eliminated entirely as it relates to debt and preferred shareholders who are now considered investors. When FCFF is substituted for FCFE in the one-stage, two-stage, or three-stage growth models, the value of the firm or its enterprise value is from the perspective of all investors. Because of this, the discount rate used is the company’s weighted average cost of capital (WACC) and not its cost of common equity.

| [latex]WACC=(W_{d})\times(k_{d})+(W_{p})\times(k_{p})+(W_{c})\times(k_{c})[/latex] | |

| kd – Cost of debt | Wd – Weight of debt |

| kp – Cost of preferred shares | Wp – Weight of preferred shares |

| kc – Cost of common shares | Wc – Weight of common shares |

To determine the value of the firm to the common shareholders only, the market value of the company’s debt and preferred shares are then deducted.

The income approach based on FCFF is similar to using FCFE, but it has a number of advantages. FCFF is less likely to be negative due to the greater use of financial leverage (i.e. higher interest costs) or the cyclical nature of the business. If financial leverage is expected to change significantly in the near term, FCFF will be easier to estimate than FCFE. Also, WACC is more stable than the cost of common equity and reliable market values for debt and preferred shares are available if these securities trade in active secondary markets.

Special Applications of the Income Approach

- Non-operating assets. Dividends, FCFE or FCFF do not include the value non-operating assets such as idle land or excess cash since these assets typically do not generate income. A firm’s value should be increased by the fair market value of these assets. Marketable securities such as stocks or bonds do generate income, but a more accurate valuation can be obtained by removing any income from FCFE or FCFF and adding the market value of the securities to the value of the firm.

- Multi-unit businesses. For companies with a number of business units in different industries, valuing each of the units separately and then adding them together will likely provide a more accurate valuation.

- Cyclical companies. Using figures such as sales, net income, EBIT or CFO from a cyclical business without normalizing them over a full business cycle will result in serious valuation errors. When normalizing these amounts, valuators should not just average past values as they grow naturally due to changes in the size of the business. This can be addressed by scaling them using company average ratios. Income measures also vary overtime as the nature of the company changes or if it experiences one-time operational problems. The solution is to scale them using industry average ratios or rating firm results instead of relying on historical company data.

- Distressed firms. Companies experiencing financial distress are difficult to value. They have considerable debt so their FCFE is usually negative due to high debt servicing requirements. A two or three-stage FCFF module should be used to value these firms as FCFF is less likely to be negative than FCFE. Detailed projections for the initial turnaround period are prepared followed by a healthy, more stable growth period. If the company is expected to fail, then the liquidation value of individual assets and liabilities are used to value the business. Private equity firms called vulture capitalists specialize in buying bankrupt companies at the lowest price possible and then making a profit by turning them around or breaking them up.

7.4 | Market Multiples Approach – P/E, P/BV, and P/S

When using the market multiples approach to value a firm, a benchmark multiple is first calculated that relates share price (P) to a measure of financial performance such as earnings per share (EPS), book value per share (BVPS), or sales per share (SPS). The benchmark is then multiplied by the company’s historical or estimated future EPS, BVPS, or SPS to determine its appropriate share price. Finally, this price is multiplied by the number of common shares to calculate the intrinsic value (V0) of the firm.

[latex]V_{0}=\text{Benchmark }(P/EPS)(EPS)(\text{Number of common shares})[/latex]

[latex]V_{0}=\text{Benchmark }(P/SPS)(SPS)(\text{Number of common shares})[/latex]

[latex]V_{0}=\text{Benchmark }(P/BVPS)(BVPS)(\text{Number of common shares})[/latex]

Given the uncertainty of business valuations, analysts typically use more than one type of benchmark multiple to improve the accuracy of their results.

Price/Earnings (P/E) Multiple

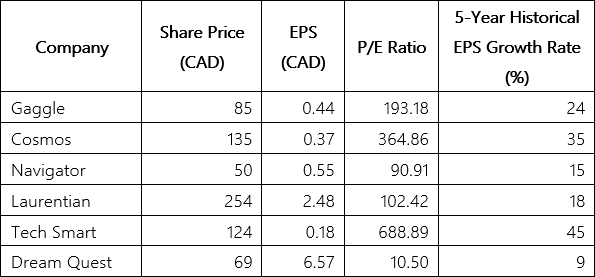

A P/E multiple measures how much investors are willing to pay for each dollar of a company’s earnings. It is the most widely recognized and commonly used market multiple as earnings are the primary indicator of financial performance since it includes both revenues and costs. Over the long term, firms with low P/Es usually underperform the market while those with high P/Es outperform it.

Despite its popularity, using the P/E multiple to value a firm has a number of potential shortfalls. Many companies manipulate earnings to misrepresent their financial performance. Aggressive revenue recognition policies are adopted to record sales prematurely. Costs are reduced by excessive cost capitalization, altering accounting estimates like the bad debt percentage, or delaying discretionary costs such as advertising, maintenance or R&D. Companies may not intentionally manipulate their financial statements, but the wide choice of accounting policies under IFRS makes them less comparable to other firms. P/E multiples also vary over the business cycle especially with cyclical firms like automobiles that experience large swings in sales and may have high degrees of operating and financial leverage that cause profits to be even more variable. Finally, earnings can sometimes be small, zero or negative especially for start-up and cyclical companies which is illogical when incorporated into a P/E multiple.

To apply the market multiples approach using P/E, analyst must calculate a firm’s EPS and then the benchmark P/E multiple.

-

- Calculating EPS. EPS is calculated using either trailing EPS from the previous four quarters or leading or forward EPS estimated for the next four quarters. Leading EPS is preferable as it is forward looking and incorporates recent operational and financial changes such as a company expansion or a revision to its capital structure. Trailing EPS should be used if reliable future earnings estimates are not available.

- When calculating leading EPS, valuators can use their own earnings forecasts, forecasts of equity analysts who follow the company, or consensus forecasts of these analysts provided by financial information firms. The exact method used to calculate trailing and leading EPS varies among the information providers so analysts must ensure all earnings data is measured consistently. Diluted EPS which correctly includes the potential effect of convertible securities or options should be used.

- Earnings can be adjusted for aggressive revenue and cost recognition practices. Non-recurring accounting charges like discontinue operations, restructuring charges, and gains/losses on asset sales may also be eliminated so the P/E multiple reflects continuing earnings. Finally, adjustments can be made for differences in accounting policies adopted by companies such as LIFO versus FIFO inventory. LIFO is not allowed under IFRS, but it is still regularly used by U.S. companies. In practice, making these adjustments is difficult due to a lack of information in the company’s financial disclosures and it is also time consuming.

- Valuators typically normalize or average trailing EPS to compensate for the effects of the business cycle on earnings including losses. The two methods used include:

- Average historical EPS. Diluted EPS is averaged over the last business cycle.

- Average historical ratios. Rate of return on equity () is averaged over the last business cycle. This average ratio is then multiplied by the company’s current BVPS. BVPS cancels out leaving an estimate of EPS.

- [latex](\frac{{EPS}}{{BVPS}})BVPS=EPS[/latex]

- The average historical ratios method is preferred. If diluted EPS is normalized over the last business cycle, the older EPS figures will likely be smaller as they do not include the growth in the business over that period. Alternatively, ROE will not be affected by growth since both net income and shareholders’ equity rise as the business grows. Taking the average ROE over the last business cycle and then applying it to the current BVPS provides a more accurate measure of EPS. The opposite logic applies if a firm becomes smaller.

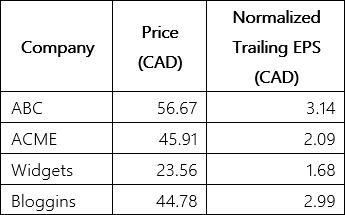

- To compare companies with small, zero or negative EPS, the earnings yield ratio $latex=\frac{{EPS}}{{BVPS}}) can be substituted for the P/E multiple. This allows valuators to rank companies based on their financial performance regardless of whether it is positive or negative.

- Calculating the benchmark P/E multiple. Once EPS is accurately measured, the benchmark P/E multiple is determined using one of the following methods:

- Justified P/E benchmark multiple based on fundamentals. The one-stage DDM is used to determine a firm’s justified P/E multiple. Substituting P0 for V0 in formula 1, both sides of the one-stage DDM are then divided by leading earnings per share (E1) in formula 2.

- [latex]\text{Formula 1 }P_{0}=\frac{{D_{1}}}{{k_{c}-g_{d}}}[/latex]

- [latex]\text{Formula 2 }\frac{{P_{0}}}{{E_{1}}}=\frac{{\frac{{D_{1}}}{{E_{1}}}}}{{k_{c}-g_{d}}}[/latex]

- Formula 2 indicates that the justified leading P/E multiple is a function of three fundamental factors kc, gd, and D1/E1 which is a company’s expected payout ratio. The higher the risk level of a company as measured by kc, the lower the P/E multiple. The higher the company’s growth rate as measured by gd, the higher P/E multiple. Additionally, the higher the payout ratio, the higher the P/E multiple. The justified trailing P/E multiple formula is slightly different, but it is a function of the same three factors.

- [latex]\text{Formula 3 }\frac{{P_{0}}}{{E_{0}}}=\frac{{\frac{{D_{0}}}{{E_{0}}}(1+g_{d})}}{{k_{c}-g_{d}}}[/latex]

- A firm’s justified P/E multiple is calculated by inputting estimates for these three fundamentals into either formula 2 or 3. The analyst then compares the company’s justified P/E multiple to its actual P/E ratio to decide whether the company is under, over, or fairly valued. Given the potential for estimating error, valuators typically establish a range of 5.0% around the justified P/E multiple. If a company’s P/E ratio falls in this range, they are considered fairly valued but otherwise they are either under or overvalued. Alternatively, the justified P/E multiple can be multiplied by leading EPS to estimate the firm’s value and the 5.0% range is used to establish an appropriate confidence interval.

- As discussed, if companies do not pay dividends or pay dividends that are well below or above what they should be paying, FCFE may be substituted for D. The two-stage and three-stage DDM can also be used to determine the justified P/E multiple for more complex multi-stage valuations where the fundamentals are expected to vary over the life of the business.

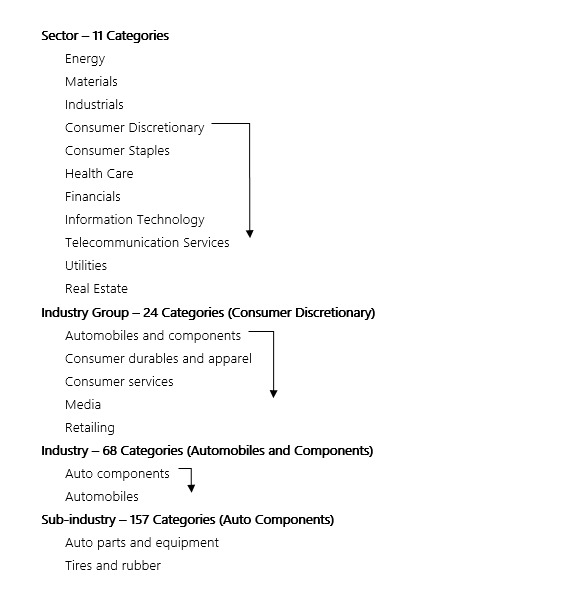

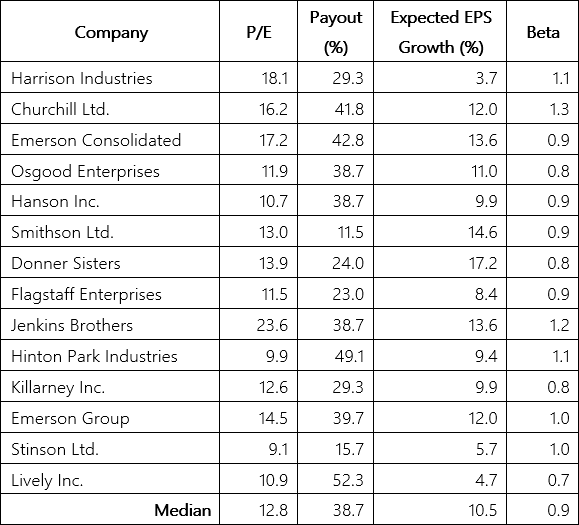

- Comparable companies. Companies with equivalent operational and financial characteristics should have similar financial ratios. As a result, the average or median P/E ratio for a carefully selected group of comparable companies (also called a peer group) should provide a reliable benchmark P/E multiple. Median values are typically used to eliminate the effect of outliers.Industrial classification systems determine groupings of comparable companies. One commonly used system is the Global Industry Classification Standard (GICS) sponsored by Standard & Poor’s and MSCI. This system classifies companies by sector, industry group, industry, and sub-industry with sub-industry being the most precisely defined category. Below is an example of how a company producing auto parts and equipment is categorized.

-

Exhibit 2: Global Industry Classification Standard

- To determine the most accurate benchmark P/E multiple possible, comparable companies should be selected from the relevant sub-industry group. If the number of companies in the sub-industry are insufficient to provide a reliable benchmark, the larger industry, industry group or sector grouping may be used although these companies will be less representative of the firm being valued. P/E multiples for the industry, industry group, sector, or the stock market as whole may be used for comparison if analysts feel a sub-industry is over or undervalued relative to the larger economy. Mispricing sometimes occurs due to market inefficiencies that affect the entire sub-industry such as the internet bubble in the early 2000s.

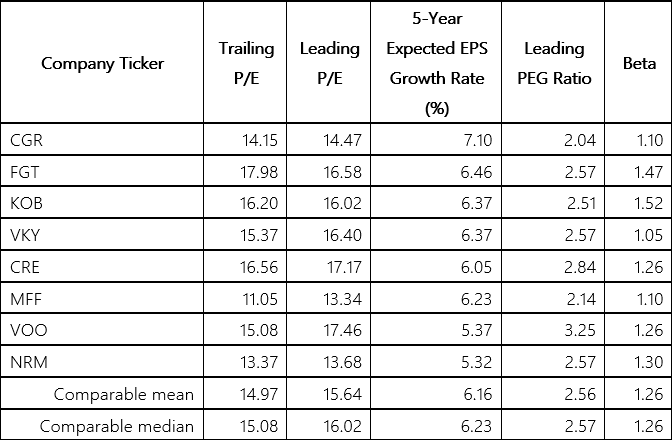

- A value investor may buy an undervalued share expecting that the firm’s P/E ratio will eventually rise to the mean or median P/E multiple of its peer group once any market inefficiencies correct themselves. Before taking investment action, investors should carefully consider whether there are good reasons for the firm’s lower P/E ratio. According to the justified P/E multiple formula, P/E is a function of the fundamental factors risk, growth, and dividend payout. A firm’s low P/E compared to its peer group may not be due to market inefficiencies, but higher risk, lower growth prospects, or reduced payout. This means the lower P/E ratio may be justified. The P/E-to-growth (PEG) ratio is commonly used with the comparable companies’ method to measure what investors are paying for growth to determine if a company’s current P/E ratio is reasonable or not. PEG is calculated as a firm’s PEG ratio divided by the expected percentage growth rate. A low PEG ratio in relation to the other comparable companies does not always indicate an undervalued share if there is a high level of risk or low payout.

- Multi-regression analysis. This method is used to measure the cause and effect relationship between P/E ratios and the three fundamental factors of risk, growth, and payout. Based on comparable companies from the same sub-industry, a multi-regression equation that estimates P/E based on these three factors is calculated. Estimates of growth, payout, and risk for the company are then inputted into the equation to determine the benchmark P/E multiple. The growth rate is typically the five-year expected growth rate of earnings or some proxy such as the growth rate of dividends or sales. Risk can be measured by a company’s kc, beta, or another volatility measure such as the coefficient of variation of earnings.

- In practice, the multi-regression approach is not widely used to estimate the benchmark P/E multiple. Low and unstable R squares, multi-collinearity between variables, and unstable regression coefficients with low confidence and incorrect signs are serious problems. Analysts attempt to correct for these concerns by eliminating variables that are multi-collinear, adopting more accurate measures of risk, growth, or payout or using industry, sector or market data instead of sub-industry data to increase the sample size.

- Historical average price multiples. If reliable comparable company data is not available, the benchmark P/E multiple can be calculated using the company’s own average or median P/E ratio over the last business cycle. By averaging the P/E ratio instead of EPS, changes in the business’ size are incorporated. Do not use this method if a firm’s business mix or level of financial or operational leverage has been altered as past data will not be representative of future performance.

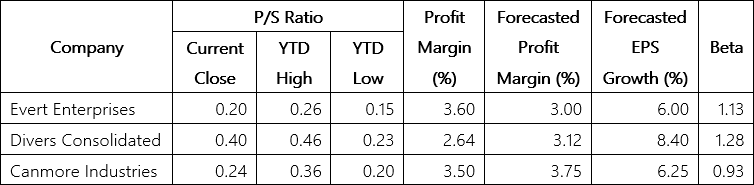

Price/Sales (P/S) Multiple

Some analysts prefer the P/S multiple to the P/E multiple because sales are easier to estimate, never negative, more stable than earnings over the business cycle, and subject to less accounting manipulation. Sales should still be normalized for the business cycle and adjusted for aggressive revenue recognition practices to provide the most accurate valuation possible.

The main problem with the P/S multiple is it does not include operating expenses and interest making it a poorer measure of a business’ overall performance. The P/S multiple is effective though when valuing mature companies or firms with standardized operating procedures which results in similar cost structures. This is the case with franchises where P/S multiples are used to value individual outlets when they are traded between franchisees or with the franchisor. P/S multiples are also employed to value start-ups that are not yet generating profits.

Most valuation practices used with P/E multiples can also be apply to P/S multiples. When calculating the justified trailing P/S multiple, there is an additional fundamental factor. Formula 1 is the one-stage DDM. Formula 2 is a derivation of formula 1 that shows DPS is equivalent to EPS times the payout ratio. Because current values are used for earnings and payout, the expected growth rate is applied. In Formula 3, both sides of the formula are divided by SPS. EPS divided by SPS is the NPM.

[latex]\text{Formula 1 }P_{0}=\frac{{D_{1}}}{{k_{c}-g_{d}}}[/latex]

[latex]\text{Formula 2 }P_{0}=\frac{{E_{0}\times \frac{{D_{0}}}{{E_{0}}}\times (1+g_{d})}}{{k_{c}-g_{d}}}[/latex]

[latex]\text{Formula 2 }\frac{{P_{0}}}{{S_{0}}}=\frac{{NPM_{0}\times \frac{{D_{0}}}{{E_{0}}}\times (1+g_{d})}}{{k_{c}-g_{d}}}[/latex]

The justified P/S multiple is a function of NPM in addition to risk, growth, and payout.

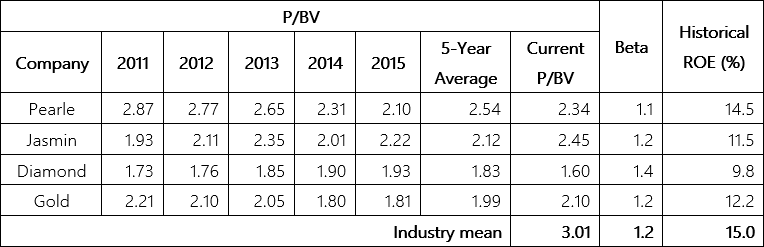

Price/Book Value (P/BV) Multiple

Some analysts prefer the P/BV multiple to the P/E multiple because BV is nearly always positive, is more stable over the business cycle, and is harder to manipulate. The main problem with this multiple is that many assets and liabilities are recorded at historical cost instead of fair market value, while other assets such as patents that are developed internally or off-balance sheet financing such as take-or-pay contracts are not included in the balance sheet at all. For the best results, book value should be re-calculated to include all recognized and unrecognized assets and liabilities measured at their fair market value. This is difficult in practice because of limited company financial disclosures and some intangible assets such superior employees, strong customer service, or superior product quality are very difficult to measure. Finally, the P/BV multiple is not suitable for service firms who have few fixed assets or companies in sub-industries with large differences in cost structure due to varying degrees of labour or capital intensity. Remember that preferred shares and any preferred dividends in arrears need to be removed from book value as only common equity is being valued.

Justified trailing P/BV multiple is a function of ROE plus risk, growth, and payout. Formulas 1 and 2 are the same as for the P/S multiple. Formula 3 is a derivation of formula 2 that shows E is equivalent to BV times ROE [latex]\frac{{E}}{{BV}}[/latex]. In formula 4, both sides of the formula are divided by BV leaving the four factors.

[latex]\text{Formula 1 }P_{0}=\frac{{D_{1}}}{{k_{c}-g_{d}}}[/latex]

[latex]\text{Formula 2 }P_{0}=\frac{{E_{0}\times \frac{{D_{0}}}{{E_{0}}}\times (1+g_{d})}}{{k_{c}-g_{d}}}[/latex]

[latex]\text{Formula 3 }P_{0}=\frac{{BV_{0}\times ROE_{0}\times \frac{{D_{0}}}{{E_{0}}}\times (1+g_{d})}}{{k_{c}-g_{d}}}[/latex]

[latex]\text{Formula 4 }\frac{{P_{0}}}{{BV_{0}}}=\frac{{ROE_{0}\times \frac{{D_{0}}}{{E_{0}}}\times (1+g_{d})}}{{k_{d}-g_{d}}}[/latex]

7.5 | Market Multiples Approach – P/CF and EV/EBITDA

Other benchmark market multiples provide a more accurate business valuation by addressing some of the problems with traditional P/E, P/S, and P/BV multiples.

Price/Cash Flow Multiple

Some valuators replace EPS in the P/E multiple with a firm’s cash flows as this amount is more stable, less likely to be negative, subject to less manipulation, and not affected as much by a firm’s choice of accounting policies. Different measures of operating cash flows include:

- Earnings before interest, taxes, depreciation and amortization (EBITDA). EBITDA provides a quick approximation of operating cash flows by adding back depreciation and amortization to EBIT. These are typically a firm’s largest non-cash expenses. Using EBITDA is not recommended as it does not include interest and taxes which are major cash items, nor does it adjust for changes in NWC and other non-cash transactions such as gains and losses on asset sales.

- Cash flows from operations. CFO is given on the statement of cash flows and is a more accurate measure of operating cash flows than EBITDA. It can be manipulated as IFRS gives considerable discretion in classifying certain transactions allowing firms to exaggerate CFO. Normally interest paid and interest and dividend income received are classified as operating activities as they are included in the determination of net income. Interest paid can also be classified as a financing activity as it is a cost of financing which increases CFO. Interest and dividends received may be classified as investing activities as they are investment returns which lowers CFO. Dividends paid are normally classified as a financing activity because they are a cost of financing. They may be classified as an operating activity to assist users in determining an entity’s ability to pay dividends out of operating cash flows which lowers CFO.

- To manipulate CFO, companies can capitalize additional costs as inventory or fixed assets, so they appear as investing and not operating activities. Over the short-term, they can also defer payments on accounts payable, delay discretionary costs such as advertising, maintenance, and R&D, reduce inventory purchases, or accelerate accounts receivable collections using expensive cash discounts or factoring.

- Under US GAAP, interest paid and interest and dividend income received must be included in operating activities while dividends paid are always classified as financing activities. This provides a more accurate measure of the cash return for common equity holders and should be used for valuation purposes. These amounts must be disclosed separately under IFRS so analysts can easily reclassify them when valuing a firm. Other adjustments relating to the manipulation of CFO and non-recurring items should be made if the needed information is available.

- The justified trailing P/CFO multiple is a function of risk, growth and D/CFO. D/CFO is another dividend payout measure that is based on cash flows from operations.

- [latex]\frac{{P_{0}}}{{CFO_{0}}}=\frac{{\frac{{D_{0}}}{{CFO_{0}}}(1+g_{CFO})}}{{k_{c}-g_{CFO}}}[/latex]

- Free cash flow to equity. FCFE improves on CFO by including capital expenditures (CE) net of any borrowing (NB). They are a firm’s total cash flows and not just the operating cash flows available to equity investors. One of the formulas for FCFE is:

- [latex]FCFE=CFO-CE+NB[/latex]

- Because CE and NB vary considerably from year-to-year, FCFE is usually more variable than CFO. These amounts should be normalized over the business cycle.The justified trailing P/FCFE multiple is a function of risk and growth. As discussed, D and FCFE should be equivalent.

- [latex]\frac{{P_{0}}}{{FCFE_{0}}}=\frac{{(1+g_{FCFE})}}{{k_{c}-g_{FCFE}}}[/latex]

Economic Vlaue/EBITDA Multiple

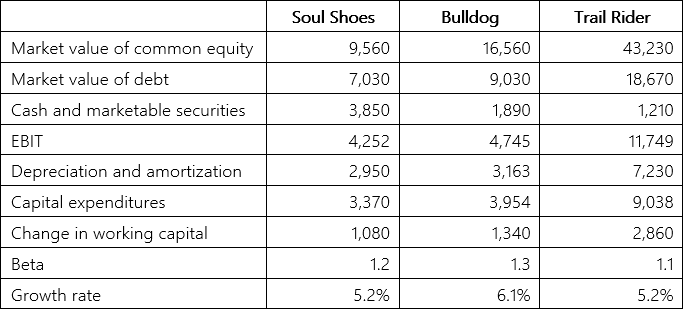

Instead of using a firm’s share price in a market multiple, some valuators substitute enterprise value (EV). EV is the market value of its common equity, preferred shares and debt minus any cash, cash equivalents and short-term investments. It is the value of the firm to all investors which includes both the debt and equity holders. Cash, cash equivalents, and short-term investments are deducted as they are not needed in the operation of the business and can be used to buyout current debt and equity investors thus lowering the cost of the acquisition or value of the firm. EV is then divided by EBITDA which approximates operating cash flows available to debt and equity holders as it is EBIT before interest plus taxes, depreciation, and amortization.

EV/EBITDA is a useful multiple because it is capital structure neutral. This means it excludes the effect of financial leverage by not including interest which is important if the use of debt varies substantially between comparable companies. EV/EBITDA is also capital intensity neutral as it excludes depreciation and amortization which is important if the comparable companies have different fixed cost structures. Reliable market values are typically available for debt and preferred shares, so once EV is determined using the benchmark EV/EBITDA multiple then the value of these securities is deducted to determine the value of the common equity.

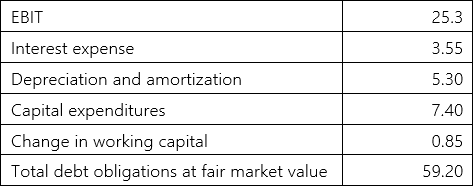

FCFF is preferable to EBITDA because it correctly measures all of a firm’s cash flows and not just the operating cash flows available to debt and equity holders. One of the formulas for FCFF indicates:

[latex]FCFF=CFO+(I)(1-TR)-CE[/latex]

FCFF begins with CFO but then capital expenditures (CE) are deducted. Interest (I) is added back on an after-tax basis and net borrowing (NB) is not included because they relate to the debt holders. As discussed in the income approach using FCFF section, EV is equal to the present value of a firm’s future FCFF:

[latex]EV_{0}=\frac{{FCFF_{0}(1+g_{FCFF})}}{{WACC-g_{FCFF}}}[/latex]

WACC is the appropriate discount rate since FCFF is available to both debt and equity holders. Again, to determine the value of the firm to the common shareholders only, the current market value of the company’s debt and preferred shares are deducted.

The justified trailing EV/FCFF multiple is a function of risk and growth.

[latex]\frac{{EV_{0}}}{{FCFF_{0}}}=\frac{{(1+g_{FCFF})}}{{WACC-g_{FCFF}}}[/latex]

7.6 | Asset-Based Approach

The asset-based approach values a company by taking its historical cost balance sheet and restating all its assets and liabilities at their fair value. The difference between total assets and liabilities is the fair market value of the business. This approach is used sparingly because of the difficulty valuators have accurately pricing non-financial assets including land, building, equipment, and particularly intangible assets and goodwill. Also, more information is generally available about an entire business operating as a going concern than its individual assets and liabilities. With IFRS, more assets and liabilities are now recorded at fair value instead of historical cost which makes this method simpler to apply.

The asset-based approach is best used to value four types of companies. These include 1) distressed companies where the fair market value of their net assets is usually more than their value as part of a going concern, 2) financial institutions and investment funds whose assets are largely financial and can be more accurately valued individually as they typically trade in active secondary markets, 3) resource and real estate companies whose main assets are properties with objectively determinable outputs, and 4) small, privately traded start-up companies where estimating future cash flows is difficult and few intangible assets or goodwill exists.

Steps in Applying the Asset-Based Approach

- Step 1 Obtain a historical cost-based balance sheet

- Step 2 Identify any off-balance sheet assets and liabilities including:

- Unrecorded tangible or intangible assets

- Contingent liabilities

- Non-capitalized leases

- Other off-balance sheet assets and liabilities

- Step 3 Measure all assets and liabilities at fair value if material

- Step 4 Estimate the fair value of any goodwill

- Step 5 Construct a fair value-based balance sheet

Valuation Methods

Different methods can be used to determine the fair value of assets and liabilities.

- Financial assets and liabilities. These assets and liabilities derive their value from a contractual claim or obligation involving cash and frequently trade in active secondary markets. Under IFRS, these assets and liabilities are usually recorded at fair value already. If not, they should be recorded at the present value of their future cash flows using a discount rate that reflects the riskiness of the asset or liability. Any allowances for doubtful accounts should be re-assessed as part of the valuation process.

- Inventory. These assets can be valued at either replacement cost or net realizable value (NRV). Replacement cost is what a company would currently pay to replace an asset with another asset in similar condition. NRV is what the inventory can be sold for less any costs to complete and dispose of the asset.

- Long-term assets. These assets, which include land, building, equipment and intangibles, are valued using either the market, income or cost approaches. The market approach reviews recent sales of similar assets and adjusts for differences in the quantity and quality of output. The income approach estimates an asset’s future cash flows and determines their present value using a discount rate that reflects the riskiness of the asset. The cost approach looks at what is would cost to buy or build a replacement asset with a similar quantity and quality of output.

- Goodwill. This is the portion of a business’ value that is not attributable to specific tangible or intangible assets. It results from superior operating performance and the ability to produce innovative, high-quality goods and services. Under IFRS, goodwill is only recorded when purchased based on the objectivity principle. Companies who frequently engage in acquisitions have considerable goodwill while those that avoid acquisitions do not. Goodwill is also not regularly amortized under IFRS, but it is written down when the cash-generating unit the goodwill relates to is written down. This means that the value of a company’s goodwill is unreliable and should be re-assessed when using the asset-based approach.

- Goodwill is valued at the present value of a company’s excess earnings.

- [latex]\text{Excess earnings }=FCFF-(\text{Net assets})(WACC)[/latex]

- Excess earnings are the additional profits a company actually earns compared to what it should earn given the assets it employs and their required rate of return. As discussed, FCFF is what a company earns from the perspective of both debt and equity investors. Net assets consist of long-term assets plus net working capital. WACC is the required rate of return of debt and equity investors. Instead of using the WACC, separate required rates of return for net working capital, fixed assets and intangibles may be estimated. The rate for net working capital would be the lowest given its lower risk as an asset class, followed by fixed assets, and then intangible assets. The weighted average of these separate required rates of return should approximate the WACC. In practice, these individual rates are not readily available, so WACC is used for all asset classes.Valuators can assume that the excess earnings will last indefinitely or only for a finite period of time. Excess earnings are likely to attract competition, so unless the industry has high barriers to entry, a finite period should be adopted.

7.7 | Residual Income Approach

Some managers feel that if a firm is profitable it is creating value for its investors. This is incorrect because although net income (NI) includes interest expense that fairly compensates debt holders, there is no deduction for the cost of common equity. If NI is insufficient to meet the shareholders’ required rate of return (RRR), the company is actually destroying value. Consider the following company after its first year of operations:

Exhibit 3: Destroying Shareholder Value

| BV | CAD 250,000 |

| Number of common shares | 10,000 |

| P0 at the beginning of the year | CAD 25.00 |

| P0 at the end of the year | CAD 18.75 |

| NI | CAD 18,750 |

| EPS | CAD 1.875 |

| RRR (kc) |

10.0% |

Shareholders invested CAD 250,000 and expected to make at least CAD 25,000 (CAD 250,000 × 0.10) in the first year. NI was only CAD 18,750, so equity investors received CAD 6,250 (CAD 25,000 – CAD 18,750) less than required. In percentage terms, the firm generated a ROE of 7.5% (CAD 18,750 / CAD 250,000) but investors required 10.0%. The company did not generate an adequate return to compensate its shareholders and thus destroyed value. If investors continue to receive CAD 6,250 less than required in perpetuity, a total of CAD 62,500 (6,250 ÷ 0.10) or CAD 6.25 per share (CAD 62,500 / 10,000) will be lost. The company’s share price fell from CAD 25.00 to CAD 18.75 (CAD 25.00 – CAD 6.25) to reflect this poor performance. Any new investors buying into the company will now receive the required return of 10.0% (1.875 ÷ 18.75) due to the decline in share price. A company’s share price will rise and fall so investors always earn the RRR in efficient markets.

Residual income (RI) is the difference between a company’s NI and its shareholders’ RRR. If this amount is positive, the firm is creating value and its share price will rise above its BVPS. If RI is negative, the share price will fall below BVPS as the firm is destroying value. If the firm generates no RI, it BVPS should approximate its share price. The following equivalent formulas demonstrate this relationship and the different ways to calculate RI:

[latex]V_{0}=BVPS_{0}+\sum\limits_{t=1}^\infty \frac{{RI_{t}}}{{(1+k_{c})^{t}}}=BVPS_{0}+\sum\limits_{t=1}^\infty \frac{{EPS_{t}-k_{c}BVPS_{t-1}}}{{(1+k_{c})^{t}}}=BVPS_{0}+\sum\limits_{t=1}^\infty \frac{{(ROE_{t}-k_{c})BVPS_{t-1}}}{{(1+k_{c})^{t}}}[/latex]

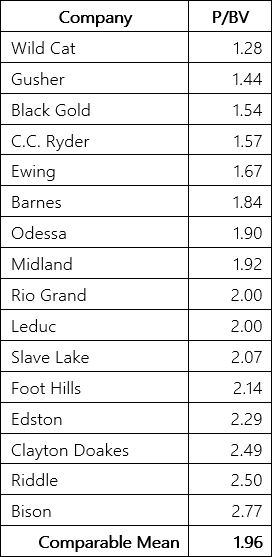

The current P/BV ratio for the S&P 500 is 3.58 indicating that on average the 500 largest U.S. public companies are creating value.

RI is also referred to an economic profit, excess earnings, abnormal profits or economic value added (EVA)®. EVA is a registered trade mark of Stern Stewart & Company, a U.S-based consulting firm that publishes a set of adjustments to earnings and book value in order to provide a more accurate measure of RI. These adjustments are similar to those discussed for the P/E and P/BV multiples. Besides business valuation, residual income is also used internally by companies to measure business unit performance and determine appropriate levels of executive compensation. This is discussed in the Module: Financial Statement Analysis.

Valuing Equity Using the RI Approach

The intrinsic value (V0) of a company can be estimated using a one-stage, two-stage or three-stage RI model. The one-stage model is used if valuators expect the firm’s ROE and other inputs will remain constant. The formula is modified as follows:

[latex]V_{0}=BVPS_{0}+\frac{{(ROE-k_{c})BVPS_{0}}}{{k_{c}-g}}[/latex]

The one-stage model is of limited value because ROE is usually not stable. If a firm’s ROE is above its kc, it will likely revert to kc over time as new competitors enter the market and eliminate any excess profits. Alternatively, if a firm’s ROE is below its kc, it may rise over time as competitors leave the market. Finally, if its kc is expected to consistently exceed its ROE, the firm should be liquidated and its assets redeploy to other investments that create shareholder value. Valuators normally assume a ROE above kc in the initial stage that reverts to kc in the terminal period.

The RI approach has a number of advantages and disadvantages compared to the other valuation methods. It is more easily applied to companies that do not pay dividends or whose cash flows are unstable. It focuses on profitability which some valuators feel is a more accurate measure of a firm’s performance than dividends or cash flows because it is smoother over time. It uses readily available accounting data, although adjustments should still made to eliminate aggressive accounting policies, report assets and liabilities at their fair value, and remove non-recurring or unrelated items. Finally, the firm’s terminal value makes up a very small portion of its intrinsic value unlike the income approach based on dividends or cash flows. This is because the valuation formula for the RI approach begins with a firm’s BVPS and then adds the present value of RI to determine its intrinsic value. These RI amounts are more recent so they are easier to estimate accurately compared to a firm’s terminal value. The RI approach typically assumes a terminal value of zero as the firm’s ROE reverts to it kc over time resulting in no RI.

Final Valuation

Business valuation is an imprecise process. Instead of relying on just one approach, most analysts employ a number of different valuation methods to improve the accuracy of their results. Some methods may be eliminated because their inputs are difficult to estimate or the final results are outliers. A weighted average of the remaining valuations is then calculated.

Exhibit 4: Weight-Average Valuation

| Method | Estimate

(CAD) |

Weight |

| DDM | 43.62 | 25% |

| FCFE | 36.42 | 30% |

| FCFF | 44.09 | 25% |

| P/E | 51.33 | 10% |

| P/BV | 53.87 | 10% |

| Firm Value | 43.37 | 100% |

The weights are subjectively determined and greater emphasis is placed on the methods an analyst feels are more reliable. The usefulness of a particular valuation approach varies with a firm’s position in the company life cycle.

- Development stage. Asset-based approach is best as these companies do not pay dividends and their future cash flows are difficult to determine due to a lack of historical data.

- Growth stage. Residual income or income approaches using either FCFE or FCFF are favoured as rapidly growing cash flows can be more precisely estimated.

- Mature stage. Market multiples approach is preferred as growth is limited and industry relationships are well established making company comparisons more accurate.

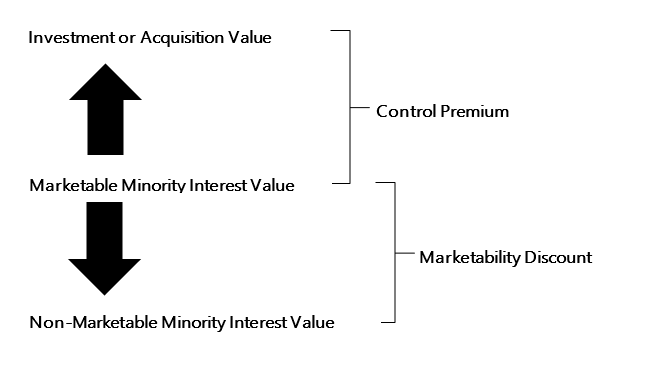

7.8 | Control Premium, Marketability Discount, and Private Firms

The business valuation process is not complete when the value of a company is determined using the income, market multiples, asset-based or residual income approaches. This value, which is referred to as the marketable minority interest value, may have to be adjusted upward or downward to incorporate a control premium or marketability discount.

Exhibit 5: Control Premium or Marketability Discounts

Control Premium

A control premium is the additional consideration a buyer will pay a seller over the marketable minority interest value to acquire a controlling interest. Investors with a controlling interest can make improvements to the company’s operations that a minority investor cannot resulting in synergies that increase the value of the firm.

Factors that increase potential synergies and the size of the control premium include:

- Poor management.

- Weak corporate governance.

- Excessive executive compensation and management perks.

- Ability to increase revenues and realize cost efficiencies.

- High discretionary expenses such as advertising that can be quickly reduced.

- Non-optimal use of financial leverage.

- Low dividend payout resulting in unprofitable investments and large amounts of low-yielding, non-operating assets such as excess cash or real estate.

- Supermajority voting rules or weak non-controlling shareholder rights that entrench management and limit the likelihood of an acquisition.

- Holding the balance of power between two competing shareholder groups which is called a swing vote premium.

Control premiums average from 20% to 30% based on studies of share prices before and after corporate acquisitions. Acquisitions can be very lucrative for buyers as long as they do not over pay and give all the synergies to the seller. When the control premium is expressed as a percentage of a firm’s investment or acquisition value, it is referred to as a non-control discount. The topic of synergies and control premiums, which are also called take-over premiums, are important issues in Module: Mergers & Acquisitions and Corporate Restructuring.

Marketability Discount

A marketability discount is the reduction in the marketable minority interest value a buyer receives to fairly compensate them for the lack of a ready market for their shares. Marketability is not usually a problem for public companies whose shares actively trade in secondary markets, but it is for private firms whose shares are much less liquid. Marketability discounts typically range from 40% to 60% based on studies of share prices before and after initial public offerings. Going public is lucrative for shareholders in private companies due to the elimination of the marketability discount.

Liquidity is not the only factor that influences the size of a marketability discount. Any factor that makes a private company’s shares less appealing to potential buyers will increase the marketability discount. Many of these factors are measured separately and have their own names. Some examples include:

- Low prospect of a public offering or business sale by the owners.

- High share issuance costs reducing the willingness to go public.

- Small firm size limiting its access to capital which raises the cost of borrowing.

- Weak performance due to poor governance and public financial oversight.

- Concentrated share ownership leading to abuses of power when dealing with minority investors.

- Limited access to financial information making it difficult for investors to monitor the company’s performance.

- Low or infrequent dividends indicating low company profitability or agency problems such as excessive management pay or perks.

- Ownership of a large block of the shares that are more difficult to sell which is called a blockage discount.

- Small pool of potential buyers that are interested in buying the shares.

- Provision preventing investors from selling their shares for a specific period of time after an initial public offering to support the share price which is called a lock-up agreement.

- Limited management depth so the departure of key staff exposes the company to considerable risk which is called a key-person discount.

- Greater difficulty attracting strong managers due to lower salaries and fewer career opportunities within the firm.

- Limitations on the rights of certain shareholder groups such as non-voting shares which is called a restrictive shareholder agreement discount.

- Actions are highly influenced by tax planning strategies and not their business merit.

A private company does offer some advantages that help reduce the marketability discount. They are leaner and more flexible than public firms because of their limited access to resources and smaller size. A private firm is not as focused on short-term earnings and share price performance due to a lack of public oversight enabling them to concentrate more on long-term growth. Finally, agency costs may be lower as managers are also owners and will only hurt themselves if they choose not to maximize share price.

Valuing Private Companies

The income, market multiples, asset-based, residual income approaches can also be used to value private companies, but there are a number of limitations due to the unique nature of these enterprises.

- Financial information quality. Before using accounting information to value a business, its earnings should be normalized to smooth out the effects of the business cycle, eliminate aggressive accounting policies, and remove any non-recurring or unrelated items. Assets and liabilities should also be reassessed at their fair market value. This is more difficult to do for a private company since their financial statements are generally not subject to a full audit by a qualified public accounting firm. They typically receive a less rigorous review engagement or compilation which provides a lower level of assurance and less detailed financial statement notes. In Canada, private companies use a simplified set of accounting standards called Accounting Standards for Private Enterprises (ASPE) that do not provide as detailed disclosures as IFRS.

- Private companies typically engage in numerous non-arm’s length transactions with their majority owners who may abuse their control positions to benefit themselves at the expense of their minority investors. Excessive salaries, lavish expense accounts, shareholder loans, life insurance policies, personal vehicles, and private residences may be received by the majority owners as well as their family members and friends who are employ by the firm. Frequently, a private company owns assets that it does not use but it still pays all the expenses for the majority owner. In other cases, the majority owner may lease their private assets to the company at an above market rate. Sometimes, the majority owner may work for less than the market rate, allow their firm to use their personal assets or lend it money at below market rates.

- To properly value a private firm, earnings should be normalized to adjust for these questionable non-arm’s length transactions. Excessive pay and perks should be eliminated especially for friends and relative who are employed by the business but do little work. Assets that are not used by the business should be removed from the financial statements along with any income they produce and retreated as non-operating investments. If the assets are used, they should be recorded at their fair market value and depreciated appropriately. If assets are rented from the majority owners, a lease agreement should be capitalized at the market interest rate and appropriate amounts of interest and depreciation expense recognized.

- Financial projections. Many private firms are small businesses in the early stages of their development, which makes forecasting their future performance very difficult. Company managers are likely the most knowledgeable about the firm’s potential but they are less experienced preparing financial projections and their forecasts tend to be either overly optimistic or pessimistic. Valuators should utilize this valuable source of information but be very cautious. Given the high level of uncertainty, valuators may employ scenario analysis when valuing companies instead of relying a single (i.e. most-likely) estimate of future operations. For start-ups, the scenarios could include a successful initial public offering, acquisition by another firm, continued operation by the owner as a private company, or liquidation if the business fails. For established private companies, scenarios may be constructed for different levels of growth and profitability. Each option is valued using different cash flow estimates and a cost of capital that reflects its riskiness. A probability is assigned to each scenario and an expected value is determined.